Artykuł

EBA publishes new standards and guidelines on IRRBB and CSRBB management

New regulatory package

Risk Advisory 2023

Background

Rising interest rates, high inflation, and the unstable situation on financial markets have made the issues related to Interest Rate Risk in the Banking Book (IRRBB) and Credit Spread Risk in the Banking Book (CSRBB) the focus of attention for the regulators.

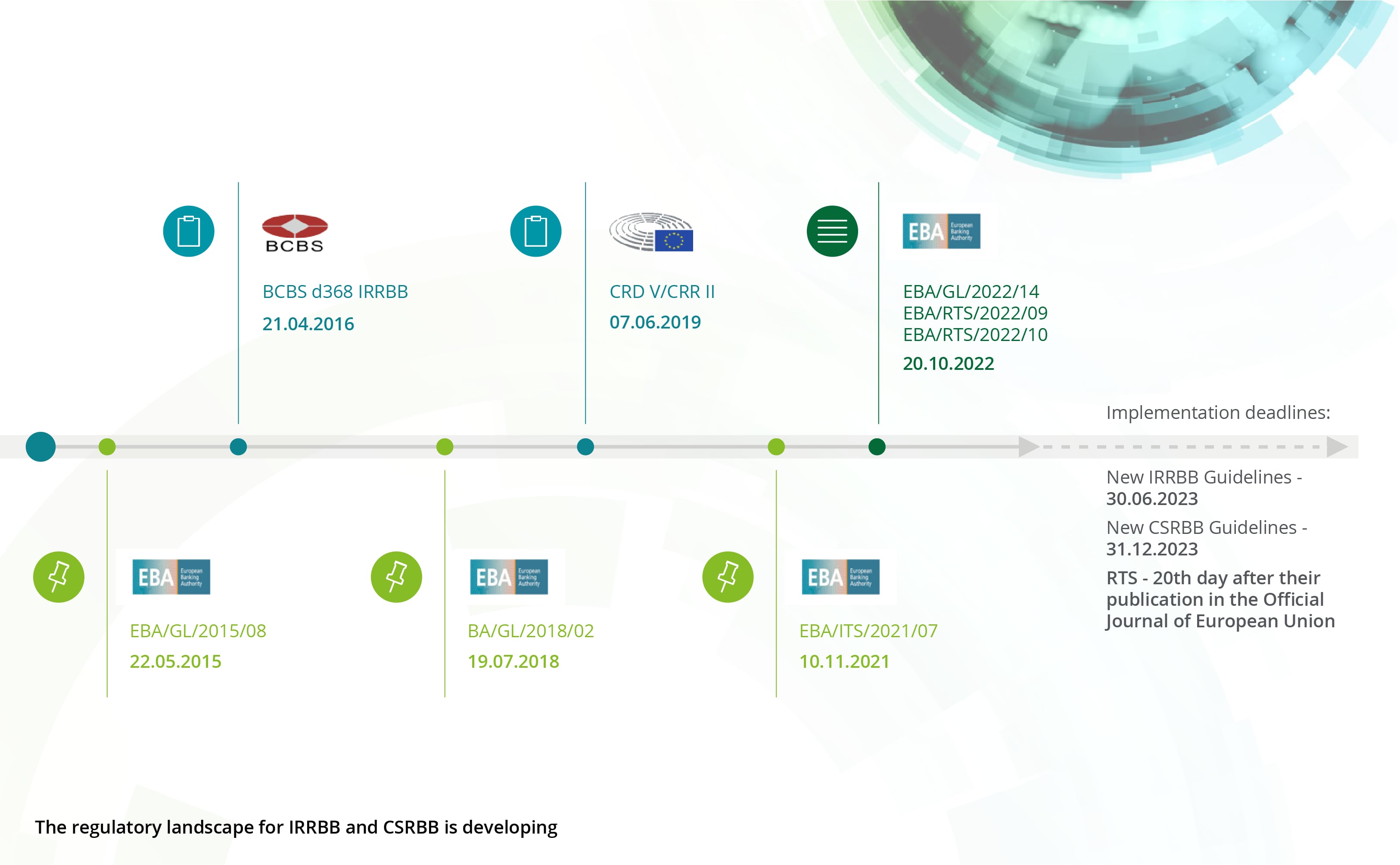

Accordingly, the European Banking Authority (EBA) updated and complemented the existing Guidelines on IRRBB and CSRBB by publishing a set of new regulatory requirements on 20 October 2022.

