Noncontrolling interests has been saved

Perspectives

Noncontrolling interests

On the Radar: Interpreting the accounting guidance

Consolidation of a subsidiary may require reporting on equity-classified instruments that the parent doesn’t own. Between complex capital structures and varying levels of guidance, the accounting principles for these noncontrolling ownership interests can be difficult to apply.

On the Radar series

High-level summaries of emerging issues and trends related to the accounting and financial reporting topics addressed in our Roadmap series, bringing the latest developments into focus.

A challenging aspect of US GAAP

Once a reporting entity concludes that it is appropriate to consolidate another legal entity, the reporting entity must evaluate the accounting for equity instruments that are not owned by the parent. Only equity-classified instruments that are not owned by the parent are noncontrolling interests.

The objective of accounting for noncontrolling interests is to present users of the consolidated financial statements with a clear depiction of the portion of a less than wholly owned subsidiary’s net assets, net income, and comprehensive income that is attributable to holders of equity-classified ownership interests other than the parent. In practice, the combination of complex capital structures, multiple sources of authoritative guidance on accounting for noncontrolling interests, and multiple policy elections available to reporting entities can make this objective difficult to achieve.

ASC 810-10-20 defines a noncontrolling interest as the “portion of equity (net assets) in a subsidiary not attributable, directly or indirectly, to a parent” and further states that a “noncontrolling interest is sometimes called a minority interest.” This definition applies to all entities that prepare consolidated financial statements.

Although the accounting principles related to noncontrolling interests have been in place for many years, they can be difficult to apply. The relatively brief guidance on nonredeemable noncontrolling interests (ASC 810-10) has resulted in diversity in practice, while the guidance on redeemable noncontrolling interests (ASC 480-10-S99-1 and ASC 480-10-S99-3A) is highly prescriptive and contains multiple policy elections. For these reasons, accounting for noncontrolling interests is a particularly challenging aspect of US GAAP.

On the Radar: Noncontrolling interests

Identifying noncontrolling interests

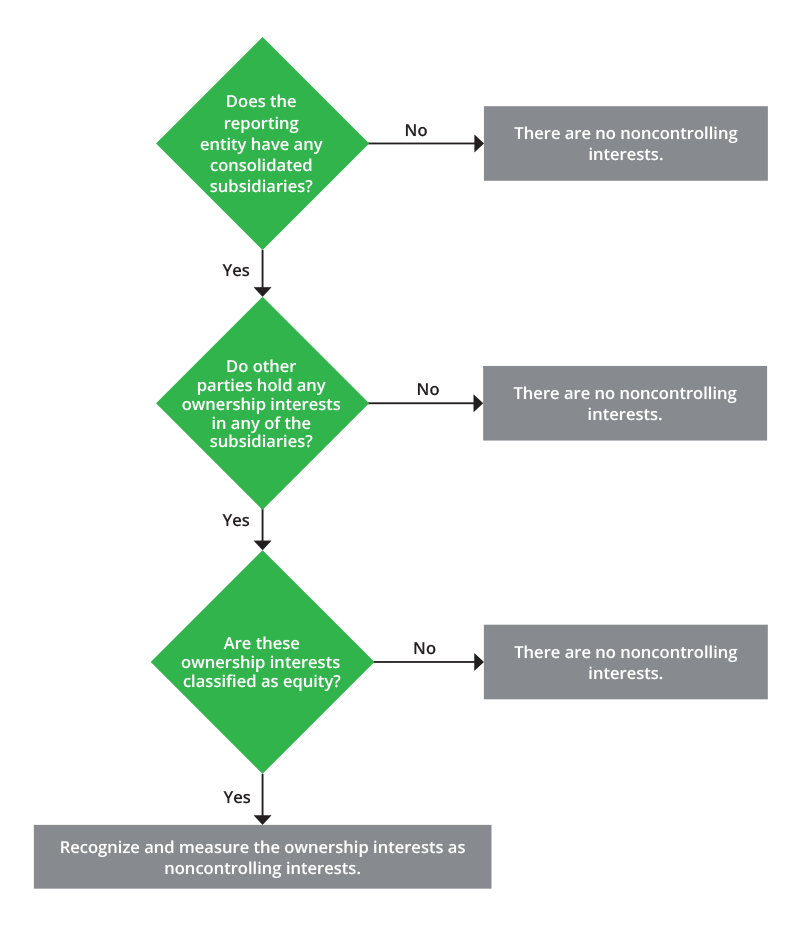

The decision tree below illustrates how to determine whether a reporting entity has any noncontrolling interests.

