Article

Deloitte 2024 Q2 CFO Express

Issue No. 14

Published date: 13 June 2024

Explore Content

- Play this episode

- Policy support to reignite animal spirits

- Tech Trends 2024: six macro technology forces critical to business

- Stability and progress: Deloitte China releases Chinese Banking Industry 2023 Review and 2024 Outlook

- Deloitte China releases Consumer and Retail Industry Outlook 2024, highlighting new consumption trends

- How can China build more world-class enterprises? Deloitte proposes a new blueprint

- Deloitte Global Chief Procurement Officer Survey: procurement as orchestrators of value

- Sustainability report guidelines for listed companies officially released

- Deloitte's 2024 Gen Z and Millennial Survey finds these generations stay true to their values as they navigate a rapidly changing world

China's real GDP growth recorded 5.3% yoy in the first quarter of 2024, reflecting the trend of a gradual recovery or at least stabilization. April's PMI index was 50.4, indicating an expansion in overall economic output. Since April 2024, a new round of policy support to the real estate sector is being rolled out, which ought to address both supply and demand sides. In terms of trade, so far China's external sector has not been adversely affected by the renminbi's relative strength as seen in Q1 export data. As protectionism in the North American market rises (with the US announcing tariffs on Chinese electric vehicles in May), China's EV makers and export businesses will need to penetrate further into the Global South and Europe.

Social, demographic changes, and technology upgrades are significantly influencing development strategies of businesses. For example, with fewer children and an aging population, demand for pets, companionship, entertainment, and health and wellness products and services will continue to grow. Business opportunities will arise around the needs of single-person households and women's self-indulgent consumption. Companies will no longer overly focus on investing in individual emerging technologies but will need to strike a balance between technology investment, strengthening of basic infrastructure, core systems, and team building. Furthermore, as Chinese companies continue to expand abroad, they will need to establish a competitive advantage on a global scale through enhancing their strategic planning, management, and other core capabilities.

- In the next 18-24 months, what are the key technology trends that companies shall closely monitor for their technology investments?

- With China's consumer market having stabilized and rebounded, which consumption niches are experiencing rapid growth? What consumption trends will emerge in the future?

- How is 'world-class enterprise' defined? What are the ways to build world-class enterprises with Chinese characteristics?

- The shared goals of the Chief Financial Officer (CFO) and Chief Procurement Officer (CPO) in cost control and risk management are driving closer collaboration between the two. What strategies can companies adopt to elevate the strategic positioning of the procurement function and make it a driving force for value creation in the enterprise?

- With the release of guidelines on sustainable development reporting for listed companies, what preparations shall companies make?

This issue of CFO Express focuses on the above issues, and we hope that these excerpts and summaries will provide new insights and ideas for corporate decision-makers.

Chief Economist's View |

|

Trends and Outlook |

|

Expertise and Practice |

|

Talent and development |

Chief Economist's View

Chief Economist's View

Policy support to reignite animal spirits

Deloitte China's Chief Economist, Sitao Xu, shares his perspectives on the first quarter's economic performance as well as full-year outlook. His main takeaways are:

- A tentative cyclical recovery is underway in China, but consumer confidence is still being hamstrung by the slow pace of recovery and a slumping property sector. The good news is that PMI readings for April by the National Bureau of Statistics came in at a respectable 50.4, reinforcing the trend of a gradual recovery or at least stabilization. The strong Q1 growth of 5.3% brings the 2024 growth target of “around 5%” well in reach.

- Policy support to the real estate sector has gathered momentum as of April 2024. Specifically, meaningful policy support which ought to address both supply and demand is currently being rolled out. On the demand side, several cities have removed restrictions on housing purchases. In our view, it is only a matter of time until the remaining restrictions are inevitably phased out. On the supply side, the government has made it explicit that the guaranteed delivery of housing units will be ensured.

- Renminbi has been held steady this year and China's external sector has not been adversely affected by the renminbi's strength. The risk for China's external sector is looming protectionism, not reduced competitiveness. As protectionism in the North American market increases (the U.S. government announced on May 14th that it would impose tariffs on Chinese EV products), Chinese EV makers will need to penetrate further into the Global South and Europe.

