{kind=link}

{kind=link}

{kind=link}

{kind=link}

South Africa economic outlook, December 2022 has been saved

The authors would like to thank Santhuri Padayachee for her assistance with research.

Cover image by: Jaime Austin

As the world learns to live with COVID-19 without closing down economies in the face of rising infections, South Africa has had to deal with a range of new challenges: systemic supply chain disruptions, rampant global inflation, and the beginnings of a global recession, among others—all exacerbated by the war in Ukraine. These, together with ongoing local challenges such as power cuts, underperforming utilities, long overdue structural reforms, and the devastating impacts of climate-related events, are weighing on South Africa’s growth outlook.

However, progress made in recent months, particularly toward fiscal consolidation goals, relatively early monetary tightening, as well as some network industry reforms, will likely support an environment that promotes growth, investment, and job creation in the medium term. For example, the recently improved budget deficit allows for some fiscal space for further structural reforms that are essential to create the right environment for growth. Moreover, some industries show potential for improved and accelerated growth, especially those supporting the transition to carbon neutrality.

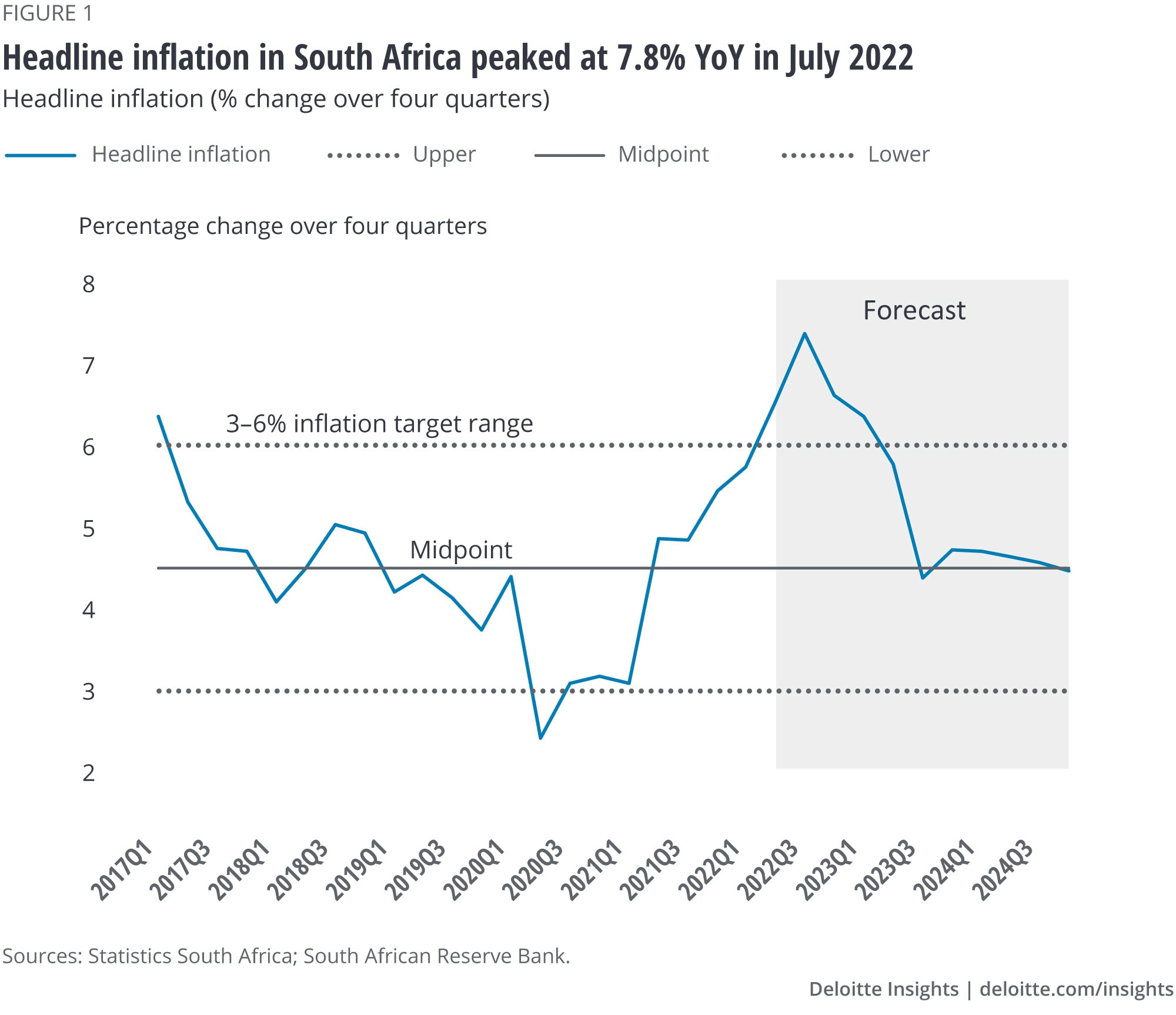

In 2022, global year-on-year (YoY) inflation breached highs last seen during the energy crises of the 1970s, with South Africa’s headline inflation peaking (so far) at 7.8% YoY in July 2022 (figure 1). While inflation moderated to 7.5% YoY in September 2022 and recorded 7.6% YoY in October 2022, it remains above the upper limit of the South African Reserve Bank’s (SARB) inflation target band of 3%–6%.1 Still, South Africa’s headline YoY inflation has remained below that of the United States, European Union (EU), and the United Kingdom since February 2022,2 trending more in line with that of emerging market peers such as India and Brazil.3

