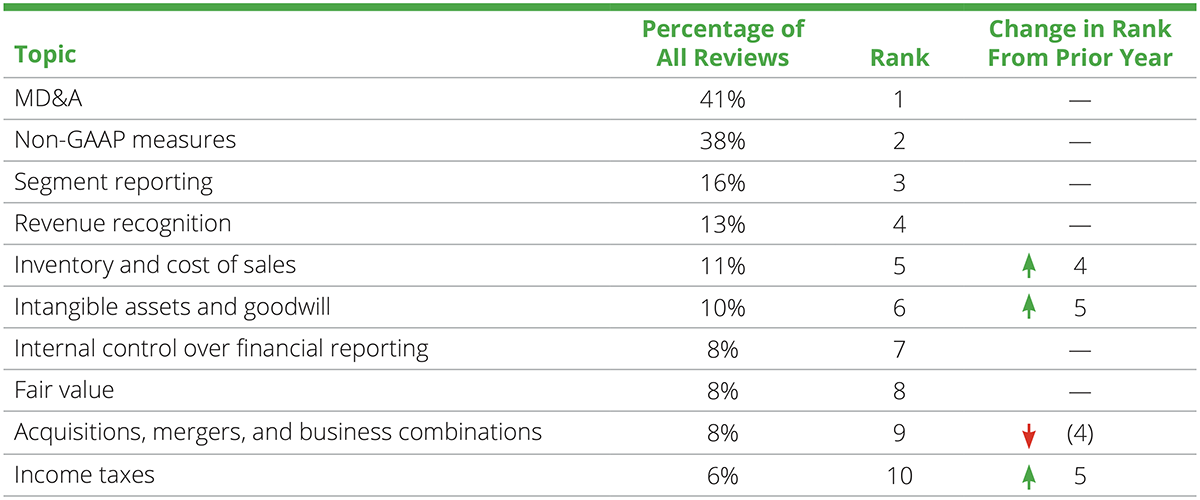

Top 10 topics in reviews

The table below summarizes comment letter trends by topic in the 12-month period ended July 31, 2024 (“review year 2024” or the “current year”).

The topics that constitute the current year’s top 10 list are largely consistent with the prior year’s list. However, the topic of income taxes and that of intangible assets and goodwill have joined the top 10 list, while the topic of signatures, exhibits, and agreements and that of debt have dropped out of the top 10.2 Comments on MD&A and non-GAAP measure disclosures continue to increase in number, and these topics are still the two most significant sources of SEC comments by a wide margin since the staff remains laser-focused on them. Given the SEC staff’s focus on ensuring that disclosures provide decision-useful information from management’s perspective, we expect the volume of comments on MD&A to remain high. We also observed an increased number of comments related to intangible assets and goodwill, which rose from 11th place in 2023 to 6th place in 2024 because of an increase in comments asking for expanded “early-warning” disclosures about potential impairments. In addition, income taxes moved up five spots to 10th place because of an increase in comments on tax-related disclosures required by ASC 740.

Further, although not identified as a separate top 10 topic, the impacts of higher interest rates, inflation, and supply-chain issues remained a source of SEC comments over the past year. Such comments have focused on disclosures related to the effects of these macroeconomic and geopolitical challenges on a registrant’s (1) risk factors, (2) MD&A, (3) market risk disclosures, (4) early-warning disclosures about impairments, and (5) adjustments to non-GAAP measures. At a recent conference, the SEC staff has advised registrants that as inflation and interest rates moderate, its equally important to provide transparent, company-specific disclosures about such trends so that investors can understand how and when companies are affected by these changing macroeconomic factors.

A number of the aforementioned trends are likely to continue in years to come since comment letter topics have been largely consistent year over year. While it is difficult to predict what new comment letter trends are on the horizon, we look to the Commission’s priorities to help us predict topics of focus in the coming year. The SEC staff has spoken extensively about disclosures related to AI, and we expect the staff to comment on such disclosures in future reviews. Given that the staff often focuses on compliance with new reporting requirements, we expect to see comments on new disclosures required under US GAAP about supplier finance programs and segment reporting, as well as comments on new cybersecurity disclosures required under SEC regulations. In addition, we expect the SEC staff to continue monitoring the impacts of interest rates, inflation, geopolitical conflicts, and concerns about the commercial real estate market, and perhaps focus future comments on accounting and reporting related to these matters. These events, coupled with the staff’s focus on ensuring that MD&A provides useful information to investors, mean that comments on MD&A are likely to remain elevated.