Get ready: How boards can prepare for activism’s next wave has been saved

Perspectives

Get ready: How boards can prepare for activism’s next wave

On the board’s agenda, February 2021

By Chris Ruggeri, Joel Schlachtenhaufen, Maureen Bujno, Annie Adams, and Bob Lamm

Explore content

- Introduction: A year of consequence

- The 2020 slowdown set the stage

- Activism in 2021: The landscape has changed

- The active board: Preparation and response

- Conclusion

Introduction

As we begin to see the light at the end of the tunnel of a pandemic that upended all of our lives and disrupted almost every business, activist investors are getting in gear, and the pieces are expected to be in place for continued growth in merger and acquisition activity through 2021. Political unrest, accelerating social change, and renewed emphasis on corporate purpose beyond shareholder primacy will continue to shape the future and inject uncertainty. Our world is literally changing before our eyes, and we have to ask ourselves, how will this affect shareholder activism in 2021 and beyond, and what will the impact be on M&A activity? And how have the events of 2020 changed what board directors need to do to be prepared for M&A generally and to deal with activists that might emerge?

Get ready: How boards can prepare for activism’s next wave

The 2020 slowdown set the stage

Activist investor activity slumped in 2020 as the pandemic rattled markets, managements, and investors. Globally, 652 companies were subject to activist demands through the first three quarters of 2020—the slowest pace since 2015.1 The drop was also pronounced in the United States, which saw the fewest activist campaigns since 2014. 2021 could show a reversal of this trend with a growth in shareholder activist campaigns.

The issues that sidelined activist investors for a time, such as overtaxed management and volatile markets, have eased. And new campaigns are likely to come quickly, with a growing focus on M&A.

With 2021 likely to be a busy year for activist campaigns, boards need to be ready. The evergreen advice that they must think like activists will be more important than ever. But there’s an added layer. Boards also need to be informed about and proactively engaged with the dramatic changes that have occurred in society, affecting the business landscape and their company. They need to think ahead—to have and be able to articulate the vision and strategy that will allow their companies to thrive through whatever comes next.

Activism in 2021: The landscape has changed

Board members need to understand what factors will likely motivate activist investors in 2021 and be ready to grapple with key issues that activist campaigns could put on the table.

As a starting point, the underlying rationale for activism—that it’s possible for an investor to identify opportunities that a company could take to boost value—hasn’t changed. However, considerations for the board have. To be sure, in the early months of the pandemic, the attention of corporate leaders was focused on the safety and health of customers and employees. Activists took a pause given health, political, and capital markets uncertainty. As the environment stabilizes, questions about the right path forward for any company to thrive are again front and center. Shareholders are seeking a role in shaping that future, and boards need to be prepared to balance a broader and more diverse range of sometimes competing stakeholder interests in decision making.

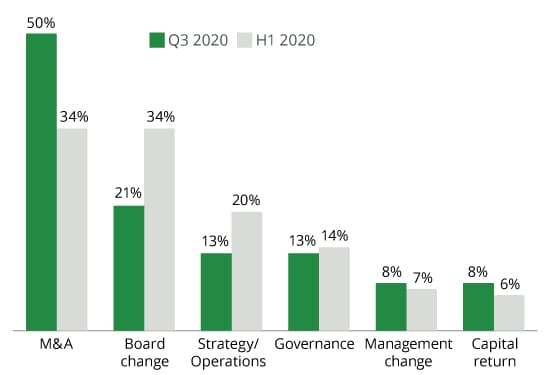

Activist investors are also getting a tailwind from the recent M&A rebound. Activists have traditionally seen M&A campaigns as among the leading options for increasing returns to shareholders, whether angling for companies to shed assets or merge with peers (see figure 1).

Figure 1. 2020 YTD campaign objectives2

After a period in 2020 when deal markets were quiet and valuations volatile, M&A activity is on the rise, with high corporate cash levels, low interest rates, and continued political uncertainty. Fifty percent of campaigns by activists in the 2020 third quarter had an M&A angle, up from just a third in the 2020 first half.3

The pandemic itself may be one possible stimulus for this greater M&A activism. Many businesses saw significant disruptions in their operations and shifts in their competitive position as a result of COVID-19. These and related changes may give activists the seeds for future campaigns in which they challenge the strategic decisions management has made to address the new circumstances. Furthermore, this environment has put pressure on the balance sheets of some companies that have struggled financially, which may create activist exposure. Therefore, activists are expected to opportunistically launch M&A-related campaigns, with a focus on companies that are underperforming and undervalued.

Nevertheless, opportunistic M&A campaigns may have new considerations given the increased focus on corporate purpose. The groundswell of social and political unrest, as well as the recent focus on corporate purpose, is changing the landscape. Customers are increasingly choosing to do business with companies that align with their values, and investors are increasing their ESG (environmental, social, governance) expectations on the companies in which they invest. How these trends affect activist investing remains to be seen and will likely put more pressure on board directors to consider the impact and preferences of any given transaction on a wider array of stakeholders.

In another intriguing example of how dramatically things have changed in the past year, labor productivity in the United States jumped even as companies scrambled to adjust to the economic upheaval. Worker productivity growth in the United States had been essentially flat in the decade since the Great Recession, but through the first three quarters of 2020, it jumped. This may be a macroeconomic clue that points to unexpected value in our new ways of doing business—increased digital interaction with their customers, or workforce changes such as work-from-home. Activists are likely to see in this and other “disconnects” new opportunities for boosting margins that can be added to their playbooks. As a result, we may see activists pushing companies to pursue digital transformation or change product mix based on the lessons of the crisis.