The regulatory package presented by EBA includes:

- New Guidelines specifying the methods of identifying, assessing, and limiting interest rate risk and credit spread risk arising from the banking book activities.

- Regulatory Technical Standards defining a standardised approach and a simplified standardised approach to measuring risk arising from potential interest rates changes that affect both the economic value of equity and the net interest income of an institution’s non-trading book activities.

- Regulatory Technical Standards specifying shock scenarios and parametric assumptions for the supervisory outliers’ tests (SOT) on both: the economic value of equity as well as net interest income.

The deadline for implementation of the updated Guidelines on IRRBB is 30 June 2023, while the new CSRRB Guidelines will apply later, on 31 December 2023.

Financial directors, risk managers, ALM units and validation teams in banks should thoroughly familiarize themselves with the introduced regulations as they entail significant changes in the existing EBA Guidelines. The following article provides an overview of the updated Guidelines and Regulatory Technical Standards and summarizes the key challenges faced by banks in terms of implementation of the new regulations.

New Guidelines on CSRBB management

The updated EBA regulations distinguish credit spread risk in the banking book as a new risk category that should be considered by financial institutions in the risk management processes and internal capital estimation processes. In addition, the regulations specify the requirements for measurement, monitoring and internal control of the CSRBB.

Definition of credit spread risk

The EBA defines CSRBB as the risk of changing the credit spread of an instrument assuming an unchanged level of creditworthiness or rating of the counterparty.

The CSRBB consists of:

- The market credit spread, representing the premium required by market participants for a given credit quality

- Market liquidity spread, representing a premium for market participants investing in low-liquidity financial instruments.

The idiosyncratic components of the credit spread (representing the situation of the individual borrower or the specificity of a particular instrument) are in principle excluded from the measurement of the CSRBB. EBA states that institutions. may include idiosyncratic credit spread components for the monitoring of CSRBB, if it is ensured that the measures will yield more conservative results.

Guidelines for the measurement of CSRBB

According to the new Guidelines, the individual approach to measuring CSRBB developed by a financial institution should be proportionate to the nature, scale, and complexity of the risks inherent in the business model and the institution's activities.

The CSRBB measurement should include all instruments in the banking book (assets, liabilities, derivatives, and other off-balance sheet items), excluding non-performing exposures. Any potential exclusion of an instrument from the calculations should be thoroughly justified and documented. Additionally, EBA points out that the exclusion of assets measured at fair value should under no circumstances take place.

Measures of economic value, net interest income and net interest income extended by the change in the market value of the instrument should all be considered in the calculation of credit spread risk.

Guidelines on monitoring and validation of CSRBB models

The new Guidelines for credit spread risk monitoring and validation of CSRBB measurement models are largely analogous to EBA IRRBB regulations in this regard.

Institutions' internal reporting on credit spread risk should take place at least on a quarterly basis. On the other hand, the CSRBB models should be reviewed at least once a year, and even more frequently in the event of rapid changes on the financial markets.

The validation of CRRBB measurement methods should become a formal process in institutions, approved by the management body and reviewed regularly.

Updated Guidelines on IRRBB management

The new regulatory requirements introduce several modifications to the existing IRRBB Guidelines.

Assessment of the IRRBB internal measurement system

The updated Guidelines specify when the internal IRRBB measurement method implemented in a financial institution is not satisfactory.

According to the new Regulations, the IRRBB measurement criteria are not met when:

- Using internal methods, the bank does not include in the calculations significant components of interest rate risk (gap risk, base risk, option risk) or any of these risk components is omitted in the risk measurement for any of the bank positions;

- The risk measurement methods implemented in the bank are not properly and frequently back tested, parameterized, and the measurement methods used are disproportionate to the level of risk associated with the business model and the institution's activities.

If the IRRBB measurement method adopted by the bank is considered not satisfactory, the bank is obliged to implement a standardised approach (or a simplified standardised approach), presented in the Regulatory Technical Standard EBA/RTS/2022/09 and discussed in the next section of the article.

Non-maturing deposits modelling

The new Guidelines also introduce an upper limit on the revaluation date of deposits without a contractual maturity date (NMD) used in the IRRBB measurement (the 2018 Guidelines limited the maturity of NMDs only for the supervisory outlier tests). In accordance with the updated Regulations, the average, denomination-weighted revaluation date for

- Retail and wholesale non-maturing deposits of non-financial clients,

- Operational non-maturing deposits of financial clients.

may not exceed five years. This limit applies to the total volume (core and non-core part) of the aggregated portfolio of NMDs of a given category, in a specific currency. The change may affect the internal results of IRRBB measurements and management, and in particular have an impact on hedging positions. EBA announces that assumptions accepted by financial institutions regarding NMDs will be a subject of detailed analysis of the regulators.

