Up-C IPOs gaining momentum has been saved

Perspectives

Up-C IPOs gaining momentum

InFocus: Benefits and complexities of an Up-C structure

Explore Up-C IPOs and how the Up-C structure has become common for IPOs of companies that historically have operated and been taxed as partnerships.

Explore content

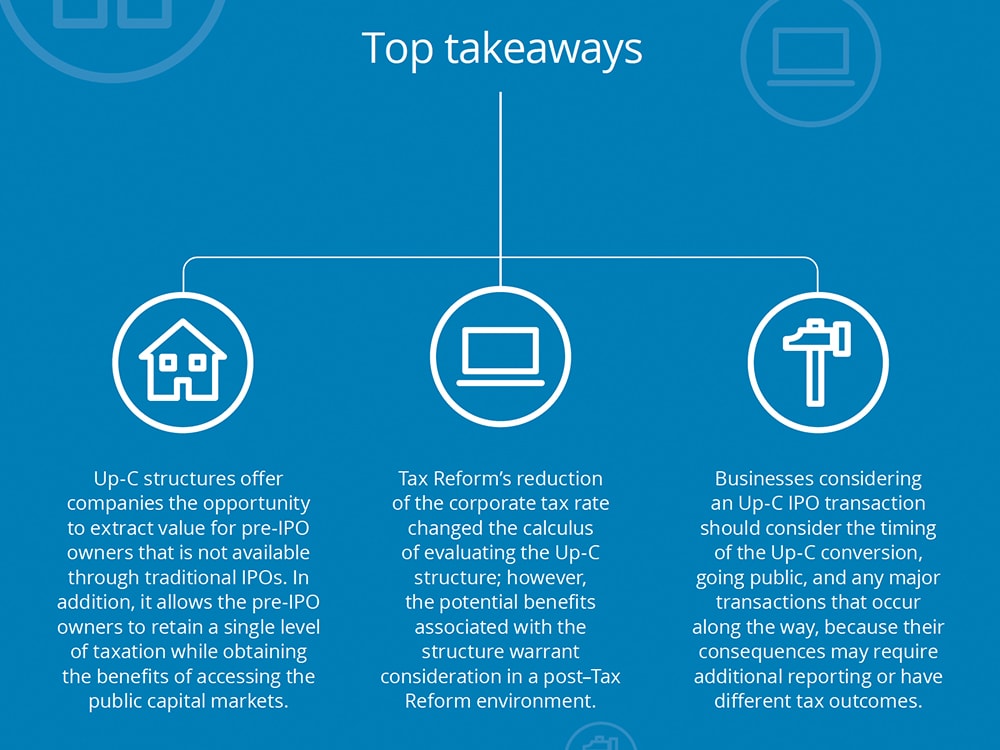

- Top takeaways

- Current market update

- Overview: Up-C IPOs

- Up-C structure may benefit owners and investors

- Up-C IPO trends (2009–June 2020)

Click image to enlarge

Current market update

The coronavirus pandemic has caused a significant decline in economic activity in the United States and around the globe. The Federal Reserve has stepped in to help offset the deep contraction in economic activity by undertaking a number of actions to help the financial markets. Actions taken since early March include cutting the federal funds rate to near zero, buying large amounts of securities, and providing low-interest-rate loans to securities firms. All of these actions are aimed at stabilizing and restoring faith in markets so that credit can continue to be provided where it is needed. What began in late February 2020 as one of the sharpest corrections in the history of the global equity markets has since emerged as one of the strongest as a result of the Fed’s actions.1 Whether this rebound continues or even remains stable is unclear, but yields on fixed income investments are likely to remain at low levels over the near-to-medium term. As a result, investors should be aware of the potential for both higher yields and growth. One of the alternatives that may be a consideration is the initial public offerings (IPO) market because of the potential to earn higher returns.