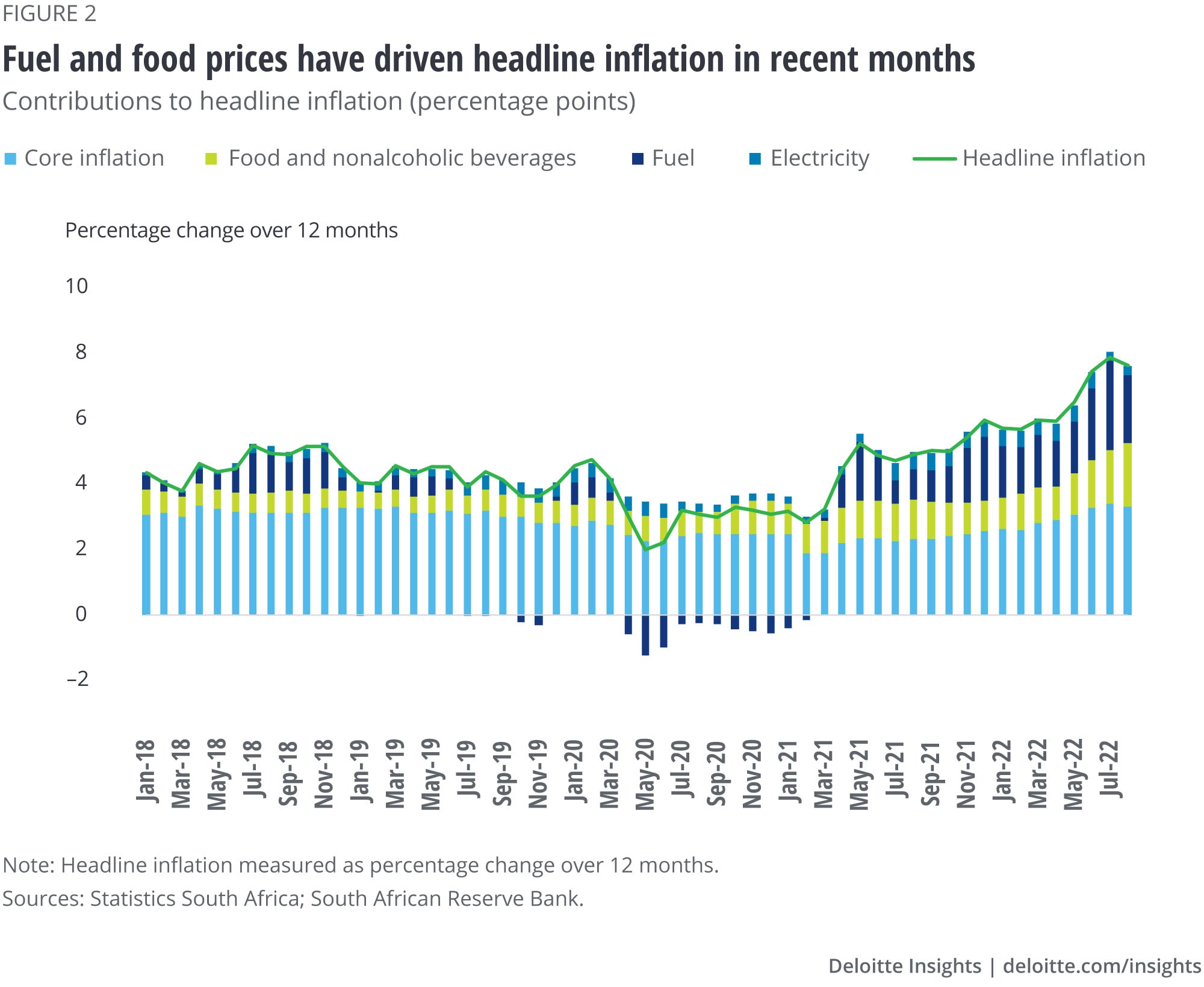

Since the beginning of 2022, South Africa’s headline inflation has been driven by global price increases in food and fuel (figure 2). This has affected the cost of living drastically, with household spending growth estimated to be less than 3% in 2022, and only 1.7% over the three years from 2022 to 2024.4 According to Deloitte’s Global Consumer Tracker for South Africa, financial stress is a key concern for South Africans given the cost-of-living squeeze: South African consumers surveyed at the end of October 2022 noted that they are delaying large purchases (51%), feel their financial situation has worsened over the past year (40%), and are concerned about their credit card debt (39%) and making upcoming payments (27%).5

Although headline inflation is expected to moderate in the next year as fuel and food prices moderate globally, the pressure on core inflation, which has been more subdued over the past year, could increase in 2023 as higher input costs are passed on to consumers.6 For example, producer price inflation for manufactured goods came in at 16.3% YoY in September 2022.7

Higher prices have not only resulted in a cost-of-living squeeze but also reduced the competitiveness of South African exports. The negative effect on economic activity is compounded by elevated interest rates, which are postponing investment, expansion, and resultant hiring decisions.

As seen in recent data (figure 1), the SARB expected inflation to fall sharply during the second half of 2022. While anticipated to average 6.5% for the 2022 calendar year previously,8 the SARB revised this by November end, and now expects inflation to average 6.7% for 2022, 5.4% for 2023, and to reach the 4.5% by Q2 2024.9

The SARB was among the first central banks to tighten monetary policy, raising interest rates to restore price stability, and to re-anchor inflation expectations. Between May and September 2022, the repurchase (repo) rate was raised by a cumulative 200 basis points to 6.25%—which was still 25 basis points below prepandemic rates.10 The SARB further hiked rates in late November by 75 basis points, bringing the repo rate to 7%.11

Against the backdrop of key advanced economies possibly entering a recession, and with the International Monetary Fund (IMF) downgrading global growth expectations to 3.2% for 2022 (from 4.4%) and to 2.7% for 2023 (from 3.8%), South Africa will be afforded little growth tailwinds from major trading partners going into 2023.12

China is expected to continue posting slow growth (less than 4% on average over 2022 and 2023), and anticipated recessions in major trading markets such as the United States, the Eurozone, and the United Kingdom will make export-led GDP growth difficult.13

