{kind=link}

{kind=link}

Infrastructure investment: An economist’s view from the ground up has been saved

Cover image by: Sanaa Saifi

Postpandemic recovery strategies in the developed world have a common thread running through them—proposals to increase spending on infrastructure. Germany, France, and Italy have announced proposals to spend part of their respective shares of the European Union’s recovery plan on infrastructure.1 Japan and Canada have also joined the infrastructure train.2 And of course, there is the United States, arguably at the forefront of infrastructure investment proposals. Three factors are at the core of this rare synchrony across countries: the need to boost growth in the short term and rejuvenate productivity in the long term, historically low borrowing costs, and the fact that infrastructure spending as a share of GDP has fallen over decades. These factors should buttress the prospect that infrastructure investment proposals—still under consideration and usually difficult to bring to complete fruition—will be at least partially implemented.

The infrastructure spending proposal in the United States—likely running into trillions of dollars—has been in the spotlight because of its sheer magnitude and scope. In this paper, we revisit the case for increased infrastructure investment in the United States. We also touch upon important questions: How big is the infrastructure gap? And what does infrastructure investment mean for growth and productivity? Finally, we raise questions about the direction and scope of possible infrastructure spending in the future.

The definition of infrastructure is not an exact science. In 2017, when there was much hullabaloo about investment in infrastructure in the United States, we published an overview of what constitutes infrastructure.3 Infrastructure refers to the fixed assets that are essential to the everyday functioning of the economy—equipment and structures that include transportation, roads, bridges, sewer systems, water supply, power supply, and communication, including structures essential to the functioning of the internet. Refer to the sidebar, “What is infrastructure?” for a more detailed explanation.