In the past month, the IPO market has made a strong resurgence, with several private equity–sponsored, umbrella partnership corporation (Up-C) structures coming to market. Initial performance has been very good and may signal continued strong interest in future IPOs.2

Overview: Up-C IPOs

Over the past 20 years, the Up-C structure has become increasingly common for IPOs of companies that historically have operated and been classified for US tax purposes as partnerships. This trend has been particularly apparent with private equity (PE)–backed businesses because an IPO is a commonly used exit strategy for portfolio investments held by such businesses. This article provides an overview of the potential benefits and complexities associated with implementing an Up-C structure and examines trends in Up-C transaction, with a focus on potential implications of certain provisions of the tax legislation commonly referred to as the Tax Cuts and Jobs Act of 2017 (Tax Reform).

Up-C structure may benefit owners and investors

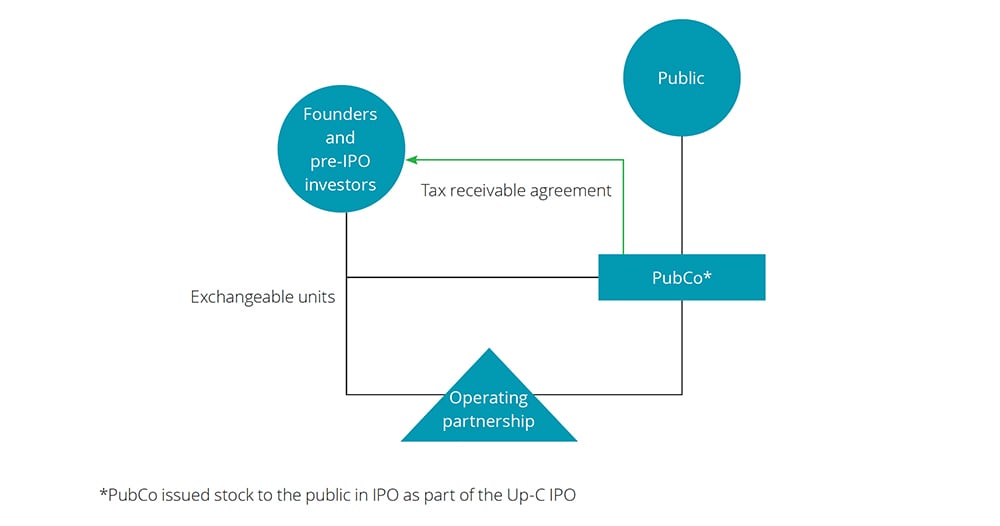

When a company prepares for an Up-C IPO, it generally forms a new entity organized as a corporation (PubCo), the shares of which will be sold to the public in an IPO.3 PubCo then uses the IPO proceeds to acquire an interest in the existing partnership whereby public shareholders have an indirect interest in the partnership. Figure 1 illustrates a simplified Up-C structure.

An Up-C structure may provide favorable tax benefits to pre-IPO owners. It allows them to access the public capital markets while maintaining ownership through a partnership, which continues to receive the benefits of a single level of taxation until the pre-IPO owners sell their interests. The Up-C structure also provides pre-IPO owners with the right through an exchange agreement to exchange their partnership interests for shares of the PubCo on a one-for-one basis. These exchanges generally result in a step-up in the tax basis of the partnership’s assets, which, in turn, increases amortization and/or other deductions available to the PubCo. A significant benefit of the Up-C is in its ability for historical owners of the partnership to receive a premium on the value of their partnership units.4

In a typical Up-C IPO, the pre-IPO owners negotiate for the right, through a tax receivable agreement (TRA), to receive payments for a portion (typically 85 percent) of tax savings the PubCo realizes arising from the exchanges (figure 1). This value, combined with the following additional potential benefits, offers a compelling proposition for partnerships to consider in advance of an IPO:

- An Up-C IPO structure offers liquidity to pre-IPO owners through their ability, subject to certain limitations, to exchange partnership interests for PubCo shares while retaining a single level of taxation by owning their interest directly in the pass-through structure.

- Pre-IPO owners are able to maintain voting control over the PubCo by issuing high voting shares.

- The Up-C structure can use cash, PubCo shares, or partnership units to fund future acquisitions.

- A partnership has flexibility in compensating employees by issuing restricted PubCo stock and/or profits interests in the operating partnership.

- An Up-C structure typically contains termination and change-of-control provisions with respect to the TRA that serve as effective antitakeover mechanisms.