Since a noncontrolling interest is defined as a specific “portion of equity” (emphasis added), the first step in the identification of a noncontrolling interest is to establish whether such ownership interest in the subsidiary is appropriately classified in the equity section of the subsidiary’s balance sheet and the parent’s consolidated balance sheet.

Key areas of focus

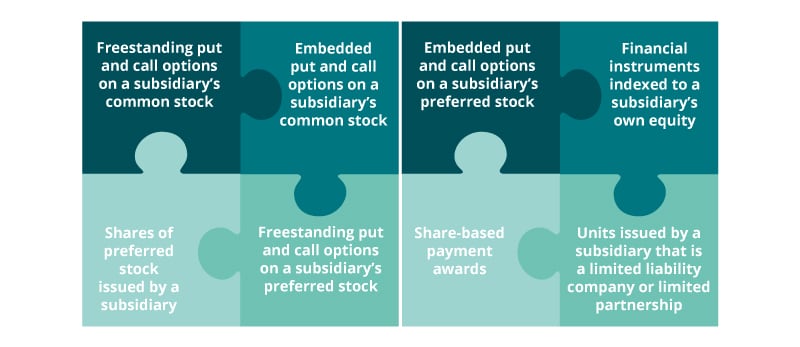

For simple capital structures involving only equity-classified common stock, the noncontrolling interest is the portion of the subsidiary’s equity not owned by the parent. For more complex capital structures, a reporting entity will need to use considerable judgment when determining whether an ownership interest represents a noncontrolling interest. While a legal-form liability is never considered a noncontrolling interest, not all equity instruments may be considered noncontrolling interests. Interests that require judgment include, but are not limited to, the following:

It is important to note that the scope of the noncontrolling interest literature begins with the identification of an instrument as an equity interest and the instrument’s classification as such on the balance sheet.

The measurement of noncontrolling interests on the reporting entity’s balance sheet is affected, in part, by the manner in which elements of a subsidiary’s income and other comprehensive income or loss are attributed to the parent’s controlling interest and the noncontrolling interests held by parties other than the parent.

While ASC 810-10 requires a reporting entity to allocate a subsidiary’s income or loss and comprehensive income or loss between the controlling and noncontrolling interests, it does not prescribe a specific means for doing so. Although attribution of income or loss and comprehensive income or loss is commonly performed on the basis of the relative ownership interests of the parent and noncontrolling interests, there are many instances in which it would be inappropriate to attribute income or loss solely on the basis of relative ownership percentages.

When assessing an appropriate attribution method, companies should consider (1) the attribution when contracts specify allocations of profits and losses, costs and expenses, or distributions that differ from investors’ relative ownership percentages, (2) the attribution of losses in excess of the investee’s carrying value, (3) the attribution of eliminated income or loss (both for entities consolidated under the variable interest entity model and for those that are not), (4) the attribution of income in the presence of reciprocal interests, and (5) the attribution of other comprehensive income or loss.

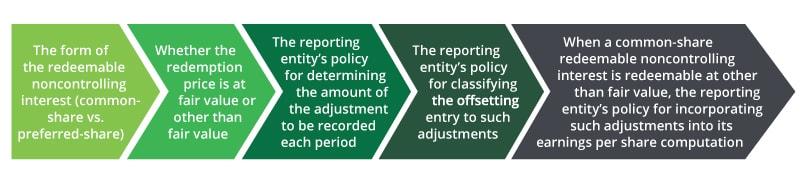

Common and preferred shares of a consolidated subsidiary are sometimes subject to redemption rights held by the noncontrolling shareholder. Accounting for a redeemable noncontrolling interest is one of the more complex aspects of US GAAP to apply because the reporting entity’s accounting may be affected by a multitude of factors that are specific to the redeemable instrument itself and to policy elections made by the reporting entity. Such factors include the following:

Nearly all of the guidance on accounting for redeemable noncontrolling interests is codified in ASC 480-10-S99-3A and originated with the SEC staff’s interpretations of ASR 268 in EITF Topic D-98. Accordingly, this guidance must be applied by all SEC registrants. While reporting entities other than SEC registrants are not subject to the guidance in ASC 480-10-S99-3A, they may elect to apply it.