More information: The Deloitte Research Monthly Outlook and Perspectives (Issue 90)

Trends and Outlook

Trends and Outlook

Tech Trends 2024: six macro technology forces critical to business

Deloitte has released its 'Tech Trends 2024' report, titled 'Generative AI: force multiplier for human ambitions,' advising businesses not to overly focus on individual emerging technologies at the expense of a holistic view. The report encourages companies to strike a balance between investing in new technologies and strengthening their infrastructure, core systems, and technical teams to create differentiated advantages with innovation. The 'Tech Trends 2024' report highlights six key technology trends that will be crucial for business transformation and upgrades in the next 18-24 months:

Three elevating forces - interaction, information, and computation

1. Spatial computing and industrial metaverse empowering industrial production interaction: Many companies are leveraging the industrial metaverse to power a wide range of use cases, such as digital twins, spatial simulations, augmented work instructions and collaborative digital spaces. This allows more traditional knowledge workers to benefit from immersive 3D interaction. Additionally, the growing availability of high-fidelity 3D digital assets and hardware is paving the way to an operationalized spatial web.

2. Generative AI as growth catalyst: With enhanced computing power, better training data, and clever coding, generative AI technologies can imitate human cognition in a number of ways. In industrial environments, generative AI can create the opportunity for huge productivity and efficiency gains. The key question for the future is how this capability will impact the business environment broadly.

3. Beyond brute force compute: For the cutting-edge cases that drive competitive advantage, the cloud services' new need for specialized hardware is emerging. Training AI models, performing complex simulations, and building digital twins require different types of computing power. Leading business today are finding new ways to get more out of their existing infrastructure and adding cutting-edge hardware to speed up processes of constructing computing power.

Three Grounding Forces - business of technology, core modernization, and cyber & trust

4. From DevOps to DevEx: empowering the engineering experience: In most companies, developers typically spend only 30% to 40% of their time on feature development. Companies that are dedicated to attracting and retaining the best technical talent are increasingly focusing on the developer experience, or a developer-first mindset that aims to improve their day-to-day productivity and satisfaction ('DevEx') by considering their every touchpoint with the organization.

5. Defending reality: truth in an age of synthetic media: With the proliferation of AI tools, it is now easier than ever for bad actors to impersonate and deceive their targets. Leading organizations are implementing a range of policies, strategies, and technologies to identify harmful content and make their employees more aware of the risks.

6. Core workout: from technical debt to technical wellness: Companies that want to lead in the future need to forgo piecemeal approaches to technical debt for a new holistic frame of technical wellness. Preventive wellness assessments, rooted in business impact, can help teams prioritize the areas of the tech stack that need treatment.

More information: 2024 Tech Trends

Stability and progress: Deloitte China releases Chinese Banking Industry 2023 Review and 2024 Outlook

In 2023, amidst a complex international environment and numerous domestic reform and development tasks, the Chinese banking industry delivered a "stabilizing and progressing" answer sheet. Deloitte publishes the report 'Chinese Banking Industry 2023 Review and 2024 Outlook,' which analyzes the performance of 10 representative domestic commercial banks, showcasing the achievements of the Chinese banking industry in 2023 and its future development.

In terms of "stability," Chinese banks faced some pressure in areas such as capital supplementation, profitability, real estate loans, and risk resolution of local government debt. However, their fundamentals remained stable and demonstrated a good ability to withstand risks. As an economic ballast, the Chinese banking industry continued to increase its credit extension and optimize its credit structure. The assets of large banks grew rapidly, driving the banking industry's asset growth rate to 9.9%. Despite the fast growth in asset-liability size, the banking industry's overall operation was stable, with a non-performing loan ratio of 1.62%. The provision coverage ratio and the liquidity coverage ratio remained in a healthy range. Although asset size maintained steady growth, the uncertainty of economic recovery prospects posed various challenges to banks' credit extension and credit risk management. Due to a number of factors, including narrowing interest rate spreads, the decline in the scale of wealth management products amid capital market volatility, and sluggish consumer market recovery, the growth rate of key profitability indicators slowed down significantly.