It may be a truism that after any slump in any market, a rebound comes. But activist investors are poised to do more than simply bounce back in 2021, given the array of factors that are aligned to motivate and expand their efforts in the aftermath of our pandemic year.

The active board: Preparation and response

The traditional guidance to boards—that they should think like an activist—gains weight and relevance during a time of upheaval, not to mention a period when a surge in activist investor campaigns may be expected. Accordingly, a starting point for boards is to acknowledge that activists fill a role. Board members need to engage proactively with the ideas and strategies these investors put on the agenda, principally that managements and boards should focus intently on how they plan to maximize both short-term and long-term value.

Activists will typically look in three main areas: potential to grow revenue, potential to boost margins, or potential portfolio changes. Boosting margins will often be preferable to revenue growth, as smaller gains have a bigger effect. (Raising a business’s margins from 5% to 6%, for example, can yield as much extra cash flow as a 20% revenue increase.) Portfolio changes are the most common focus, as already mentioned, and they have potential to give activists their biggest wins.

Our Deloitte guidance in the past has been framed around the idea that managements and boards should be able to keep control of the company’s fate, and this remains the operative principle. To do this requires self-assessment across a number of factors, such as how efficiently the company uses cash, whether its capital structure is fit for purpose, and refreshing the view of the risk landscape, risk profile, and risk appetite of the company (see figure 2).

Figure 2. How to be your own activist: A rigorous self-assessment4

![]()

Given the dramatic shifts of the past year, a proper assessment may demand a new focus on competitive position and market environment. For many companies, competitive positioning will likely have shifted in ways large and small in the past year. The relative performance of specific business units may also have been altered, and this is often a key area for activist attention, with a cold eye on operations that should perhaps be divested. A disaggregated analysis of divisional cash flows and valuation multiples may look very different today than it did a year ago, pre pandemic.

Board members should be ready to articulate a company’s strategic vision, which is why the above steps are so important and need to be up-to-date. They may need to articulate this publicly to all their shareholders, or privately when approached by an activist. Either way, they should be prepared to tell the story well before they are called upon to do so—and should demand of management a clear articulation of the company’s strategy and all relevant analysis to support it.

Given that portfolio options are in play, managements and boards should give careful consideration to where the company might be pruning and where it should be grafting. The pickup in carveouts and divestitures, which is already in evidence as M&A activity rebounds from last year’s slump, suggests companies are making strategic moves in response to the changes caused by the pandemic. Such moves may anticipate activist efforts to some extent and may show how boards and managements already have an activist viewpoint. Still, this is only beginning to play out, and activists may well see M&A moves that companies so far have rejected or failed to consider.

The M&A ideas in activist campaigns can vary. In 65% of the campaigns that had an M&A agenda in 2019, the activist goal was the sale of the company, the divestiture of noncore assets, or a full breakup of the company.5 In the balance of M&A-focused campaigns, opposition to a proposed transaction was the driver. In these cases, activists may be trying to boost the value of their position in a proposed deal, or they may believe a proposed transaction simply is not in the best interest of shareholders and should be blocked.

To truly have an activist mindset today, it has also become necessary to examine how the nature of activist campaigns has been changing. For one thing, there has been growing involvement by traditional long-only institutional investors. Activist Insight6 highlighted that 93% of institutional investors have become more accepting of activist investors in the past 12 months than in the past few years. Also, the field of play for activism is shifting to be more global. Boards of non-US companies may be wise to pay particular attention to the possibility that activism may finally reach their companies. And directors newly named to companies that become public through SPAC transactions should also be aware that their companies may quickly find their strategy and progress challenged by activists.

Overall, however, the fundamental principle to guide all board members should be to cultivate the ability to listen carefully and understand where activists are coming from. Recognize that investors make a choice to own your stock as a basic first step, and ask why investors are in your shares rather than a competitor’s. It’s a question that can inform much of what your company then does.

Conclusion

The year 2021 is expected to see growth in both shareholder activism and mergers and acquisitions. As a board director, the traditional advice to think like an investor has not changed, but the world around us certainly has. Continue to be prepared in identifying issues that might attract activists’ attention, proactive in communicating your strategy, and responsive to shareholder needs; consider how recent trends, such as political and social change and renewed corporate purpose, may change priorities for your stakeholders; and have a clear plan on how to respond if an activist launches a campaign to be able to maintain control of the situation from Day 1.

Endnotes

1 Activist Insight, October 2020.

2 Lazard’s Quarterly Review of Shareholder Activism – Q3 2020.

3 Lazard’s Quarterly Review of Shareholder Activism – Q3 2020.

4 Deloitte, Be your own activist: Developing an activist mindset.

5 Lazard’s Quarterly Review of Shareholder Activism – Q3 2020.

6 Activist Insight, October 2020.

Get in touch

Joel Schlachtenhaufen

Global Mergers & Acquisitions Leader | Consulting

Maureen Bujno

Center for Board Effectiveness | Deloitte & Touche LLP

Carey Oven

Enterprise Leader Development & Succession | Deloitte & Touche LLP

Recommendations

Time to act: Applying discretion to outstanding incentive awards in the era of COVID-19

On the board's agenda, December 2020