Profitable growth through a product and service catalog has been saved

Perspectives

Profitable growth through a product and service catalog

Strategies for group insurers in uncertain markets

From an ever-growing demand for products and services to ongoing tech transformations to the evolution of partnerships—macro trends have been taking the world of group insurance by storm. How can insurers separate themselves and their market offerings from the competition? Enter the product and service catalog.

Why implement a product and service catalog?

Recent macro trends have been compounded by organizational aspirations to accommodate customers and partners by offering the broadest possible product and service portfolios—further amplified by underwriting coveted cases involving marquee employer logos or brokers with significant influence. During the sales cycle for such cases, insurers often try to match products and services offered by the incumbent competitor—adapting their operations and technology in pursuit of the business while threatening performance and financial results.

Achieving profitable growth that satisfies the market and aligns with the insurer’s value proposition, operations, and technology capabilities often depends on a disciplined approach to product and service offering decisions. Developing a well-defined and actively governed product and service catalog can promote sales discipline, help insurers navigate evolving product needs, and establish a competitive position in an increasingly complex market. It may also serve as a reference guide for insurers in evaluating investments, determining partnerships, and building integrations across ecosystems.

Building a group insurance product and service catalog to drive profitable growth

Product and service catalog: From features to functions

At its core, a product and service catalog should include features that provide benefits and capabilities (e.g., life face amount, disability benefit period, portal customizations, and real-time integrations) with descriptions of tiered variations in offerings. The tiers potentially provide a structured separation of feature functionality based on complexity, level of customizations, and support levels (e.g., custom versus standard file feeds, weekday versus 24/7 support). Insurers should be strategic in mapping these tiers to consumer segments, accounting for requirement variations across demographics. While market dynamics will likely influence an insurer’s catalog, strategic goals, differentiating capabilities, and operations and technology should also be considered during development.