In terms of "progress," under the development goal of building the financial sector to provide strong support for building China into a strong country, the strategic blueprint for "fintech, green finance, inclusive finance, elderly care finance, and digital finance" has initially taken shape. The financial regulatory system and mechanisms have been further refined and made more efficient, creating a favorable institutional environment for high-quality development of the banking sector. In 2023, the Chinese banking industry achieved over 20% growth in green and inclusive loans, high-tech manufacturing, and tech-based SME loans, as well as loans for the elderly care sector. The Chinese banking industry has continued to increase its investment in the area of fintech, and the application of advanced digital technologies such as intelligent services, intelligent operations, and intelligent risk control has further enhanced the service quality, operating efficiency, and risk control of the Chinese banking industry.

Looking ahead to 2024, opportunities and challenges coexist for the Chinese banking industry. With continuous consolidation of China's economic recovery, effective enhancement and release of residents' consumption demand, gradual mitigation of real estate investment risks, and continuous resolution of local government debt risks, the Chinese banking industry is expected to resolve risks from their origins, comprehensively repair and improve the quality of its assets and liabilities, and achieve a better balance of profitability, liquidity, and security.

Deloitte China releases Consumer and Retail Industry Outlook 2024, highlighting new consumption trends

2024 is the year of consumption promotion, and China's consumer market has stabilized and rebounded, driven by a series of policies. Deloitte's latest report, "China consumer goods and retail industry outlook 2024: insights into industry new trends amidst changing consumption structures," provides an in-depth analysis of the performance of nearly 600 listed consumer goods and retail companies, revealing the development trends in various sub-sectors of this industry and capturing the factors driving industry performance.

Entering 2024, most sub-sectors of consumer goods and retail formats have seen accelerated growth. Specifically, lifestyle consumption that meets consumers' self-indulgent, social, and immediate needs has maintained rapid growth. For example, tobacco and alcohol consumption has maintained double-digit growth, and the growth rates of grain, oil, food, beverages, and cosmetics are higher compared to the same period last year, and these categories are expected to maintain rapid growth. Traditional consumer goods industries like home appliances and dairy products maintain low growth rates. However, they may see new development opportunities in the future under the stimulus of the national policies such as promoting the trade-in of consumer goods and growing demand for green and healthy products. In terms of retail formats, consumers' preference for multi-channel shopping has deepened, resulting in a less-than-expected recovery of traditional offline businesses, including specialty shops and supermarkets. In the first half of 2023, department store achieved only a low single-digit growth rate. Compared with the traditional offline industry, the penetration rate of e-commerce continues to rise. As e-commerce companies accelerate their presence in new formats and lower-tier markets, the revenue scale of China's e-commerce industry will maintain an upward trend. By the end of 2023, the number of domestic e-commerce live-streaming users reaches nearly 600 million, and the penetration rate of e-commerce live-streaming users increases from 44.6% at the end of June 2022 to 54.7%.

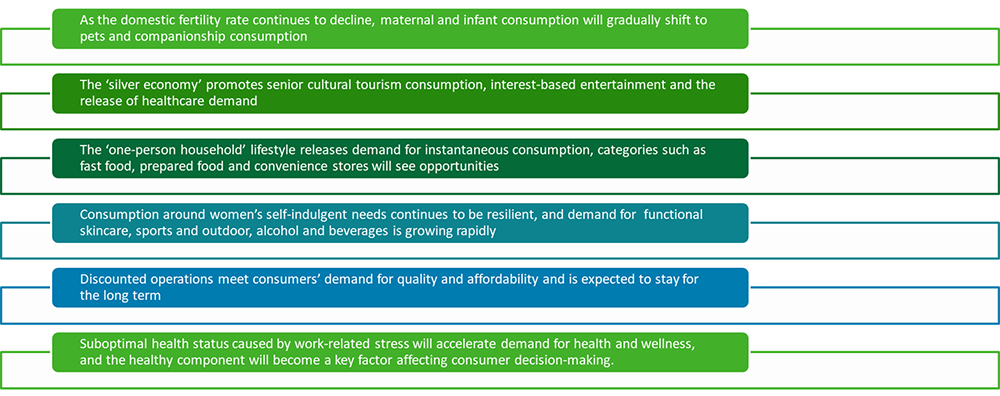

Currently, changes in demographics, family structures, and lifestyle are driving a new round of consumption structure reforms, which has given rise to the 'silver hair' economy, 'she' economy, health economy and leisure economy, bringing new development opportunities for the industry. For example, with the social trends of fewer children and an aging population, the demand for pet, companion, entertainment, and health care products will continue to be released. The development of "one-person household" and women's "self-indulgent" consumption are also expected to bring opportunities. Discounted operations meet consumers' demand for quality and affordability and may stay for the long term.

