新たな舞台の幕開け – Breaking new ground ブックマークが追加されました

ナレッジ

新たな舞台の幕開け – Breaking new ground

日本のプライベート・エクイティ(PE)市場の概説および今後の展開 – Overview and future outlook of the private equity market in Japan

日本のプライベート・エクイティ環境への関心は、この12か月間で急速に高まりました。資金調達の条件が良く、地政学的に安定しており、企業文化がこの資産クラスを受け入れつつあることが、日本の投資環境を好ましいものにしており、国内外の両方のジェネラル・パートナーは、こうした環境からもれなく恩恵を受けることを期待しています。

「日本のプライベート・エクイティは、2023年に過去最高を記録しました。その背景には、事業承継、企業のカーブアウト、非公開化の全てにおいて、引き続き勢いが増していることがあります」とデロイト アジア パシフィック の関根 俊は述べます。

洞察した内容については、「プライベート・エクイティ・インターナショナル」誌の日本特集に掲載された基調インタビュー「新たな舞台の幕開け」をご覧ください。

Interest in Japan’s private equity landscape has grown rapidly over the past 12 months. Local and international GPs alike are hoping to reap the rewards of Japan’s favourable investment environment, driven by strong fundraising conditions, geopolitical stability and a business culture that is becoming more comfortable with the asset class.

Japanese private equity hit new highs in 2023 as succession deals, corporate carve-outs and take-privates all continued to gain momentum, says Deloitte Asia Pacific’s Satoshi Sekine.

For insights, read the keynote interview, Breaking new ground, featured in Private Equity International’s special report on Japan.