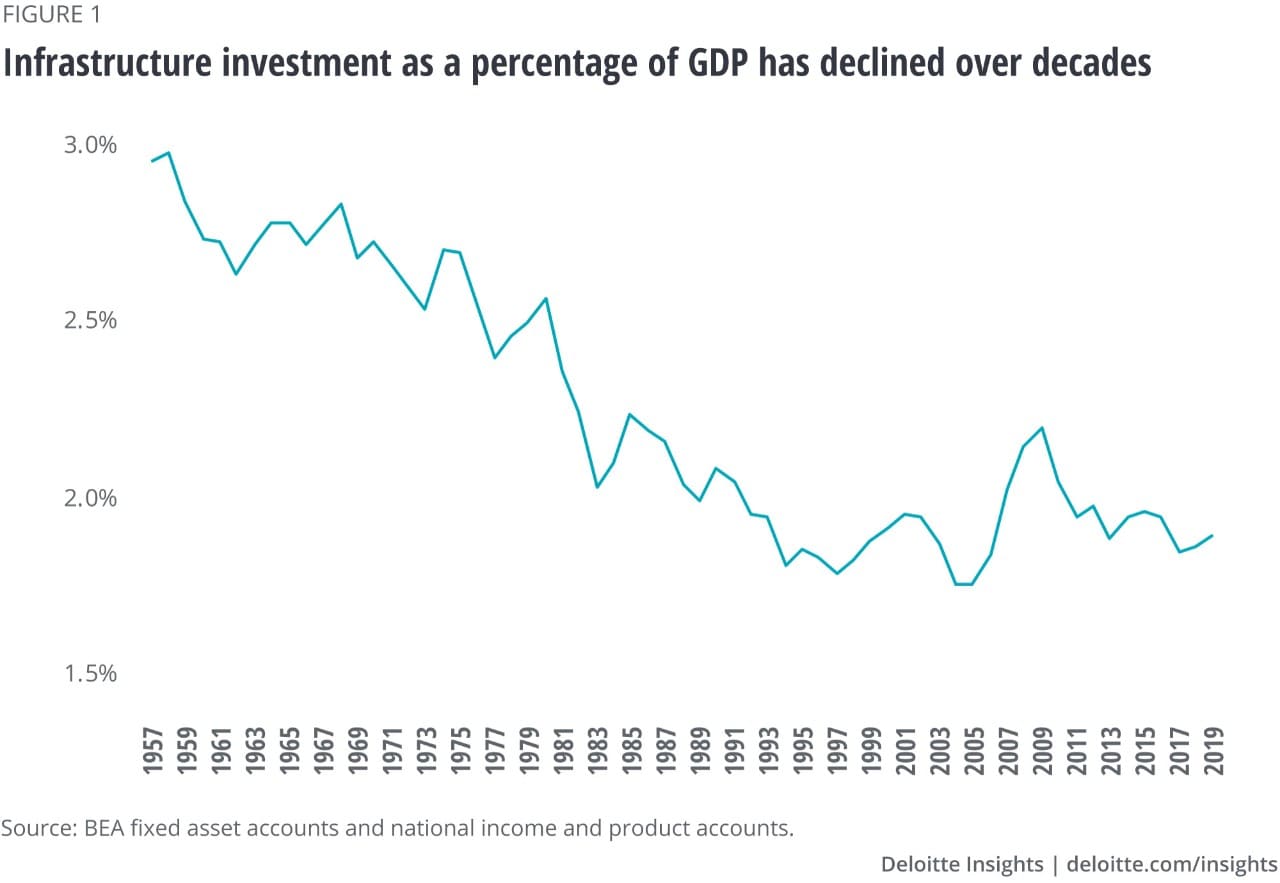

Infrastructure investment as a share of GDP in the United States has fallen since the early 1960s (figure 1). This implies that as the economy has grown, existing infrastructure has been used more intensively. And conceptually, infrastructure is more valuable the more it is used. But overuse without sufficient investment in repairs and expansion could cause existing infrastructure to crumble. Run-down or insufficient infrastructure can make it difficult for goods and services to transition from one stage of value addition to the next. At scale, this can erode productivity and limit future economic growth. This sets the context for renewed investment in infrastructure in the United States.