Graph: New consumption trends

Expertise and Practice

Expertise and Practice

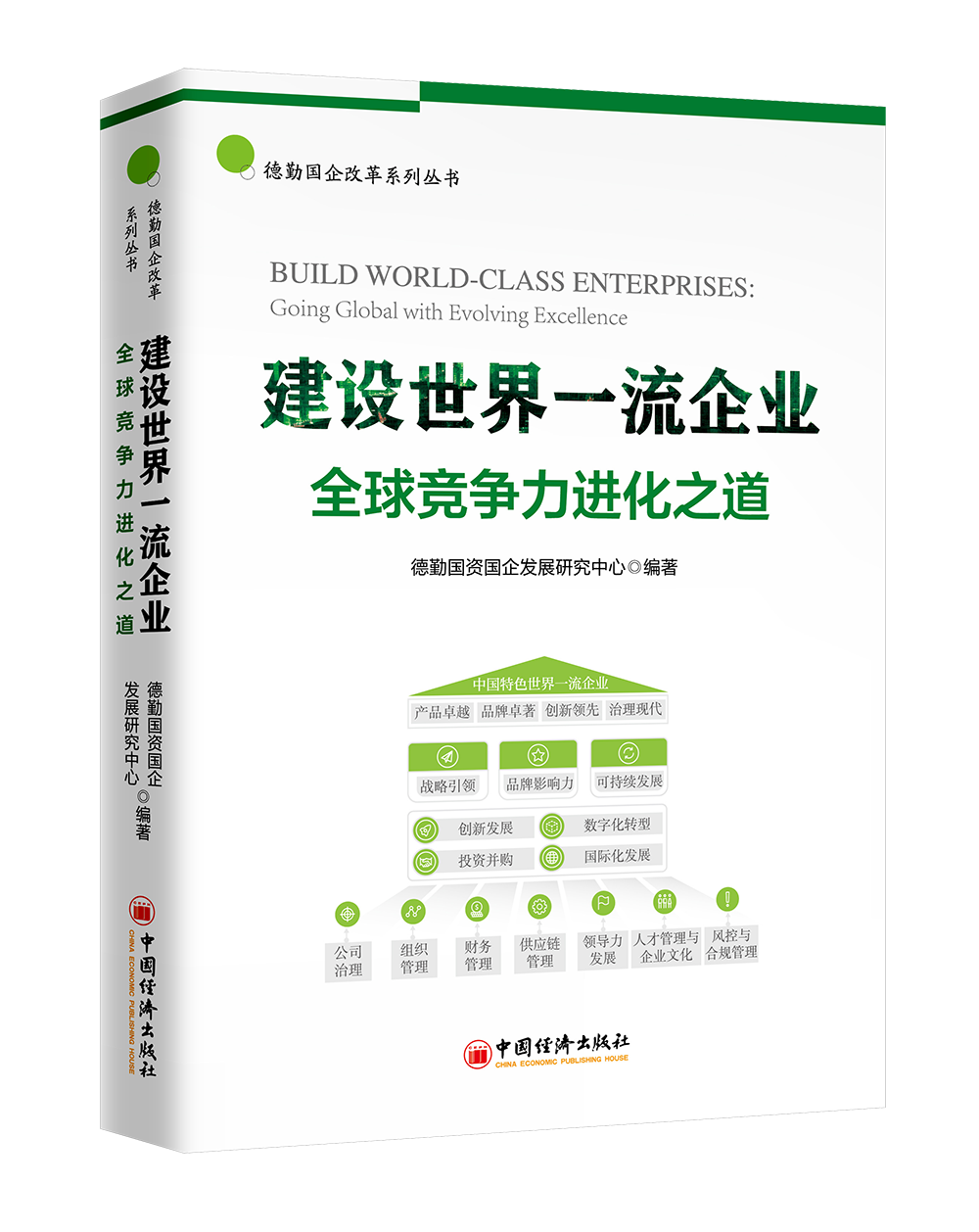

How can China build more world-class enterprises? Deloitte proposes a new blueprint

