Semiconductor sustainability: Becoming business as usual has been saved

Perspectives

Semiconductor sustainability: Becoming business as usual

Four strategies for industry-wide sustainability integration

Earlier articles in Deloitte’s Semiconductor Sustainability series have discussed the overall sustainability landscape and delved into each sustainability strategy. As the closing chapter in the series, this article explores the ways semiconductor companies are revising sustainability strategies and integrating them into the business.

Context:

Previous articles in this series have discussed the range of pressures for semiconductor companies to address sustainability. We have also discussed the specific drivers that have been leading to the adoption of a set of sustainability strategies that range from new investments in manufacturing and deeper engagement of supply chain partners; to the redesign of products to help reduce their energy use and enable circularity; through development of new sustainability-related revenue streams and service offerings.

The breadth of these pressures, drivers, and strategies shows that sustainability considerations have become important to almost every element in the business of manufacturing and supplying semiconductor products. It is no surprise that semiconductor company leadership today sees sustainability as a central factor in the success of their business and that companies have been revising both the content and structure of their sustainability goals and strategies to reflect this. In general, as companies’ experience with sustainability has matured, the representative approach has evolved from being a somewhat separate compliance- and brand-related effort managed by a distinct environmental, social, and governance (ESG) team, toward a priority that is co-owned by executive leadership and increasingly integrated throughout the business.

Discover how the semiconductor industry is revising sustainability strategies and integrating them into the business.

How are the market drivers and opportunities for delivering new sustainability-related offerings manifesting for semiconductor manufacturers?