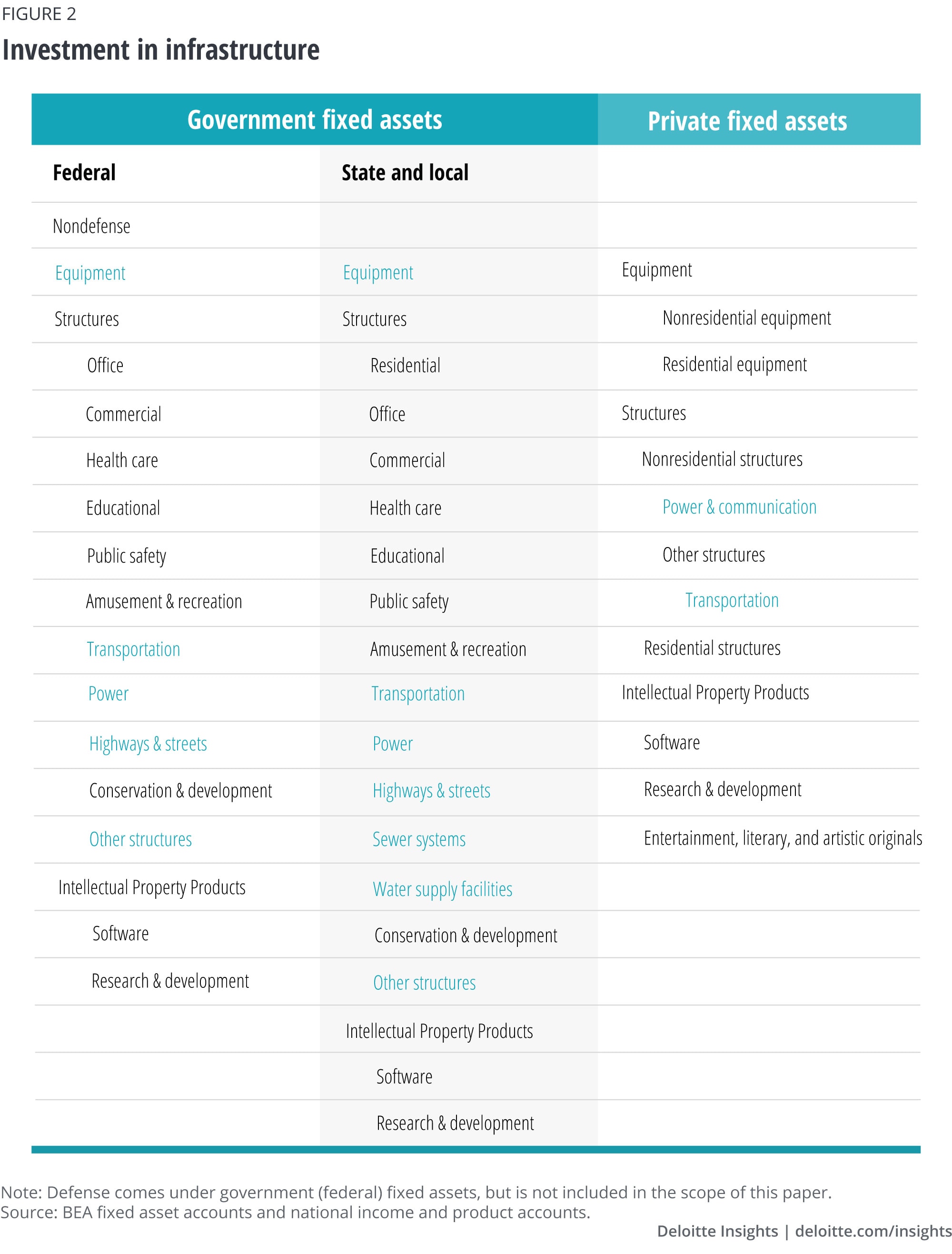

Government-owned fixed assets in the United States are either owned by the federal government or state and local governments. Federal government–owned fixed assets are classified as either defense or nondefense. We have excluded defense fixed assets when speaking about infrastructure in this paper. Nondefense fixed assets are further classified as equipment, structures, or intellectual property. Similarly, state and local government–owned fixed assets are also classified as equipment, structures, and intellectual property. Privately owned fixed assets follow the same broad classification. For the most part, private fixed assets fall outside the definition of infrastructure because use is limited by ownership. Private power and communication structures, as well as transportation structures, are the exception, and are therefore included within the definition of infrastructure.

The highlighted items in figure 2 are included in our definition of infrastructure for the purpose of this paper.

Investment in infrastructure

Gross investment is the value of purchases of new fixed assets and net purchases of used assets at depreciated cost from other types of owners (private business, governments, households, and nonresidents). We measure investment in infrastructure by considering annual spending on the fixed assets highlighted in figure 2.

Data on investment in infrastructure is sourced from the BEA’s Fixed Assets Accounts. Data on GDP is sourced from the BEA’s National Income and Product Accounts. We use this data to calculate the ratio of investment in infrastructure:GDP in figure 1.

The declining share of infrastructure investment in GDP sets the context but does not solidify the case for increased investment in infrastructure. Reports on the state of infrastructure make a stronger pitch. The most widely cited report—from the American Society of Civil Engineers (ASCE)—grades infrastructure in the country. America’s overall grade for infrastructure has hovered between “D” (indicating poor infrastructure) in 1998 and “C-” (indicating mediocre to poor infrastructure) in 2021.4 The country’s infrastructure grade remained unchanged between 2006 and 2010, despite an increase in infrastructure spending during the period. Perhaps this was because of the magnitude of infrastructure funding required. The bill is likely to keep growing the longer it remains unaddressed. The latest ASCE report highlights that 43% of public roads in the country are either in poor or mediocre condition, 7.5% of bridges are structurally deficient, and there is a water main break every two minutes.5 In 2021, the ASCE estimates that based on current trends in infrastructure investment, the funding gap for physical infrastructure in the United States over a 10-year period is approximately US$2.1 trillion.6