In April 2024, Deloitte published a new book titled 'Building a world-class enterprise: the evolutionary path of global competitiveness,' which comprehensively and systematically analyzes the experiences and leading practices of world-class enterprises and upgrades the framework of core competency elements of world-class enterprises in conjunction with the national guidelines on 'Accelerating the Building of World-Class Enterprises.' Commissioned by the State-owned Assets Supervision and Administration Commission of the State Council, Deloitte China has long supported the building of world-class enterprises as a professional think tank and has been conducting research on 'World-Class Enterprise Standards' since 2011. The research results have been compiled and published as books in 2013 and 2019, and have become widely read, used, and recommended as reference books in the reform of state-owned enterprises.

There is no unified international standard for "world-class enterprises," and it is more of a practical guideline that is constantly summarized and dynamically updated based on the best practices of leading companies in various industries. Deloitte understands "world-class" from three perspectives: first, the company's business scope expands from domestic to global; second, the company learns from advanced practices worldwide; and third, Chinese companies need to compete and cooperate with world-class enterprises. Therefore, the book's key proposition is that only by keeping up with world-class enterprises through benchmarking can there be an opportunity to meet the standard of world-class enterprises, and then continuously set standards, export models and standards and lead development. The book is divided into three chapters, which explain the connotation and construction path of becoming world-class enterprises with Chinese characteristics from three aspects:

The first chapter, "Becoming a World-Class Enterprise: Concepts and Trends," focuses on analyzing the current uncertainties in the global economy, the reconstruction of the global value chain, and the challenges that enterprises face under China's development model. It also clarifies the reasons for China to accelerate the construction of world-class enterprises and updates the "Framework of Core Capability Elements for World-Class Enterprises."

The second chapter, "Core Capabilities of World-Class Enterprises: Practices and Cases," summarizes the best practices, reference benchmarks, and successful cases for each capability element in the "Framework of Core Capability Elements for World-Class Enterprises." Among them, value realization, value-driven, and value assurance are the three core capabilities that are the breakthroughs for Chinese enterprises to achieve maximum value creation in the next ten years.

The third chapter, "Building World-Class Enterprises and Realizing Value Creation: Methods and Paths," clarifies the methods and paths to build world-class enterprises with Chinese characteristics. Chinese enterprises must establish a mindset of "benchmarking, meeting the standard, and setting the standard", place themselves in a competitive environment, and reflect on their situation through benchmarking against world-class enterprises, ultimately integrating "world-class" mindset into the enterprise's strategy.

Deloitte Global Chief Procurement Officer Survey: procurement as orchestrators of value

In the context of enterprises facing multiple challenges such as supply chain risks, rising costs, and declining growth, Chief Financial Officers (CFOs) and Chief Procurement Officers (CPOs) are having deeper and closer collaboration, based on common goals in the areas of cost control and risk management, including topics such as management of both fixed expenses and variable costs, supply chain risks, ESG compliance, and digital transformation. Collaboration between the two will give the procurement function more strategic positioning and help it become a driver of organizational value creation. Deloitte's 'Global Chief Procurement Officer Research Report 2023' points out that as the scope of the procurement function continues to expand beyond cost control, procurement's working model has shifted from passive-responsive to business-enabling. CPOs are evolving into orchestrators of enterprise value and help build competitive advantage by collaborating with internal organizations and managing external suppliers. The research shows that implementing procurement operations, talent management and digital transformation are the top three strategies for CPOs to achieve excellence:

- A more agile procurement operating model: To reduce the time taken up by transactional processes and free up more energy to focus on strategic activities and procurement organizations. CPOs can proactively use a hybrid operating model (outsourcing/BPO) for flexible workforce deployment; centralize category management/supply development, source-to-contract, procure-to-pay, and supplier relationship management processes; and manage potential workload fluctuations through the adoption of flexible automation tools to improve the standardization of policies, processes, systems, and data.