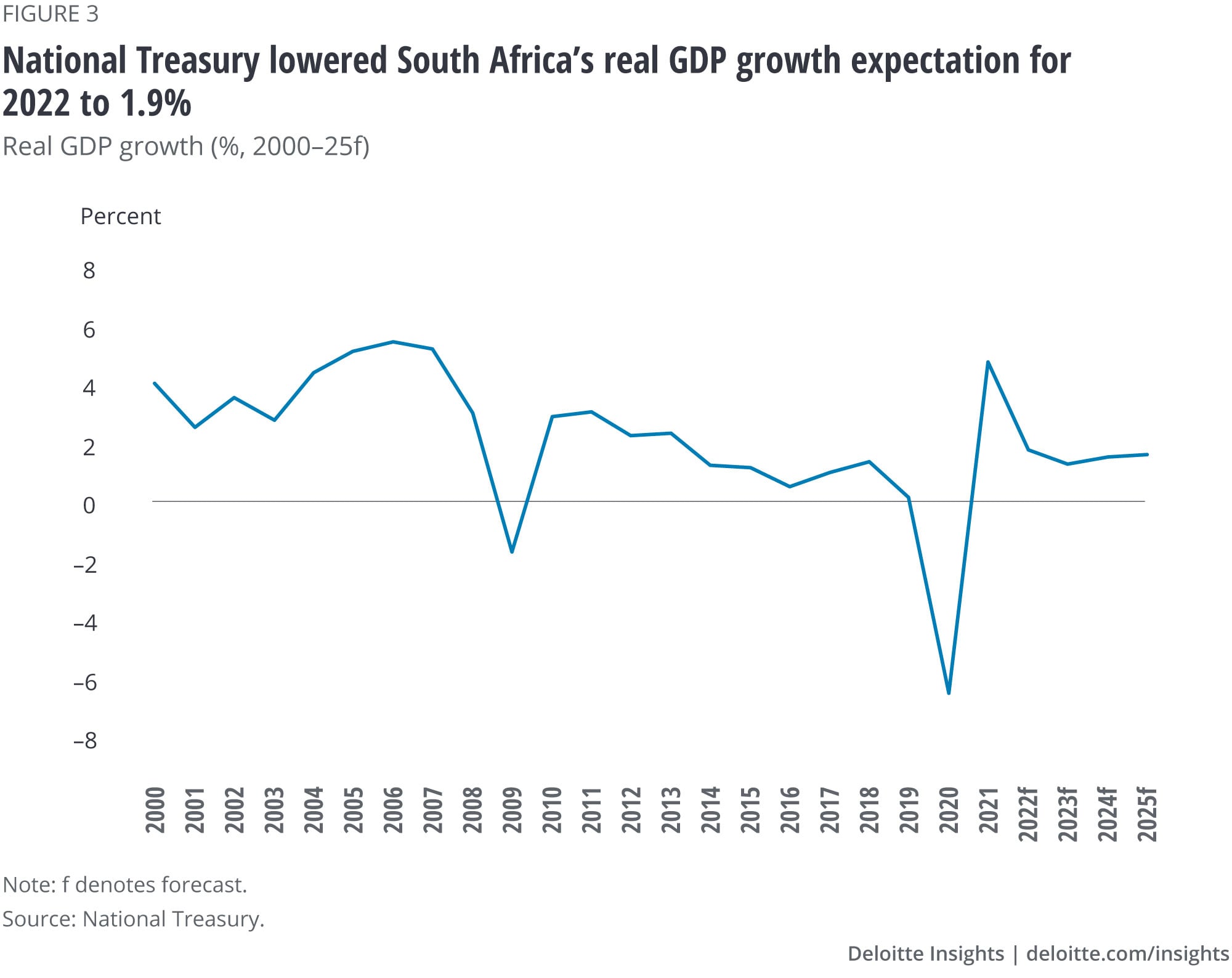

As such, South Africa’s 2022 GDP growth expectations have moderated from estimates earlier this year. National Treasury in October 2022 lowered its real GDP growth expectation for 2022 to 1.9% (from 2.1% in the 2022 Budget read in February-end) and 1.4% in 2023 (from 1.6%) (figure 3).14 The projected 2022 economic recovery from the pandemic was disrupted by the repercussions of the war in Ukraine and by devastating floods in the provinces of KwaZulu-Natal and the Eastern Cape, resulting in loss of lives, large-scale displacements, and the destruction of homes, while also impacting critical infrastructure such as roads and ports.15 This, together with industrial action in some sectors and “loadshedding,” resulted in a contraction in economic activity in Q2 2022 after a stronger-than-expected Q1.16