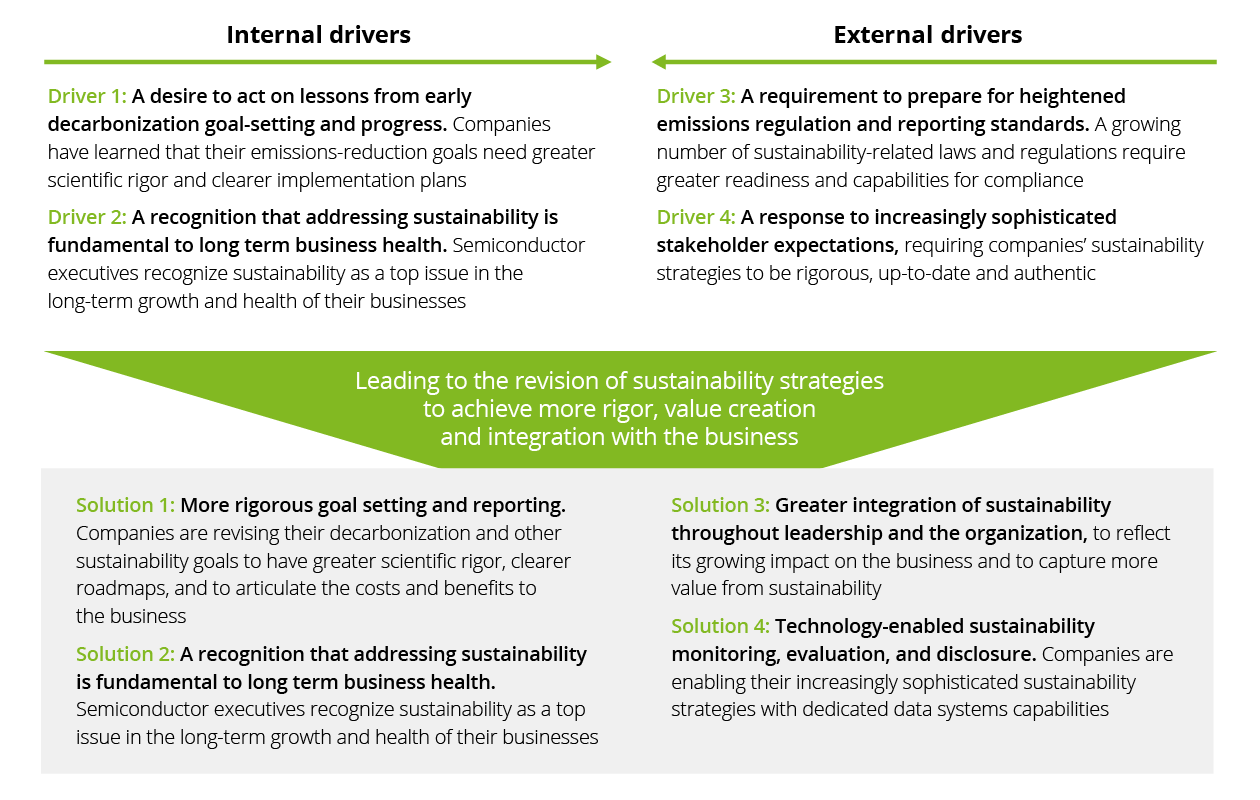

Drivers and solutions for sharpening and integrating sustainability strategy into the semiconductor business

- Driver #1: A desire to act on lessons from early decarbonization goal-setting and progress.

Following the Paris Agreement’s goal to limit global temperature rise by 1.5°C or less, many semiconductor companies announced goals to reduce their greenhouse gas (GHG) emissions. AMD,1 Wolfspeed,2 and Analog Devices,3 for example, have each announced a goal of reducing scope 1 and 2 emissions by 50% by 2030. A visit to semiconductor manufacturers’ websites will likely reveal that the majority have set, or are planning to set, decarbonization goals.

With the benefit of several years’ experience, two broad lessons have emerged. First, early decarbonization goals often lacked a clear scientific basis and feasibility analysis and fell short of guiding ambitious, long-term action. Of the 1,000 companies that disclosed data via the 2017 CDP Climate questionnaire, 89% had already set targets for emissions reduction while only 20% set emissions reduction targets that extend to 2030 or beyond.4 Second, progress toward reducing emissions has frequently lagged the timeline needed to achieve those goals. An analysis led in part by the Semiconductor Climate Consortium shows that the industry as a whole is not on track to reach the required net-zero emissions mark by 2050 and will exceed its allocated emission budget by 3.5 times.5 - Driver #2: A recognition that addressing sustainability is fundamental to long-term business health.

The business sustainability strategies described in earlier articles in this Semiconductor Sustainability series point to how the topic is becoming fundamental to semiconductor operations and market strategies. Looking to the longer term, Deloitte’s global Turning point report6 finds that unchecked climate change could cost the global economy US$178 trillion over the next 50 years, unless global leaders unite in taking action to address its causes. Meanwhile, the same analysis indicated that by investing in a systemic net-zero transition, the global economy could gain US$43 trillion over the same period.

Deloitte’s 2023 CxO sustainability report7 found that 42% of CxOs rated climate change as a “top-three issue” with only economic outlook ranking higher; 61% said climate change will have a high or very high impact on their organization’s strategy and operations over the next three years; and 75% said their organizations have increased their sustainability investments over the past year (with nearly 20% reporting that they had increased investments significantly). With this growing centrality of sustainability to current and future business health, the topic is firmly on the executive and board agendas at semiconductor companies. - Driver #3: A requirement to prepare for heightened emissions regulation and reporting standards.