- More flexible talent management strategies: On the one hand, by implementing flexible talent development programs, CPOs can focus their training on new experiential skills, such as digitization-related data and analytical abilities. Research shows that organizations that adopt a skills-based talent strategy are more likely to retain high-performing talent. On the other hand, to break down functional silos, the procurement department could adopt a higher degree of cross-functional and cross-organization collaboration, as well as better cross-training.

- More Effective Digital Transformation: Digital transformation is a key strategy for improving efficiency and capabilities, while poor data quality remains the primary factor hindering digitization. CPOs should value the analysis of spend/savings performance, supplier risk and supply market intelligence, leverage analysis to improve decision-making and business performance, and continuously improve data quality.

Sustainability report guidelines for listed companies officially released

In April 2024, with the unified deployment of the CSRC, SSE, SZSE and BSE formally issued the Guidelines on Sustainability Report for Listed Companies (collectively referred to as the 'Guidelines'), which will come into effect on 1 May 2024. The Guidelines require multiple index constituent companies and companies listed simultaneously in Chinese Mainland and overseas markets to disclose their 2025 sustainability reports for the first time by 2026 and encourage other listed companies to also voluntarily publish their Sustainability Reports. The issuance of the Guidelines regulates the disclosure of sustainability information on environmental, social and governance of listed companies in China, specifies the scope of the first batch of mandatory implementation, and leads to the standardized development of sustainability information disclosure of listed companies and other market entities through the demonstration effect. Deloitte's interpretation of the key points of the Guidelines is as follows:

- Disclosure framework: For topics with financial materiality, the Guidelines require disclosing entities to analyze and disclose four core elements of 'governance, strategy, impact, risk and opportunity management, as well as metrics and targets'.

- Specific topics: The Guidelines set 21 specific topics for environmental, social and sustainability-related governance, and set differentiated disclosure requirements for different topics through a combination of qualitative and quantitative approaches, as well as mandatory and encouraging approaches.

- Double Materiality Principle: As shown in the Exposure Draft, the Guidelines require the adoption of the Double Materiality Principle. Further clarified from the Exposure Draft, the guidelines have appropriately revised the definition of financial materiality and systematically adjusted the specific disclosure approach and requirements based on the analysis results of material topics.

- Responding to climate change: with reference to the prevailing international climate disclosure framework, the Guidelines set out detailed disclosure requirements on climate topics.

- The Guidelines set different disclosure requirements according to the complexity of the information and the difficulty of disclosure, dividing into three levels: mandatory, encouraged and voluntary, and adopt a combination of qualitative and quantitative disclosure.

Deloitte suggests that companies should take advantage of the transition period to plan and continuously accumulate experience and optimize adjustments in practice. We recommend enterprises refer to the following five steps for action:

- First, establish the governance body responsible for sustainability-related matters, and clarify the roles, responsibilities, ways of performing and principles of the sustainability governance body.

- Integrate sustainability elements into the company's strategy, identify relevant impacts, risks and opportunities, assess their impacts on the enterprise's strategy and business model, and formulate a response strategy.

- Establish internal and external stakeholder engagement mechanisms, identify stakeholder priorities, develop a sustainability disclosure roadmap, and allocate resources to ensure the smooth implementation of the roadmap.

- Establish internal controls and related systems for the collection, management, verification and reporting of sustainability-related data.

- Continuously monitor trends and leading practices in sustainable disclosure, and continuously improve management methods and processes.

Talent and Development

Talent and Development

Deloitte's 2024 Gen Z and Millennial Survey finds these generations stay true to their values as they navigate a rapidly changing world

Deloitte released the 2024 Gen Z and Millennial* Survey, examining the impact of evolving global circumstances on their career paths and societal experiences. This year's survey findings reveal that Gen Zs and millennials are optimistic about the prospects for the year ahead. However, the cost of living is once again their top concern this year, followed by unemployment, climate change, mental health, and crime/personal safety as well as the potential impact brought by Generative AI (Gen AI).