The difficulty to keep the lights on and power the economy is also compounding the weak growth outlook, with disruptions to operations and supply chains and limited business confidence delaying investments and net employment creation.17 In terms of foregone GDP from power cuts, 2022 is South Africa’s worst year on record. It is estimated that till October 2022, South Africans have already experienced more hours of loadshedding than in the previous eight years combined.18 The need to address this power crisis is urgent, and so is the need for implementing structural reforms, to spur expansion in job-creating sectors to meet the country’s development goals.19

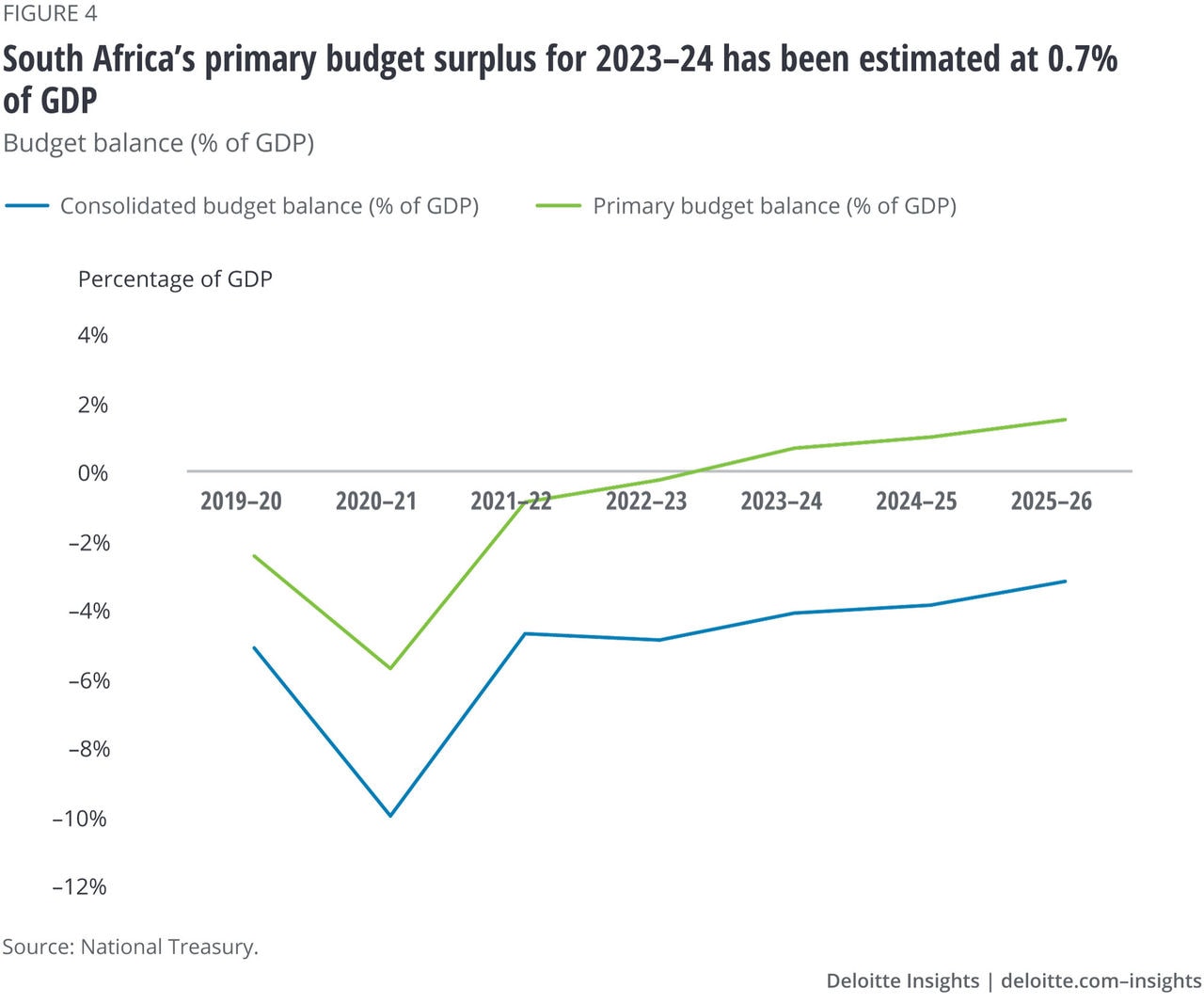

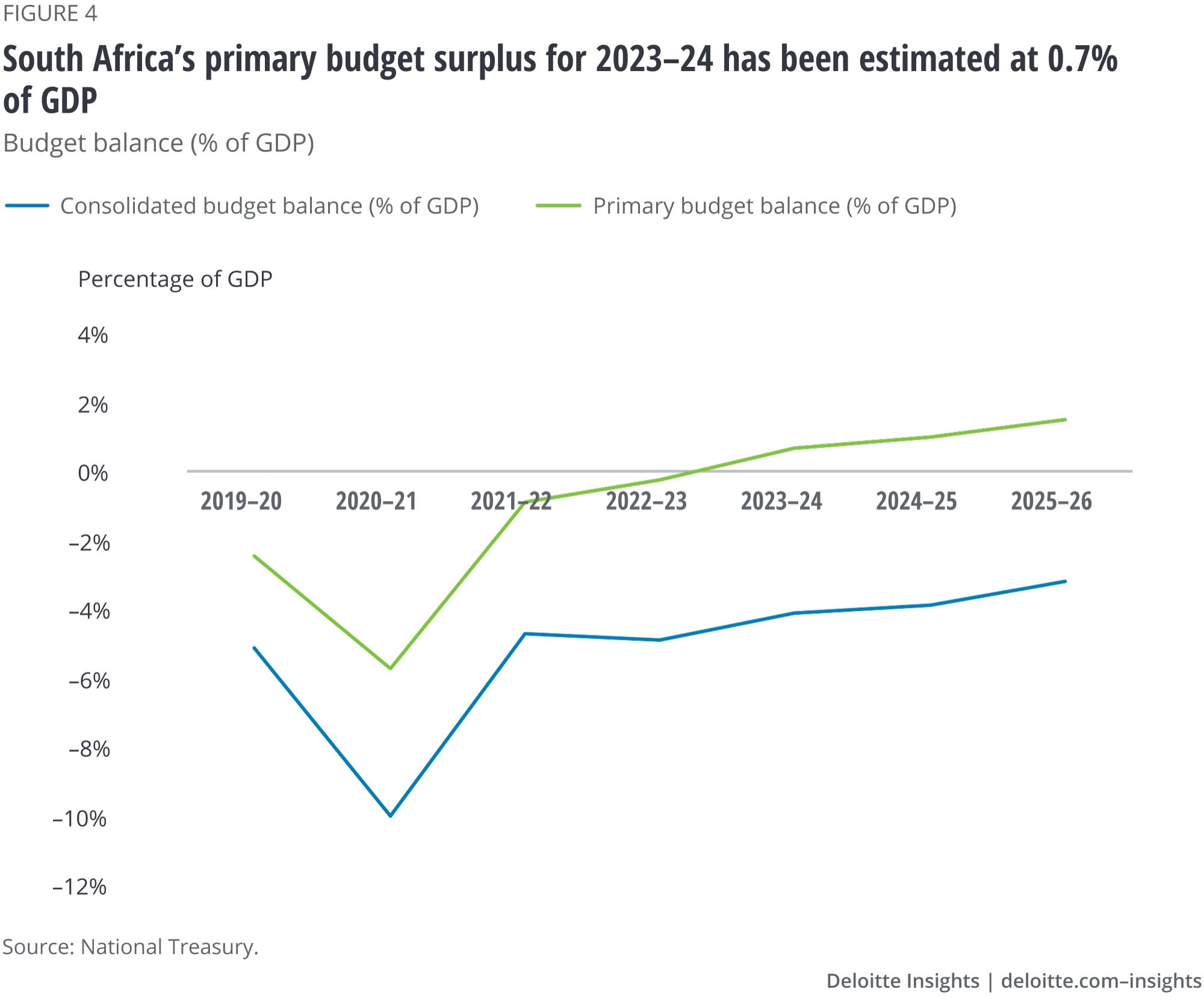

South Africa’s fiscal position—an important aspect of its macroeconomic policy and a key anchor for growth—has improved over the past two years. Fiscal consolidation measures such as budget discipline, together with better-than-expected tax collections, primarily driven by global commodities demand, have brought down the budget deficit. The budget deficit for 2022–23 has been revised down to 4.9% of GDP (from 6% in the 2022 Budget) and smaller deficits are forecast for the next three years, with a primary budget surplus (i.e., excluding interest payments) of 0.7% of GDP penciled in for 2023–24 (figure 4).20

Rightfully, the revenue windfalls are being used to reduce government debt, expected to now peak at 71.4% of GDP in 2022–23 before declining to about 65% in 2029–30, and to support reforms at crucial state-owned enterprises (SOEs).21 However, an overreliance on high commodity prices to bolster revenue collection is risky; so too is possibly higher-than-projected fiscal expenditure, particularly given pending public sector wage negotiations, the weak financial position and future bailouts of SOEs (despite conditions for funding to be put in place), and the continuation of the special COVID-19 grant, possibly in the form of a basic income grant.22