Non-operational NMDs of financial clients should not be modelled and should have maturity in overnight.

Extended NII measure

The extended NII measure should be considered by financial institutions both in the risk management processes (such as risk measurement, monitoring or control) as well as in defining their risk appetite.

The extended NII measure, in addition to the net interest income also includes the impact of changes in interest rates on the fair valuation of instruments, which, depending on the adopted accounting standards, is recognized either in the income statement or directly in equity (through other comprehensive income).

The change in the extended net interest income should be calculated as the sum of:

- The difference between expected net interest income in the stress scenario and expected net interest income in the baseline scenario.

- The difference between the expected market value of the instrument in the shock scenario and the expected market value of the instrument in the baseline scenario at the end of the time horizon under analysis. Cash flows within the NII horizon are excluded from the calculation of changes in market value to avoid double recognition.

Measurement at fair value should consider behavioural options embedded in the instruments.

Institutions should also pay special attention to the fact that changes in the interest rate environment may affect the valuation of hedging instruments and hedged items in a different way, which may consequently affect the profit and loss account.

EBA's standardised approach to IRRBB

The requirements for a standardised approach to the calculation of economic value and net interest income developed by EBA are presented in the regulatory technical standard EBA/RTS/2022/09.

The main assumptions of the requirements for the calculation of EVE and NII measures are based on:

- the distribution of cash flows into 19 predefined time buckets according to their repricing date, which is a key feature of the Basel approach;

- the clarification of the Basel standards in the regard of the treatment of behavioural options, i.e. the treatment of products in which the timing and amount of cash flow depends on customer behaviour;

- the calculation of the add-on for automatic optionality

The approaches to the calculation of both measures differs in several aspects. The calculation of the EVE measure assumes an expiring balance sheet and discounting of cash flows until the reporting date. The NII measure, on the other hand, is calculated in a specific time horizon (e.g. annual), assuming an unchanged balance sheet, in which maturing cash flows are replaced by new contract production. Moreover, when calculating net interest income, cash flows are not discounted.

In addition, the Standards define three components of the NII measure calculation that are not included in the EVE calculation.

These are:

- the aggregation of interest payments, which are already fixed, and their amount will not change due to interest rate changes; material amounts of interest accrued at t=0 need to be subtracted from this amount;

- the projection of risk-free yield for each repricing cash flow between the repricing date and the end of the projection horizon, in accordance with the assumption of a constant balance sheet.

- the projection of the commercial margin for each notional repricing cash flow between the moment of the reset of the margin (typically at the instrument’s maturity) up to the end of the projection horizon, in accordance with the assumption of a constant balance sheet

The new guidelines recommend calculating the NII measure also in the longer time horizons than one year – e.g. two/three years, considering the calculation of NII in a one-year horizon as the necessary minimum.

The Regulatory Technical Standards also introduced significant innovations in the field of behavioural parameters adopted in the calculation, such as the use of Basel scalars (1.2 and 0.8 respectively) to modify the core part of accounts without a contractual maturity date in the event of an increase or decrease of the interest rates.

In addition, the Standard adopts limits set by the Basel Committee on Banking Supervision on the core part of current accounts, ranging from 50% to 90% depending on the type of the account as well as the cap (4 to 5 year) on the weighted average maturity of core deposits.

Simplified standardised approach

The EBA allows for the simplification of a standardised approach for the smallest institutions with a moderate risk profile.

In the simplified standardised approach, the following modifications have been made for both EVE and NII measurement:

- The core part of deposits with no maturity date is predetermined and is not subject to behavioural modelling on the bank's side.

- Institutions do not need to use their own estimates of the time remaining to maturity of the core portion of deposits without a contractual maturity date - the simplified approach provides a method for obtaining linear maturity date allocations between four and five years; The time assumed in the calculations until the maturity of the core part depends on the type of account and on the stress scenario (in the case of an increase/decrease in interest rates, it is scaled by 0.7 or 1.3, respectively).

- To measure NII and EVE, institutions do not need to perform a comprehensive analysis covering the effects of increased volatility.