新たな舞台の幕開け

2023年を振り返る ― 日本のプライベート・エクイティ(PE)市場の概説

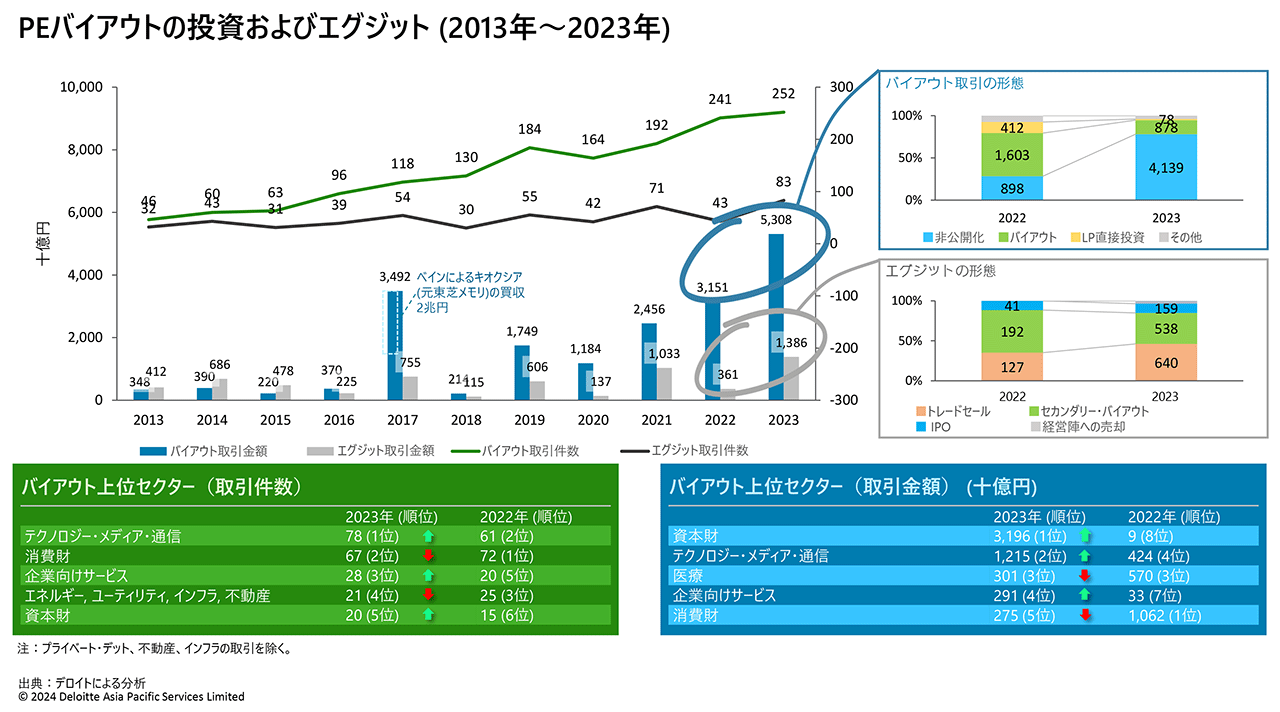

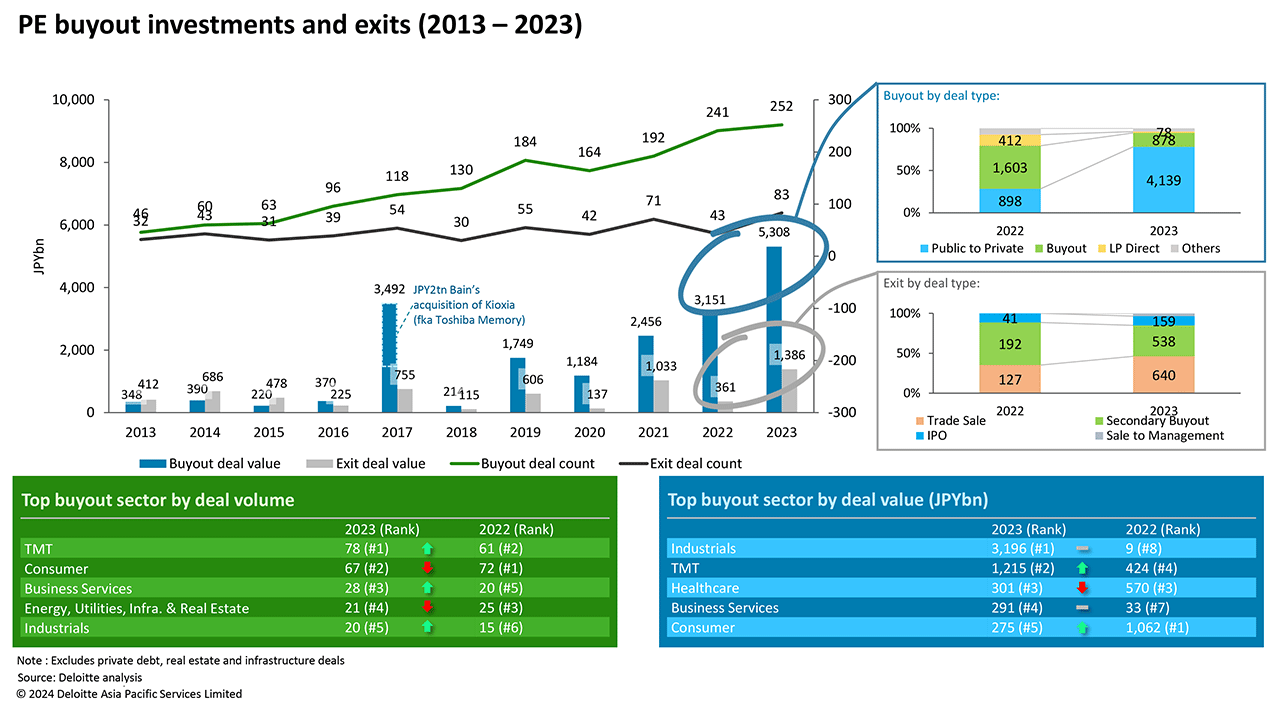

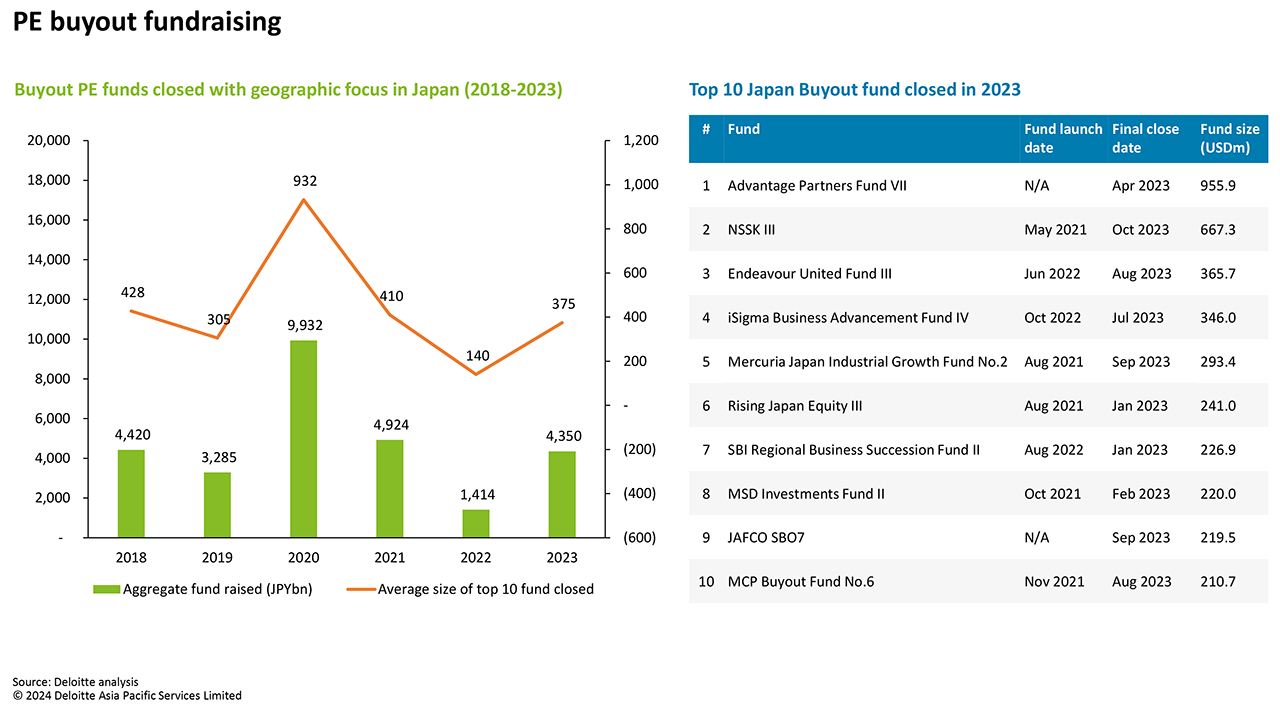

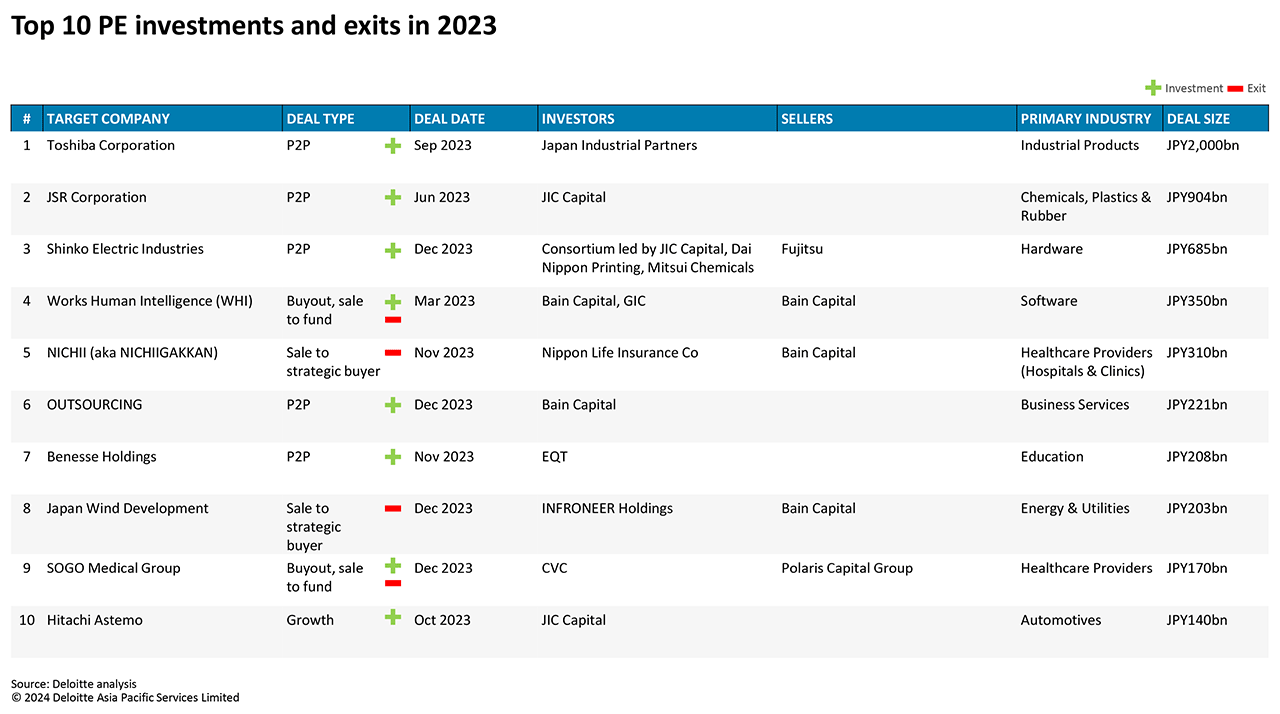

日本に重点を置くリミテッドパートナー(LP)とジェネラル・パートナー(GP)が増加した。その背景には、中国における地政学的な問題と規制改革、他市場における金利上昇による資金調達コスト増、 GPへのリターンが安定していることという要因が重なっている。アジア太平洋に焦点を置くプライベート・エクイティ(PE)のドライパウダー(投資待機資金)は、2023年12月に約6,390億米ドルと、過去最高を記録し、その内3割ほどが日本に配分された1, 2 。この結果、PEバイアウト投資の金額は、過去最高の5兆3,080億円に達し、2021年の2兆4,560億円と2022年の3兆1,510億円を超えた。ディールの規模も、このところ大幅に増大している2。

事業承継