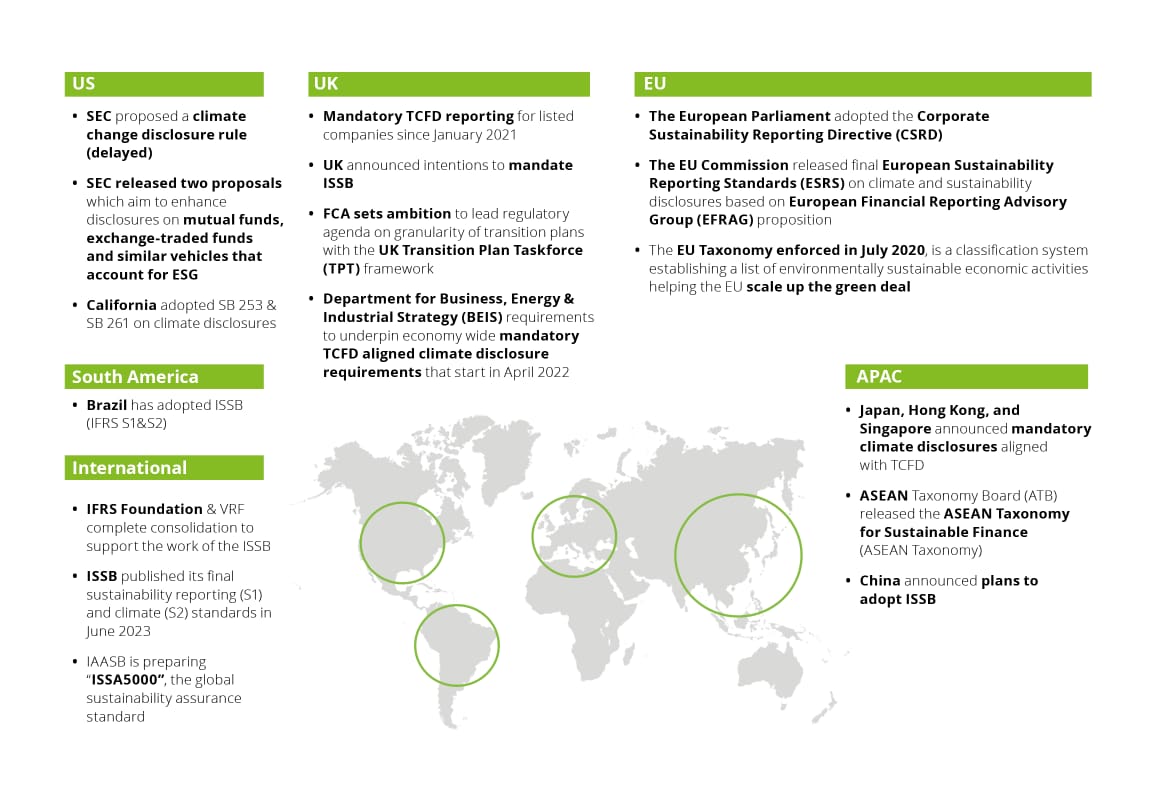

Semiconductor companies are subject to a growing number of sustainability-related laws and regulations. These span multiple geographies and are growing in both volume and sophistication and depth of implications for the business. The European Union’s Corporate Sustainability Reporting Directive (CSRD)8 broadly requires companies to publicly disclose and verify their greenhouse gas emissions, while its future Carbon Border Adjustment Mechanism (CBAM) is likely to tie emissions embedded in semiconductor products to the cost of market access. In the United States, California has passed legislation requiring disclosure of emissions data9 and climate-related financial risk disclosure,10 and the SEC is expected to issue US climate disclosure guidelines.11 Additionally, in the United States, the Inflation Reduction Act12 includes incentives for energy efficiency that are likely to affect the market for semiconductor products, while the CHIPS Act13 includes incentives for semiconductor companies to review their investment strategies. In Asia, there is growing pressure to expand the availability of renewable energy to help semiconductor companies reduce the carbon footprint of fabrication and packaging.14

The increasingly complex regulatory landscape, combined with a trend toward compliance with (and reporting on) regulations requiring greater reach into both company operations and supplier networks is leading companies to revisit their sustainability regulatory preparedness and approaches to compliance. Sixty-five percent of respondents to Deloitte’s 2023 CxO sustainability survey15 said the changing regulatory environment has led their organization to increase climate action over the past year.

Emissions reporting standards are being adopted across all major economies16

- Driver #4: A response to increasingly sophisticated stakeholder expectations.

In earlier articles in Deloitte’s Semiconductor Sustainability series, we’ve discussed the increased sustainability sophistication and expectations of end consumers, customers, regulators, and capital providers. This is exerting pressure for companies’ sustainability strategies to be rigorous, up to date, and authentic. In Deloitte’s 2023 CxO sustainability survey,17 more than half of respondents said that employee activism on climate matters has led their organizations to increase sustainability actions over the past year, with 24% reporting that it led to a “significant” increase. Respondents’ relative weighting of alternative sources of stakeholder pressure for sustainability action is summarized in the following graphic.

Responses of “Large” or “Moderate” to the question: “To what extent does your company feel pressure to act on climate change from your stakeholders?”18

In response to these drivers, semiconductor companies are sharpening and revising their sustainability-related strategy and organization. What specific solutions are they pursuing?

Solution #1: More rigorous goal-setting and reporting.

Having gained several years’ experience in both stakeholders’ perspectives and the practicalities of setting and working toward emissions reduction goals, some companies are revisiting and revising their decarbonization goals. Two themes appear predominant in this trend: Aligning goals with a highly credible international standards and setting goals in parallel with developing business plans and road maps for achieving them.