In addition, only in the case of a simplified standardised approach to the calculation of the NII, the EBA has defined further simplifications:

- Institutions do not need to project cash flows according to their original maturity date and may adopt an average maturity date for contracts in each product category.

- The empirical determination of commercial margins need not be carried out based on geographical data, but only with a breakdown to product type.

- It is not necessary to aggregate interest payments that are not sensitive to changes in the interest rate (i.e. cash flows that are already fixed and will not change due to changes in interest rates), instead of aggregating interest payments for all instruments, institutions may use estimations using the average interest rate and the outstanding value of capital.

Regulatory Technical Standards on the supervisory outlier tests

EBA has developed Regulatory Technical Standards defining supervisory shock scenarios as well as modelling and parametric assumptions of supervisory outlier tests on EVE and NII.

Purpose of the supervisory outlier tests

The new IRRBB regulations in conjunction with Article 98 (5) of CRD5 introduce two important changes regarding the supervisory outlier tests (SOT): the replacement of SOT 20% on EVE and the introduction of SOT on NII.

According to the updated Regulations, banks should examine whether in any of the analysed shock scenarios:

- The value of EVE will not fall by more than 15% of Tier 1 equity, or

- The institution's annual net interest income will not fall by more than 2.5% of Tier 1 equity.

If any of these limits is exceeded, the relevant competent authority may exercise its supervisory powers.

SOT on EVE measure

The approach to conducting the supervisory outlier tests on EVE measure is largely based on the methodology described in the IRRBB standards published by the Basel Committee on Banking Supervision (BCBS) in 2016. The tests are performed in six different shock scenarios, assuming an expiring balance sheet. The decision whether to include or exclude commercial margins is left to the institutions.

SOT on NII measure

To perform the tests on net interest income, an assumption is made that the balance sheet will remain unchanged over an annual time horizon. Net interest income in the context of the supervisory outlier tests is understood by the EBA as interest income less interest expenses – a change in the market value of instruments should not be included in the calculation. NII should be measured in one year horizon.

The commercial margins of instruments included in the new production for the purposes of the fixed balance sheet should be based on the commercial margins of instruments with similar characteristics that were purchased or sold in the period immediately preceding the calculation.

The supervisory outliers’ tests are conducted for a measure of net interest income in two adverse scenarios:

- A parallel upward shift of the yield curve with the same positive interest rate shocks for all maturities; and

- A parallel downward shift in the yield curve with the same negative interest rate shocks for all maturities.

Modification of the structure of the interest rate curve

The new regulations also change the lower ceiling (the so-called floor rate) of interest rates used to calculate EVE and NII measures. The new value of the floor rate for immediate maturity – ON tenor, is 150 basis points. The lower bound should increase by 3 basis points per year, reaching 0% for maturities 50 years from the date of analysis.

Inclusion of contracts in other currencies

According to the new EBA Guidelines, when calculating the aggregate change in EVE or NII for each interest rate shock scenario, institutions should add together any negative and positive changes in the outcome occurring in each significant currency. Currencies other than the reporting currency shall be converted into the reporting currency at the ECB exchange rate.

Positive changes in both currency measures should be weighted by a factor of 50% or a factor of 80% - in the case of currencies belonging to the exchange rate mechanism ERM II with a formally established fluctuation band narrower than the standard band of +/- 15%.

Weighted gains should be recognised up to the higher of the following:

- The absolute value of negative movements in the euro or ERM II currencies, and

- The result of applying a 50 % factor to positive movements in ERM II or EUR currencies.

Draft Implementing Technical Standards for IRRBB reporting

On 31 January 2023, the European Banking Authority published a consultation paper on Implementing Technical Standards (ITS) on supervisory reporting with respect to IRRBB. EBA plans to include comprehensive IRRBB reporting in the Common Reporting Framework (COREP) Together with the consultation document, the Authority also provided a reporting template and instructions for completing it.

The announced unification of the IRRBB reporting approach is intended to improve the quality of data received by supervisory units, thus enabling them to effectively monitor:

- The level of risk in individual financial institutions

- Implementation of the EBA regulation package of October 2022.

The deadline for comments on the consultation document is 2 May 2023. EBA plans to submit the ITS to the Commission of the European Union in mid-2023. The first expected reporting date under the IRRBB reporting requirement is June 30, 2024.

Contact:

Rekomendowane strony

Tool for managing interest rate risk in the banking book

Deloitte IRRBB Tool