When applied, ASC 480-10-S99-3A is essentially an “overlay” that is applied after the application of ASC 810-10. That is, a reporting entity must apply the provisions of ASC 810-10, including the guidance on attributing subsidiary income to controlling and noncontrolling interests, before applying the provisions of ASC 480-10-S99-3A, which primarily focus on subsequent measurement and balance sheet presentation issues that arise from the existence of a redemption feature. A redeemable noncontrolling interest may also affect a reporting entity’s earnings per share computation.

The decision tree below illustrates how to evaluate the redemption features included in a contract with a noncontrolling interest holder, or embedded in the noncontrolling interest, when the noncontrolling interest itself has already been determined to be appropriately classified as equity.

Please refer to the OTR 2024 PDF for the decision tree image

An entity’s ownership structure is often fluid. For instance:

- A parent may directly purchase additional ownership interests in its subsidiary from a third party, or it may sell some or all of its current ownership interests in the subsidiary to a third party.

- Alternatively, a subsidiary may issue (purchase) additional ownership interests to (from) third parties, thereby diluting (concentrating) the parent's ownership interest.

Irrespective of the events that lead to changes in ownership interests in the subsidiary, if control has not changed, a parent accounts for such changes in ownership as equity transactions. Generally, the parent should neither recognize a gain or loss on sales or issuances of subsidiary shares nor step up to fair value the portion of the subsidiary's net assets that corresponds to the additional interests acquired. Rather, any difference between consideration paid or received and the change in noncontrolling interest is typically recorded in equity. As part of equity transaction accounting, the reporting entity must also reallocate the subsidiary's accumulated other comprehensive income (AOCI) between the parent and the noncontrolling interest.

To properly reflect these principles when accounting for changes in ownership interest (within the scope of ASC 810-10) without an accompanying change in control, a reporting entity should perform the following five steps:

ASC 810-10 requires:

- Separate presentation of consolidated net income and consolidated comprehensive income on the face of the consolidated financial statements; additional detail must also be provided about the portions of each of these totals that are attributable to the parent and the noncontrolling interests, respectively

- Reconciliations of changes in stockholders’ equity that detail changes attributable to the parent and the noncontrolling interests, respectively

- Disclosure of reallocations of AOCI between the parent and the noncontrolling interests

Each of these presentation and disclosure requirements ultimately arises from the desire to clearly articulate for users of financial statements how changes in a reporting entity’s net assets affect the parent and noncontrolling interest holders.

While ASC 810-10 provides extensive presentation and disclosure guidance aimed at clearly depicting a noncontrolling interest holder’s claim on the net assets, net income, and comprehensive income of a consolidated subsidiary, no such presentation and disclosure requirements exist for the consolidated statement of cash flows. Redeemable noncontrolling interests remain subject to the disclosure and reconciliation requirements of ASC 810-10-50-1A(c) and SEC Regulation S-X, Rule 3-04, even if such interests are classified in the temporary equity section of the reporting entity’s balance sheet.

Continue your noncontrolling interests learning

Deloitte’s Roadmap Noncontrolling interests comprehensively discusses the accounting guidance on noncontrolling interests, primarily that in ASC 810-10 and ASC 480-10-S99-3A. For extensive analysis of whether a reporting entity should consolidate another legal entity, see Deloitte’s Roadmap Consolidation—Identifying a controlling financial interest. Entities should also consider Deloitte’s Roadmap Distinguishing liabilities from equity, which provides extensive interpretive guidance on the appropriate classification of equity instruments, including noncontrolling interests, within or outside of the equity section of a reporting entity’s balance sheet.

Subscribe to the Deloitte Roadmap Series

The Roadmap series provides comprehensive, easy-to-understand guides on applying FASB and SEC accounting and financial reporting requirements.

Explore the Roadmap library in the Deloitte Accounting Research Tool (DART), and subscribe to receive new publications via email.

Let's talk!

Learn more about this topic

|

Andrew Winters |

|

Andrew Pidgeon |

Get in touch for service offerings

|

Will Braeutigam |

|

Recommendations

A guide to consolidation accounting

On the Radar: Identifying a controlling financial interest

Distinguishing liabilities from equity

On the Radar: Financial reporting impacts of ASC 480