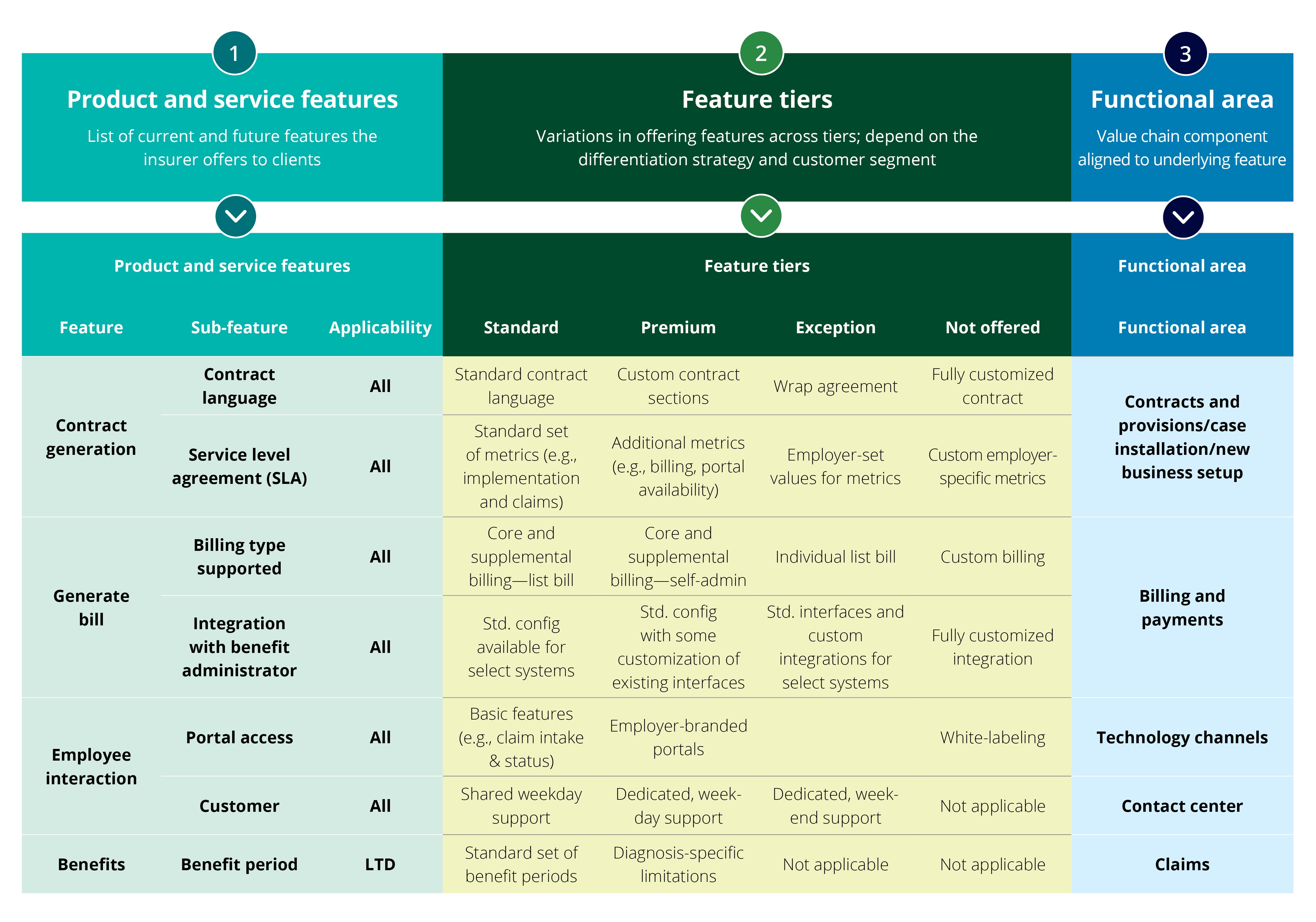

Figure 1. Illustrative product and service catalog

Product and service features include the capabilities and benefits to customers, partners, and internal stakeholders. Examples include integration with BenAdmin and HRIS systems, self-service portals, and on-call support. Products refer to commitments to adjudicate and/or pay a designated beneficiary a predetermined amount (e.g., some portion of someone’s salary) or reimburse the expense of a predefined benefit (e.g., teeth cleaning). From a group insurance perspective, product features are typically embodied in an insurance contract for which the timing and maximum amount are known at contract issuance. For the avoidance of doubt, contracts that do not include insurance risk (such as administrative services only (ASO), advice to pay (ATP), and leave administration are considered to be products in this construct. Services are sets of actions required by the insurer to interface with its customers (employers and employees) in administering products and are typically embodied in service-level agreements and performance guarantees.

Feature tiering is the structured separation of functional variability within a feature based on complexity, including the levels of customization (e.g., custom versus standard file feeds) and required support (e.g., custom versus standard file feeds; weekday versus 24/7 support). Feature tiering also helps address variations in customer needs and pricing decisions based on the level of support offered. While insurers should choose tiers that best suit the organization’s needs, a typical structure may classify features as standard, premium, exception, or not offered.

- Standard options reflect baseline capabilities that the insurer can profitably deliver based on its current operations and technology infrastructure and capabilities.

- Premium options are priced to deliver nonstandard service profitably, accounting for the added effort required to deliver.

- Exception options are avenues to request nonconfigurable options that trigger decision-making on whether to accommodate and price for one-off customization, incorporate functionality in the future, or deny the request.

- Not offered options should not be considered by the organization except in extraordinary circumstances. These will need to be approved by an executive leadership team for critical strategic purposes.

Functional area is the high-level category for market offerings based on an insurer’s value chain and functions (e.g., policy administration, billing, or claims). Aligning products and services with a functional area helps identify stakeholders and aids in establishing accountability.

Just as insurers segment their customers to determine the appropriate delivery models, they should also do so to develop an appropriately nuanced catalog. Insurers should base such segmentation on customer research and awareness of competitors’ offerings. Due to potential variations in needs across segments, the catalog maps the applicability of feature tiers for each segment. Generally, standard and not offered features are consistent across segments, while premium and exception are reserved for select segments based on the relative importance to the insurer. In some instances, the catalog may also have multiple features within tiers tailored to specific segments (e.g., list bill for small to medium cases and self-bill for larger cases).

Figure 2. Overlay of customer segmentation with feature tiering

Designing and building a product and service catalog

The process of designing and operationalizing should be done in a structured order to help ensure that the products, services, and associated feature tiers are well received within the organization and can create market differentiation in alignment with the broader organizational strategy. Before defining the catalog, the insurer should consider how it will align with its business strategy. A clear set of short- and long-term goals should be articulated for the catalog that serves as guardrails and helps the core team make appropriate decisions while designing it.

Benefitting from product and service catalog implementation

The central benefit of deploying a catalog is improved alignment across disparate stakeholders. When implemented well, it can potentially:

- Align sales and operations functions to sell what can be profitably delivered.

- Create clarity regarding the prioritization of investments to close operational gaps.

- Establish a framework for evaluating product and service offering extensions to satisfy the demands of high-value customers and partners.

By increasing alignment and reducing conflict in these ways, insurers can put themselves on a path to selling more business and enabling profitable growth.

Looking ahead

In the face of many challenges and evolving expectations, insurers must diligently curate profitable products and services. By implementing a product and service catalog, insurers can channel their organizational energies into building market-valued capabilities rather than competing reactively in an unprofitable arms race. For some deliberate insurers, a product and service catalog will preserve leading practices already in place across the organization to improve the likelihood of continued prosperity. For others that suffer more acutely from the whiplash of ever-changing product and service requests, a well-executed product and service catalog implementation may help avoid providing products and services that are not fiscally prudent. In both cases, building a product and service catalog will likely be essential for going to market more efficiently and profitably.

Get in touch

Managing Director

Group, Voluntary,

and Worksite Practice Lead

Deloitte Consulting LLP

Senior Manager

Insurance Strategy &

Transformation

Deloitte Consulting LLP

Manager

Insurance Strategy & Technology

Deloitte Consulting LLP

Recommendations

COVID-19 impact on group insurance companies

Combating the current crisis. Preparing for the future.

Digital transformation in insurance: Digital ecosystem connectivity

Redefining the group insurance ecosystem