- All of the aforementioned benefits should be weighed against the administrative complexity of creating and maintaining the Up-C structure. Potential challenges include:

- Maintaining partnership books and records and tracking partnership unit exchanges

- Designing a policy for addressing the buildup of excess cash at the public company due to the disparity between the corporate tax rate and individual partners’ tax rates, which increased as a result of Tax Reform (the partnership will typically make periodic distributions to its owners, including the PubCo, to enable its partners to pay taxes on their allocable share of partnership income)

- Maintaining partnership books and records and tracking partnership unit exchanges

- Addressing complex financial reporting and accounting issues associated with the Up-C transaction and subsequent reporting, such as:

- Determining the relevant accounting model for the IPO transactions (for example business combination versus common control accounting)

- Accounting for share-based payments under Accounting Standards Codification (ASC) 718

- Applying the consolidation guidance in ASC 810 to determine if the voting interest or variable interest model applies

Figure 1

Up-C IPO trends (2009–June 2020)

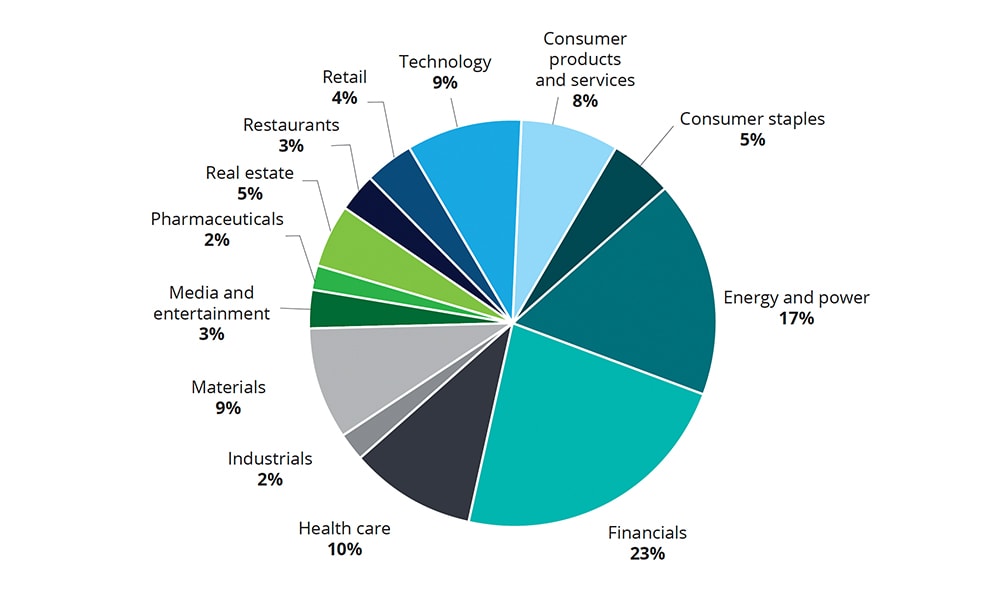

Up-C IPOs are a relatively small percentage of the overall IPO pool—from 2009–2019, there were 94 Up-C IPOs, which represented 5 percent of total IPOs—and generally have been concentrated in the financial services (such as investment management) and energy industries (figure 2). In the first half of 2020, there have been five Up-C IPOs, which represent 7 percent of total IPOs.5

Figure 2

Tax Reform’s impact on Up-C transactions

US Tax Reform decreased the top corporate tax rate from 35 percent to 21 percent, which reduces the value of the potential tax amortization and deductions to the PubCo and corresponding TRA payments. Despite this reduction in value, businesses classified for US tax purposes as partnerships continue to consider the Up-C structure (see figure 3), as it provides the pre-IPO owners with incremental value that may not be available through a traditional IPO.