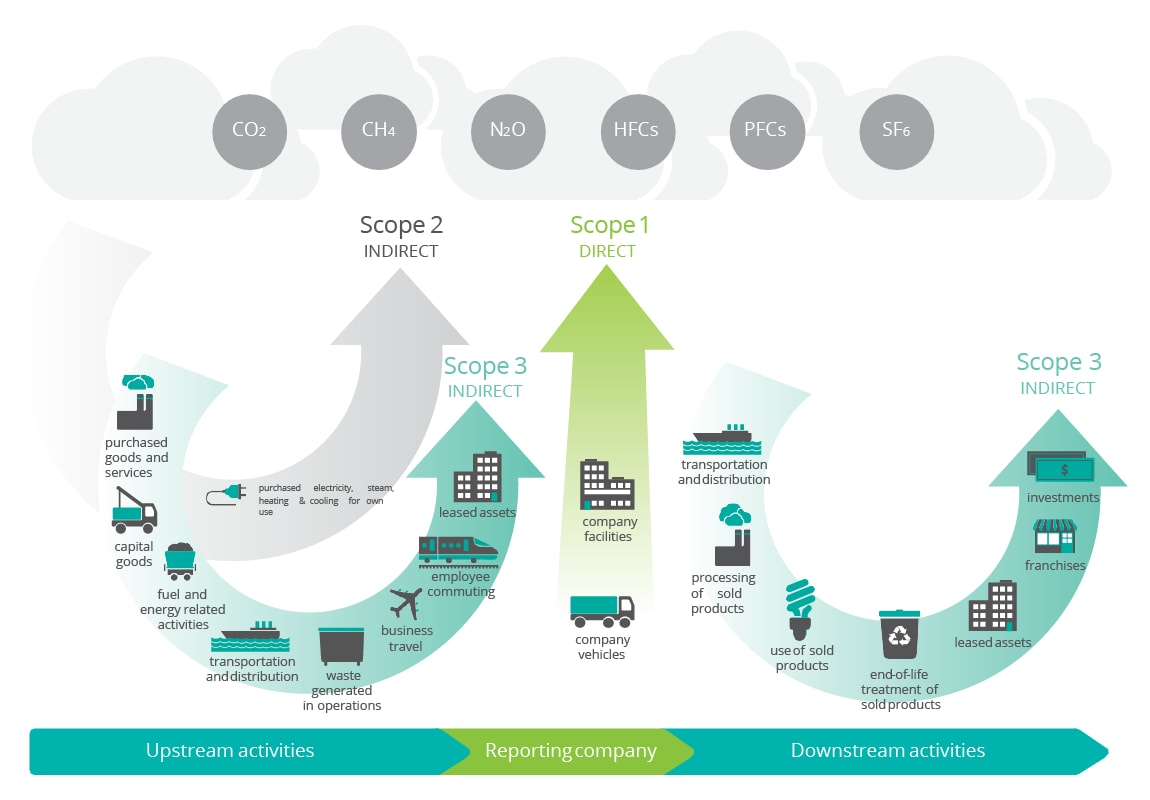

While multiple standards exist, the Science Based Targets initiative (SBTi)19 has emerged as a highly credible standard for net-zero targets. SBTi developed the definitions for scopes 1, 2, and 3 emissions, as well as for specific emissions categories within each scope. It requires companies to address the more challenging scope 3 emissions, in addition to scopes 1 and 2, and also is consistently developing and publishing guidelines to setting emissions reduction targets for individual economic sectors. At the start of 2019, just one semiconductor company had a SBTi-approved target. As of October 2023, 22 semiconductor companies now have science-based targets.20 Onsemi, NXP, and Analog Devices each have committed to SBTi goals, for example; and others, such as Allegro Microsystems, are in the process of evaluating science-based targets.