同族企業のオーナーたちは高齢化しており、その多くが適切な後継者探しに困難を覚えている。 2022年において、同族企業の最高経営責任者の平均年齢は60.4歳であり、同族企業の57.2%には組織的な承継計画がない状況である3。事業オーナーにとってPE投資会社が今では身近な存在となり、受け入れられるものになってきたため、事業承継の取引はますます活発化している。事業オーナーは、PE投資会社が提供しうる価値、例えばDX (デジタル トランスフォーメーション)の活用等の業務改善などを認識するようになっている。弊社の分析によると、事業承継の取引は、日本におけるPE取引の6割以上を占め、日本の人口動向を考えると、この数値は上昇する可能性が高い。日本の人口は高齢化すると共に減少しており、2022年の65歳以上の人口は、中国が14%なのに比べ、日本では30%である4。事業承継の取引の金額は、かつては50億円~300億円の範囲だったが、3年ほど前から1,000億円超の事業承継の取引を目にするようになった。

セクターとしては、介護施設や医療など高齢者向けサービスの需要が高いものの6、日本のPE投資企業は、工業製品やテクノロジー企業など、国際的な事業展開を期待できるセクターを選好している。

売り手、特に事業オーナーの関心は、価格だけではなく、PE投資会社が事業を改善・成長させ、従業員やその他のステークホルダー(供給業者、顧客、社会全般)に安心感を与えることができるかどうかに着目している。これを受けてPE投資会社は、ESGが、従業員の動機付けとなり、ガバナンスと透明性をもたらし、環境を保護することにより、価値創造と収益向上の源泉になるという見方を取り始めている。

カーブアウト取引

大型案件については、日本企業は継続的なコーポレート・ガバナンス改革によって事業ポートフォリオの合理化と資本効率性の改善を追求するように促されている。それと同時に、より高度なアクティビスト投資家の活動が増えたため、日本のコングロマリットその他の企業にとり、PE投資会社は頼りがいのある買い手となり、好機が生まれている。利益は出しているが経営管理機能が不足している非中核事業の売却が増加している。

マネジメント・バイアウト(MBO)による非公開化

上場企業が次々と非公開化していることを受け、グローバルなPE投資会社と日本のPE投資会社は、マネジメント・バイアウト取引の活動を増している。これを誘発した要因は数多くあり、コーポレート・ガバナンス・コードおよび企業買収ガイドラインの改訂、日本で活動するアクティビスト・ファンドの増加(2014年に僅か8社であったのに対し、現在は約70社5)、株価純資産倍率(PBR)が1未満の企業に対して東京証券取引所が企業価値向上を要請したこと、低コストの資金調達が依然として可能であることが挙げられる。