Figure 3

Market evidence suggests that, despite a lower corporate tax rate post–Tax Reform, the appetite for the Up-C structure continues to be strong. The annual average of Up-C IPOs from 2009–2017 (pre–Tax Reform) was eight, with a peak of 16 Up-C IPOs in 2013 and 2014, respectively. In 2018 and 2019, post–Tax Reform, 12 and nine Up-C IPOs closed, respectively. As a percentage of total IPOs, 2018 and 2019 were above average in the number of Up-Cs relative to total IPOs (10 percent and 8 percent, respectively, versus an average of 5 percent from 2009–2017).6

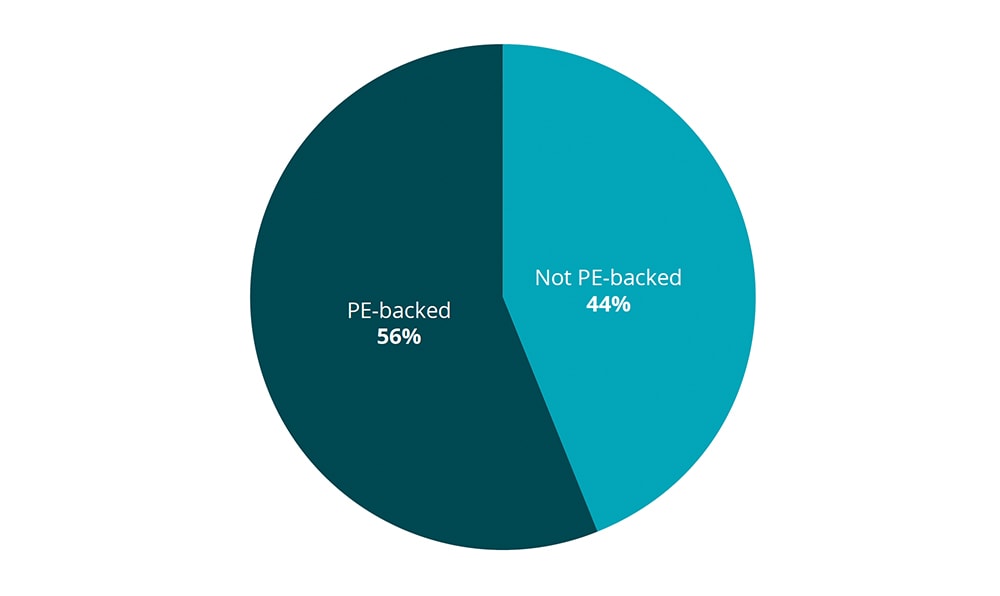

The sustained use of PE-backed IPOs (figure 4) is expected to be a continued source of Up-C expansion.

Figure.4

What’s next?

Businesses considering an Up-C IPO transaction should consider the timing of the Up-C conversion, requirements of a PubCo, and any significant transactions that occur along the way (for example, acquisitions or divestitures) because the consequences of such transactions may require additional reporting or influence tax outcomes.

If you want to learn more about the potential benefits and complexities of executing an Up-C IPO, contact your Deloitte engagement team or one of the contacts below.

Explore additional financial services perspectives in the InFocus series

Staying on top of new financial services industry trends, emerging technologies, and changing regulations isn’t easy—it’s not enough to rely on the headlines to understand the complete picture. Our InFocus series takes a deeper dive into the issues that affect financial services organizations and gives you the insights needed to make more informed decisions.

Endnotes

1 https://www.wsj.com/articles/global-stock-markets-dow-update-6-30-2020-11593508397.

2 https://www.barrons.com/articles/ipos-are-back-why-vroom-zoominfo-and-shift4-stocks-have-soared-51591999919.

3 Deloitte Center for Financial Services, Positioning for success in private equity: The Up-C advantage, 2015.

4 The premium on the value of partnership units is equivalent to the present value of a percentage of the tax savings to the PubCo on its acquisition of the partnership units in exchange for PubCo shares.

5 Deloitte analysis of Intelligize data set and full IPO population collected by Thomson One.

6 There were 289 and 282 IPOs in 2013 and 2014, respectively, representing the top two years for IPO volume from 2009–2019. Source: Thomson One.

Get in touch

| Brian Finnegan Senior manager Audit & Assurance Deloitte & Touche LLP |

Tania Taylor Partner, Audit & Assurance leader Investment Management Deloitte & Touche LLP |

Sean Brennan Partner Deloitte Tax LLP |

Eric Savoy Partner Deloitte Tax LLP |

Recommendations

COVID-19: Financial impacts and disclosures

Considerations for banking and capital markets, insurance, and investment management

COVID-19: Virtual close preparedness

Preparation, planning, and execution of the virtual close