Economic optimism on the rise despite continued financial concerns. Nearly one-third of Gen Zs (32%) and millennials (31%) are optimistic that the economy in their country will improve within the next year, and this optimism extends to their personal finances. Despite this, financial insecurity is also a significant concern, roughly six in ten Gen Zs (56%) and millennials (55%) live paycheck-to-paycheck—up five points for Gen Zs and 3 points for millennials since last year.

Purpose influences workplace satisfaction. Nearly nine in 10 Gen Zs (86%) and millennials (89%) say having a sense of purpose is important to their overall job satisfaction and wellbeing. These generations are increasingly willing to reject assignments or employers who don't align with their values such as having a negative environmental impact. Half of Gen Zs (50%) and over four in 10 millennials (43%) have rejected assignments. Nearly as many (44% of Gen Zs and 40% of millennials) said they have rejected employers before.

Businesses have an opportunity and the necessary influence to drive climate action. In the past month, 62% of Gen Zs and 59% of millennials have felt anxious or worried about climate change. Both generations are trying to drive businesses to act through their career decisions and consumer behaviors. More specifically, two in ten Gen Zs and millennials have already changed jobs or industries due to environmental concerns, with another quarter planning to in the future. As consumers, about two-thirds of Gen Zs (64%) and millennials (63%) are willing to pay more to purchase environmentally sustainable products or services.

Gen Zs and millennials are uncertain about Gen AI, but positive perceptions largely increase with frequent use. Nearly six in 10 Gen Zs (59%) and just over half of millennials (52%) believe the prevalence of Gen AI will make them look for job opportunities that are less vulnerable to automation, such as technical roles or manual labor. It is noteworthy that women express greater uncertainty about Gen AI than men do. In response to these types of concerns, both generations are focused on reskilling and training, about half of Gen Zs (51%) and millennials (45%) say their employers offer sufficient training to help them understand Gen AI-related knowledge.

Work/life balance remains a top concern. Around a third of respondent who regularly feel anxious or stressed say their job and work/life balance contribute a lot to their stress level. Additionally, the return-to-office mandate recently implemented have yielded mixed results, with some reporting benefits like improved engagement, connection and collaboration, while others are experiencing increased stress and decreased productivity.

Despite a dip this year, stress and workplace mental health stigma remain. Stress levels and mental health continue to be a concern, although there are some signs of improvement this year. Up to four in 10 Gen Zs (40%) and millennials (35%) say they feel stressed all or most of the time (down from 46% and 39% in 2023). While employers are making some progress in improving workplace mental health, there is still much room for improvement when it comes to speaking openly about mental health.

*Note: As defined in the study, Gen Z respondents were born between January 1995 and December 2005, and millennial respondents were born between January 1983 and December 1994.

More information: 2024 Gen Z and Millennial Survey

If you have any enquiry, please contact:

Norman Sze

Vice Chair

Deloitte China

Phone: +86 10 8512 5888

Email: normansze@deloitte.com.cn

Maggie Yang

Partner

Deloitte Consulting China

Phone: +86 10 8520 7822

Email: megyang@deloitte.com.cn

Michael Jin

Partner

Deloitte Consulting China

Phone: +86 21 2316 6317

Email: mijin@deloitte.com.cn

Bo Sun

Senior Manager

Deloitte China CXO Program

Phone: +86 10 8512 4866

Email: bsun@deloitte.com.cn

Explore Content

- Play this episode

- Policy support to reignite animal spirits

- Tech Trends 2024: six macro technology forces critical to business

- Stability and progress: Deloitte China releases Chinese Banking Industry 2023 Review and 2024 Outlook

- Deloitte China releases Consumer and Retail Industry Outlook 2024, highlighting new consumption trends

- How can China build more world-class enterprises? Deloitte proposes a new blueprint

- Deloitte Global Chief Procurement Officer Survey: procurement as orchestrators of value

- Sustainability report guidelines for listed companies officially released

- Deloitte's 2024 Gen Z and Millennial Survey finds these generations stay true to their values as they navigate a rapidly changing world