SBTi requires companies’ emissions reduction goals to address scopes 1, 2, and 321

Source: Greenhouse Gas Protocol

The process for establishing clear science-based targets has advanced significantly in recent years. Broadly, the initial step involves measuring or estimating a company’s baseline emissions, identifying their sources, and prioritizing their relative materiality. There are several accepted methods for establishing the emissions baseline, ranging from estimations based on a database of emissions intensity factors through to direct measurement. Following this, databases of abatement technologies and processes can be consulted and assessed in light of a business’s operations and supply chain, as well as its ambitions, to arrive at credible emissions reduction approaches, timelines, investment plans, goals, and reporting. The result can be a much more rigorous, credible, informed, and achievable set of emissions reduction goals than was possible just a few years ago.

In addition to emissions reduction, many companies have also expanded the breadth of their sustainability goal-setting to include other environmental and social goals beyond climate. It is increasingly recognized that rigorous sustainability targets can strengthen a business and “enhance revenue and lower operational costs by developing new business models and low-carbon processes, technologies, services, products and other sources of value.” 22

Solution #2: Extending and sharpening sustainability strategy.

Deloitte’s experience working with organizations in the semiconductor sector has shown that there are broadly four complementary approaches to generating business value from investment and initiatives in sustainability. These are shown in the graphic below. Typically, a representative semiconductor company may have first began engaging in sustainability from the perspective of seeking to meet regulator and other stakeholder expectations as sustainability became more prominent on those stakeholder’s motivations. Another motivation may have been the need to manage risk, both the brand value and regulatory compliance risks related to compliance and transparency, and tangible business risks associated with sustainability such as raw materials access or the possibility of carbon taxes being imposed by some jurisdictions. These two broad approaches to the business value associated with sustainability tended to focus on avoiding value destruction of business costs and tended to lead to sustainability strategies that were viewed as somewhat separate from the core business and were often managed as initiatives run by distinct ESG or sustainability teams. We can think of these as “first generation” sustainability strategies, represented in the top half of the graphic.

The four sources of business value from sustainability

The articles in this Semiconductor Sustainability series have focused on a recently emerging set of “next-generation sustainability strategies” that tend to focus on the proactive generation of direct and indirect value for the business. These approaches to generating value from sustainability investments are represented in the bottom half of the graphic: Investment in the latest low-emissions semiconductor manufacturing processes and engaging with supply chain partners to track and reduce emissions can drive process innovation. Efforts to reduce products’ life cycle energy use, introduce circularity, and develop new sustainability-related businesses and products were discussed quite extensively in earlier articles and can capture opportunities to directly drive business growth. Taken together, these efforts can shape the future evolution of the semiconductor industry. In our work with semiconductor companies, Deloitte is being asked with increasing frequency to help companies chart their course for future market-based value generation related to sustainability.