Overall investment has been declining in recent years, with gross fixed capital formation still below prepandemic levels. Investment has been driven by private investment, which remains below the targeted levels of investment. The already low public investment declined further given the focus on fiscal consolidation, but also hamstrung growth.23 However, national, provincial, and public entities’ spending on infrastructure, including roads, rail, and water projects, is expected to almost double during the 2022–23 to 2025–26 budget period.24 The energy sector reforms under Operation Vulindlela are expected to further encourage private investment.25 Creating an enabling environment conducive to investment, both domestic and foreign direct investment, is vital for the structural changes needed in the South African economy to accelerate growth and create jobs. While the appetite for investment is present (for example, R332 billion was pledged at the 2022 South Africa Investment Conference (SAIC), bringing the total amount committed since 2018 to R1.14 trillion26), more will need to be done to roll out important public sector infrastructure projects over the medium term.

While South Africa’s economic reform track record has been tenuous, and although prudent macroeconomic policy is supporting growth, a lack of business confidence, the power crisis, policy uncertainty, corruption, and no real new drivers of growth, together with the uncertain global backdrop and other risks such as a potential “greylisting,” continue to stifle the economic expansion needed to create employment and make a dent in poverty.

South Africa’s unstable electricity supply has been a key hindrance to investment, growth, and employment creation. Since 2011, South Africa has already gradually been diversifying its energy mix: the Renewable Energy Independent Power Producer Procurement Programme has resulted in about 6.5GW of renewable energy-generation capacity being procured by 2019, with a further 14.4GW of wind and 6.5GW of solar PV to be added by 2030 as per the country’s Integrated Resource Plan of 2019.27

The energy crunch has also seen the increase in the private-generation limit to 100MW with more private companies (as well as households) exploring opportunities to generate their own power (including rooftop solar), although the speed of adoption has been hampered by cumbersome approval processes. South Africa’s mining industry has been leading this trend, with plans underway for 89 renewable energy projects to be implemented by 29 mining companies, estimated at over R100 billion and with an electricity-generation capacity of 6.5GW.28

Besides the power shortfalls, for South Africa to honor its Paris Agreement commitments, the country’s coal-dominated energy mix will need to be diversified significantly over the next two decades.29 These demand- and supply-side drivers have seen shifts in new energy-generation solutions, particularly for renewables.

Indeed, organizations such as the IMF have mooted the global energy transition to net-zero emissions as a possible crucial driver of growth for the global economy over the coming decade, absent other notable tailwinds.30 This is happening as new and reconstituted energy systems, production methods, modes of mobility, and ways of consumption unfold globally.

And, South Africa, together with a number of other African economies, has massive renewables potential, not only in solar PV, CSP, and wind, but also in, for example, green hydrogen. However, challenges around transmission, general grid infrastructure, and minigrid, and other decentralization opportunities need to be addressed.