Analysis by the Brookings Institution shows that the share of operation and maintenance spending in total public infrastructure spending in the United States has grown steadily, while the share of capital spending has fallen.7 This trend, which intensified over the last decade, not only points to a growing focus on maintaining existing infrastructure, but also to the deterioration of aging infrastructure in the country. The relatively large infrastructure proposal could play a role in reversing this deterioration. At the time of writing, the proposal stands between US$973 billion and US$1.2 trillion, depending on whether it extends over a period of 5 or 8 years.8 However, only about 60% of the proposal will be new funding—the remaining 40% will be recurring funding. The proposal seeks to address physical infrastructure, the kind that aligns closely with the definition used in this paper. If signed into law, focus will likely shift to the implications for short-term growth and long-term productivity.

The nature of infrastructure spending is pivotal to answering questions about its impact. Spending is either channeled to repair or to build. While repair is usually “shovel ready,” building new infrastructure often requires a longer gestation period. The different nature of these two channels results in differing impacts. Repair puts people to work and boosts growth in the short term. Building can place infrastructure in growth areas. Both are important for the process of value addition, improving productivity, and the economy’s potential for growth. Other factors that determine the degree of impact of infrastructure spending are where infrastructure is repaired or expanded, and the intensity with which infrastructure is likely to be used in the future.

Economists have long tried to quantify the impact of public infrastructure spending on the US economy. A series of landmark studies by David Aschauer between 1988 and 1990 argued that much of the decline in productivity in the United States in the 1970s was triggered by declining rates of public capital investment. According to Aschauer’s study, a US$1 increase in the stock of public infrastructure in 2019 would increase the level of private production by 66 cents in the long run.9 Other studies that span beyond the United States suggest a lower responsiveness of output to infrastructure. A meta study by Pedro Bom and Jenny Ligthart in 2009, which aggregated almost three decades of studies on the topic, proposed that the long-run impact of an additional dollar in public infrastructure in 2019 was in the range of 28–36 cents. Even if the impact isn’t as large as David Aschauer claimed, the study highlights that investing in infrastructure has a positive and significant impact on economic output.10

Two factors will likely play a role in determining the true impact of infrastructure spending in the years to come. First, of course, is just how low the current state of infrastructure is relative to its optimal level. But second, there may be significant changes in the nature of infrastructure in the postpandemic world (read The postpandemic economy: How we work for insights into how changes to the way we work are creating broad ripple effects).

Two key themes are likely to play a role in refining how we think of infrastructure in the future.

• The accelerated adoption of digital technology. Everything is digital these days, and infrastructure is no exception. From smart grid applications for managing electricity usage to road metering systems, what was once a question of steel and concrete is now a matter of silicone chips and software. That’s especially true for cybersecurity, something that didn’t exist just a few decades ago—and is likely to become increasingly important in the future.

• A growing focus on environmental sustainability and climate change. The transition away from fossil fuels to renewable sources of energy would likely require the replacement of large sections of existing power infrastructure (for more on the economic implications of a low-carbon future, do read Facing the heat).

These factors are likely to shape the infrastructure debate globally, not just in the United States. The global economy has been playing catch-up for a while. ¬¬The Global Infrastructure Hub—a G20 initiative—projects that if countries continue to invest in infrastructure in line with current trends, then the global infrastructure shortfall over the next 20 years will be nearly US$13 trillion. Add the infrastructure needed to meet sustainable development goals and the gap rises to more than US$15 trillion.11 The current infrastructure bill may just be a down payment on true global infrastructure needs.

Cover image by: Sanaa Saifi