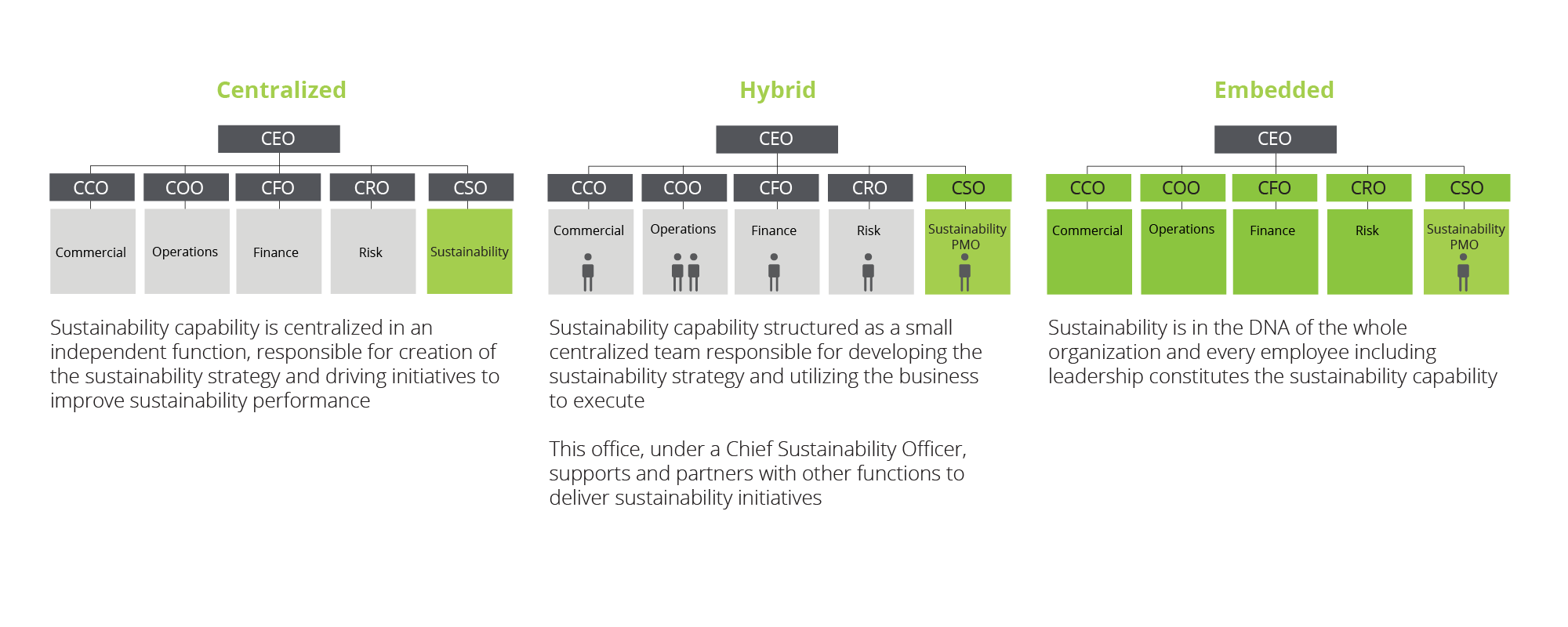

Solution #3: Greater integration of sustainability throughout leadership and the organization.

As semiconductor companies’ sustainability strategies have become more ambitious, sophisticated, and business-centric, companies have found increasing benefit from integrating their sustainability teams and functions with both overall corporate leadership and the business. Early sustainability strategies that emphasized regulatory compliance, reporting, and stakeholder management could be adequately managed as largely distinct initiatives, managed by teams that may have reported to the general counsel, corporate public relations, or investor relations.

As more evolved sustainability strategies have emerged, there has been a need to engage business units and functions more directly and more deeply. For example, procurement needs to lead engagement of supply chain partners in addressing scope 3 emissions reduction: business unit product management, sales, and corporate strategy are essential to developing new sustainability-related revenue streams; product design, engineering, and operations are essential to the introduction of circularity, while manufacturing is a key internal collaborator for reducing in-house emissions. As a result, semiconductor companies are increasingly involving the full executive group in leading sustainability—and have been moving from centralized sustainability teams toward integrating them with other functions and business units. Strategies tend to succeed when others within the business—not the ESG team alone—drive progress, and many semiconductor companies are revising their business models, organizational structures, governance processes, and networks of involved stakeholders to embed sustainability into their company’s DNA.23 This is illustrated in the next graphic.

Centralized, hybrid, and embedded approaches to organizing the corporate sustainability function

A good example of this evolution in maturity is provided by Allegro Microsystems.24 Like many other semiconductor companies, Allegro began its sustainability journey with a set of solid but largely disconnected initiatives and a small central sustainability team reporting to the general counsel’s office. This initial team tracked and supported initiatives and supported basic sustainability reporting and questions. Recently, Allegro convened its executive leadership over a period of several months to develop a holistic organization-wide sustainability strategy. Allegro’s revised sustainability strategy spans all elements of the business, and each pillar of the strategy is now led by an executive responsible for its progress and for embedding it in the business.

Putting this level of sustainability integration into action involves a range of actions, from elevating sustainability to be a part of overall corporate strategy, to restructuring capital allocation, to adopting performance-based incentives to drive accountability.25 As described repeatedly in earlier articles in this series, more fundamentally, many semiconductor companies are rethinking the core of how they do business and placing sustainability at the center through new products, business models, and partnerships that position them to win in a low-carbon, more equitable future.

Solution #4: Technology-enabled sustainability monitoring, evaluation, and disclosure.

As sustainability becomes ever-more integrated across the business, corporations in the semiconductor and other sectors are building sustainability data and analysis capabilities into their technology, systems, and processes. The aim is to enable their organization to collect and track information, derive insights, identify strategic opportunities, and meet or exceed requirements for both financial and nonfinancial climate-related data to support sustainability-related management decisions and disclosures.26 Enterprise resource planning and manufacturing systems often lack integration, and there are opportunities for increased business efficiency as well as sustainability management and reporting from the integration of both systems and data. Similarly, as Generative AI approaches are introduced to help optimize and manage manufacturing and process efficiency, they also can help model and optimize sustainability performance.