South Africa also has a notable comparative advantage in supplying key minerals and metals as part of the world’s clean-energy transition. The latter include, for example, platinum group metals (PGMs, used in catalytic agents in hydrogen electrolysis and fuel-cell applications), vanadium (input for long-duration battery energy storage applications), rare earth elements (REEs, used in permanent magnets in the electrical motors of wind turbines and in EV motors), and nickel (applications in EVs and battery storage, and hydrogen and geothermal technologies).31

Another key opportunity is the shift in demand in third markets, toward lower-emission products and services. One example is that of major export markets for South Africa’s car manufacturing industry—the United Kingdom and EU. Policy changes in these markets will prohibit the import of internal combustion engine (ICE) vehicles by 2030.32 As about three-quarters of cars manufactured in South Africa are destined for Europe, reconfiguring the automotive manufacturing landscape from ICE to EVs, alongside a comprehensive investment and tax system that will build a resilient raw material supply chain, will be important.

This will support the country’s efforts to remain globally competitive, retain access to major trading partners, and create new drivers of growth and employment opportunities to ensure a just and fair transition.33

Statistics South Africa (StatsSA), “Consumer price index (CPI),” October 2022, November 23, 2022.

View in ArticleSouth African Reserve Bank (SARB), Monetary policy review: October 22, October 2022.

View in ArticleIbid.

View in ArticleNational Treasury, “Medium-term budget policy statement—2022,” accessed November 24, 2022.

View in ArticleDeloitte, “Global State of the Consumer Tracker,” accessed November 24, 2022.

View in ArticleSARB, Monetary policy review: October 22.

View in ArticleStatsSA, Statistical release: Producer price inflation, September 2022, accessed November 24, 2022.

View in ArticleSARB, “Statement of the Monetary Policy Committee,” press release, November 24, 2022.

View in ArticleIbid.

View in ArticleSARB, Monetary policy review: October 22.

View in ArticleSARB, “Statement of the Monetary Policy Committee.”

View in ArticleInternational Monetary Fund, Regional economic outlook October 2022: Living on the edge, October 13, 2022.

View in ArticleIbid.

View in ArticleNational Treasury, “Medium-term budget policy statement—2022.”

View in ArticleSouth African Government, “President Cyril Ramaphosa: Declaration of a national state of disaster to respond to widespread flooding,” speech, April 18, 2022.

View in ArticleNational Treasury, “Medium-term budget policy statement—2022.”

View in ArticleStatsSA, “Quarterly employment statistics (QES)—Q2: 2022,” media release, September 27, 2022.

View in ArticleBusiness Tech, “New data reveals ugly truth about load shedding in South Africa,” October 9, 2022.

View in ArticleNational Treasury, “Medium-term budget policy statement—2022.”

View in ArticleIbid.

View in ArticleIbid.

View in ArticleIbid.

View in ArticleSARB, “Statement of the Monetary Policy Committee.”

View in ArticleNational Treasury, “Medium-term budget policy statement—2022.”

View in ArticleSouth African National Treasury, Operation Vulindlela progress update—2022/23: Q2 report, June 2022.

View in ArticleSouth African Investment Conference, “Home,” March 24, 2022.

View in ArticleGreen Cape, South Africa renewable energy masterplan, accessed October 5, 2022.

View in ArticleHalima Frost, “Private sector investments key for JET,” Mining Weekly, October 28, 2022.

View in ArticleJonathan Giliam and Hannah Marais, Building climate resilience: Opportunities and considerations for Africa in a net-zero future, Deloitte, accessed November 24, 2022.

View in ArticleIMF, World economic outlook: October 2022, November 2022.

View in ArticleDeloitte, Africa’s role in a clean energy future, accessed November 24, 2022.

View in ArticleJonathan Giliam and Hannah Marais, Building climate resilience: Opportunities and considerations for Africa in a net-zero future, Deloitte, accessed November 24, 2022.

View in ArticleIbid.

View in ArticleThe authors would like to thank Santhuri Padayachee for her assistance with research.

Cover image by: Jaime Austin