来年の展開についての当社の予想

他の市場とは対照的に日本のPE市場は、借入資本が低コストのままで潤沢にあり、経済がこの先も底堅く推移する限り、好調さが続くだろう。このような状況下、事業承継、カーブアウト、マネジメント・バイアウトの取引は増加し続けるであろう。しかし、日本市場には、特にグローバルなプレーヤーといった新規参入者が現れているため、PE投資会社間の競争は依然として激しい。この結果、10億米ドル超の大型ディールをめぐる競争は激化し6、それが買収価格を引き上げることになる。こうした理由から、優良案件を発掘し、オペレーションを改善させる能力を高めることは、プライベート・エクイティにとり、2024年における成功の決め手となるだろう。

注 1: Preqin

注 2: デロイトによる分析

注 3: 帝国データバンク

注 4: 世界銀行データ

注 5: アイ・アール ジャパン

注 6: プライベート・エクイティ・インターナショナル、2023年4月

Breaking new ground

Year In Review – Japan 2023 PE Market Summary

We have seen more LPs and GPs focusing on Japan in response to a combination of factors including geopolitical issues and regulatory reform in China, more-expensive financing due to higher interest rates in other markets, and steady returns for GPs. Asia Pacific-focused PE dry powder reached a record high in December 2023 at around USD639bn, of which approximately 30% is allocated to Japan.1,2 As a result, PE buyout investment value reached a record high of JPY5,308bn in 2023, up from JPY2,456bn in 2021 and JPY3,151bn in 2022, and deal size has recently increased significantly.2

Business succession

The owners of family businesses are ageing and many of them have been facing difficulties in finding suitable successors. The average age of CEOs of family businesses is 60.4 and 57.2% of family businesses do not have a formal succession plan as of 2022.3 Business succession deals continue to gain momentum as business owners are now becoming more familiar with, and accepting of, PE firms. Business owners have come to recognise the value that PE firms can deliver, for example through operational improvements including the use of digital transformation. Based on our analysis, business succession deals represent more than 60% of PE deals in Japan and this figure is likely to grow given Japan’s demographic trends: the population is both ageing and shrinking, with 30% of the population aged 65 or above in 2022, compared to 14% in China.4 The value of business succession deals used to be in the JPY5bn to JPY30bn range but from about three years ago, we have been seeing business succession deals of over JPY100bn.

In terms of sectors, services for the elderly, such as nursing homes and healthcare, are in high demand 6, but PE firms in Japan favour sectors that have international expansion potential, such as industrial products and technology companies.

Sellers, particularly business owners, are interested in more than price alone: they are looking at whether PE firms can improve and grow the business, and provide comfort to employees and stakeholders such as suppliers, customers and community. In this response, PEs have started to view ESG as a source of value creation and higher earnings by incentivizing employees and providing governance and transparency, and protecting environment.

Carve-out deals

At the larger end, continuous corporate governance reforms encouraged Japanese companies to pursue business portfolio rationalisation and improve capital efficiency. At the same time, more sophisticated shareholder-activist campaigns have created opportunities for PE firms as go-to buyers for Japanese companies including conglomerates. There has been in an increase in the sale of profitable but under-managed non-core businesses.

Public to private through management buyouts (MBOs) Global and domestic PE firms have become more active in management buyout transactions in response to a wave of delistings from the public market. These have been triggered by a number of factors, including: revised corporate governance code and takeover guidelines; an increase in activist funds operating in Japan, currently at around 70 compared to just 8 in 2014 5; Tokyo Stock Exchange’s request to companies with a price-to-book ratio (PBR) below one to improve corporate values; and low-cost financing still being available.

What we expect to happen next year

In contrast to other markets, Japan’s PE market will remain strong as long as the cost of debt capital continues to be low with good availability, and the economy continues to be resilient. In these conditions, business succession, carve-out, and MBO deals will continue to increase. However, competition among PE firms remains strong as there are new entrants to Japanese market, particularly global players. As a result, competition for large-cap deals over USD1bn is intensifying 6, resulting in high valuations. For this reason, enhancing the capabilities for sourcing good deals and delivering operational improvements will be key to PEs’ success in 2024.

Note 1: Preqin

Note 2: Deloitte analysis

Note 3: Teikoku Data

Note 4: World Bank data

Note 5: IR Japan

Note 6: Private Equity International, April 2023

お問い合わせはこちら

プロフェッショナル