A growing range of sustainability-related data platforms are available, with both mainstream enterprise resource platforms adding sustainability capabilities, and a range of new platform providers focused on sustainability data and reporting.27 To secure the maximum benefit from investing in these capabilities, a semiconductor company should thoughtfully assess its existing IT and data architecture; its sustainability data, reporting, and analysis needs; and the holistic capabilities of each potential sustainability data platform to meet these.

Take a deeper look at industry drivers and solutions in our Semiconductor Sustainability series

In conclusion:

Throughout this Semiconductor Sustainability series, we have highlighted the growing breadth of sustainability strategies being pursued by semiconductor companies; how profoundly sustainability considerations are now embedded in the leading semiconductor businesses; and the ways in which sustainability enhances value generation. As sustainability continues to be embedded in the corporate goals, strategy, organization, and systems of leading semiconductor companies, we can anticipate it becoming ever-more central to the future of the semiconductor sector. Indeed, this is essential if the potentially harmful sustainability impacts of continued growth of the sector are to be offset by its positive impacts on our economies and society.

Get in touch

Endnotes

1AMD, Environmental sustainability page, accessed January 17, 2024.

2Wolfspeed, Sustainability page, accessed January 17, 2024.

3Analog Devices, “Analog Devices advances climate strategy and commits to net zero emissions by 2050,” press release, April 12, 2021.

4Deloitte, “Establishing science-based emissions reduction targets for insight, innovation, risk management, and competitiveness,” 2019.

5Gaurav Tembey et al., “Transparency, ambition, and collaboration: Advancing the climate agenda of the semiconductor value chain,” SEMI, 2023.

6Pradeep Philip, Claire Ibrahim, and Cedric Hodges, The turning point: A global summary, Deloitte, 2022.

7Deloitte, Deloitte 2023 CxO sustainability report, 2023.

8European Commission, “Corporate sustainability reporting,” January 17, 2024.

9Wolfspeed, Sustainability.

10Analog Devices, “Analog Devices advances climate strategy and commits to net zero emissions by 2050.”

11US Securities and Exchange Commission (SEC), “SEC proposes rules to enhance and standardize climate-related disclosures for investors,” press release, March 21, 2022.

12Carrie Falkenhayn and Jonathan Traub, “The Inflation Reduction Act of 2022: What’s in it?,” 9:00 (podcast), Tax News & Views, Deloitte, July 29, 2022.

13Mark LaViolette, David Kotok, and Joniel Cha, “US semiconductor industry needs public-private partnerships for an innovation system,” Deloitte, accessed January 17, 2024.

14Judy Lin, “Taiwan’s semiconductor industry faces dilemma of carbon lock-in,” DigiTimes Asia, July 26, 2023.

15Deloitte, Deloitte 2023 CxO sustainability report.

16Deloitte analysis.

17Deloitte, Deloitte 2023 CxO sustainability report.

18Ibid.

19Science Based Targets initiative (SBTi), homepage, accessed January 17, 2024.

20SBTi, “Companies taking action – Dashboard,” accessed January 17, 2024.

21Greenhouse Gas Protocol, Corporate Value Chain (Scope 3) Accounting and Reporting Standard (September 2011), p. 5.

22Analog Devices, “Analog Devices advances climate strategy and commits to net zero emissions by 2050.”

23CB Bhattacharya and Rob Jekielek, “Sustainability progress is stalled at most companies,” MIT Sloan Management Review, July 20, 2023.

24Allegro MicroSystems, “Environmental, social, and governance (ESG),” accessed January 17, 2024.

25Deloitte, “The 5-step climate-led transformation framework,” accessed January 17, 2024.

26Deloitte, “Step 5: Regularly monitor and report,” 2023.

27Michael Steinhart et al., “Regulations take effect: ESG reporting software sales are expected to soar in 2024,” Deloitte Insights, 2023.

Recommendations

Semiconductor | Deloitte US

Deloitte's semiconductor consulting practice can solve critical issues. Explore semiconductor industry trends, from M&A to cloud to IoT, to help drive growth.