The arc of innovation in the oil and gas industry has been saved

Analysis

The arc of innovation in the oil and gas industry

Using US patent databases to track trends

The oil and gas business has a rich history of continuous innovative and technological advances, across the value chain, that have enabled the development of new and challenging resource types and given the ability to respond to customer needs, all while continually improving safety and environmental performance. This research series uses the US patent database to tell the story of oil and gas innovation.

Oil and gas patent series

Issue one: Tracking innovation in oil and gas patents

A discussion of the role and impact of government funded research.

Issue two: Patenting innovation in oil and gas

A portrayal of the arc of innovation in the oil and gas industry over time, as it relates to other industries, and a description of the factors contributing to the emergence of hydraulic fracturing technologies—perhaps the most significant oil and gas innovation area of the past two decades.

Patenting innovation in oil and gas

Part 1: How oil and gas patents have changed over time

Charting growth: A look at the growth trajectory of oil and gas patent filings

Linking for innovation: The changing O&G knowledge network

How knowledge has grown in the oil and gas space over time

Measuring innovation: The Energy Innovation Index

Part 2: Hydraulic fracturing: A case study in innovation

Studying growth: A look at patent filing trends

Inspiring innovation: Past patents show the way for future innovation

Branching out: Hydraulic fracturing looking outward for inspiration

Looking forward: The future lies in building networks of innovation

How can we help you apply these findings to your business?

Access the full methodology report: Creating an innovation index from patent data

Subscribe to receive notifications about new industry reports.

Part 1: How oil and gas patents have changed over time

Charting growth: A look at the growth trajectory of oil and gas patent filings

After many years of running on a parallel course, the pace of oil and gas patent filings has recently diverged from the overall trend in patents.

In both O&G patents and the entire patent universe, filings dipped going into the Great Recession in 2008. This decline was followed by a period of rapid intellectual property acquisition in both segments that lasted until 2012. However, after 2012, while the oil and gas industry continued to produce a significant number of patents, it did not generate the same rates of increase as the rest of the patent universe. While the absolute number of oil and gas patents was considerably higher than a decade earlier, the five-year compound annual growth rate for oil and gas patents was 1.3 percent compared to 5.7 percent for the overall patent universe.

Increase in patent activity over time

In spite of general steady growth, some O&G technologies showed an uptick in growth rate over the defined period. Earth drilling, the single largest O&G technology area has grown at a rate higher than the rest of the patent universe. In addition, metalworking, dredging, and gas turbine technologies have all grown substantially faster than the rest of the patent universe (as shown in the figure below). The same data shows that other categories of patents, specifically those related to cracking hydrocarbon oils, acyclic or carbocyclic compounds, and chemical or physical processes used in O&G applications (patents can have multiple classifications), have had markedly lower rates of growth than the rest of the patent universe.

While these changes in the volume of original filings allow us to identify the dominant new technology areas for oil and gas and determine how their relative importance is changing, a look at trends in patent citations can help in understanding how knowledge flows between different O&G technologies.

Volume by technology

Linking for innovation: The changing O&G knowledge network

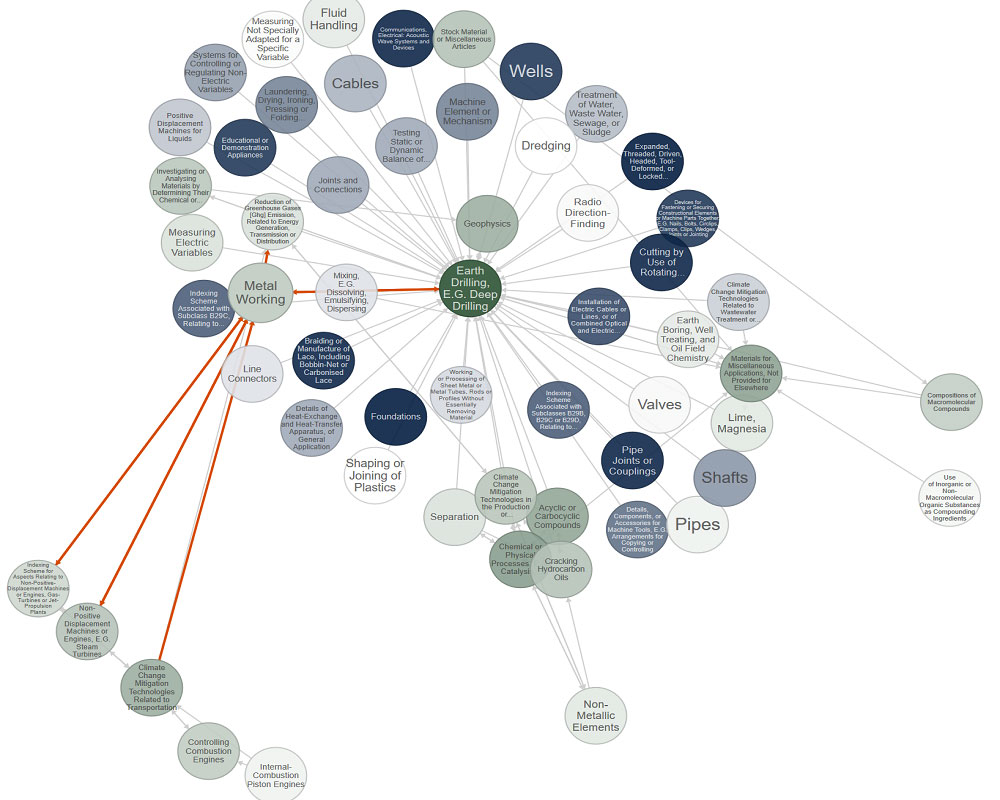

Granted patents from the USPTO reveal a great deal about the oil and gas knowledge network.1 By measuring how knowledge flows to and from technologies within the oil and gas industry, we can learn how the structure of knowledge in the industry is evolving. In Deloitte’s patent knowledge maps, circles represent technology categories while connections between them appear when patents from one technology draw on innovations from patents in other technology areas. In 2006, almost all major innovation links in oil and gas, except for a few stragglers, directly related to earth drilling (highlighted in the center of the knowledge map).

How knowledge has grown in the oil and gas space over time

Select the year you want to examine, and then click on a technology to show how its links to other technologies have changed over time. If you want to search for a specific technology, start typing in the search box to select from the list of technology categories available.

-

Year :

This pattern of dominance by earth drilling technology continued mostly unchanged until 2012. By this point, distinct other technology clusters had emerged, and while earth drilling was still dominant, it was not as uniformly dominant as in prior years.

Knowledge map for earth drilling in 2012

Access the interactive graph for more details about the knowledge flow by year for each technology.

By 2012, lesser-cited categories such as metalworking (patents comprising of new processes, tools, machines, and apparatus made from metal) had emerged as a key linking technology, or a bridge, between earth drilling and other O&G-related technologies. Combined with its high growth rate of 192 percent from 2006–2015, metalworking has become a technology area that has not only grown in volume but seemingly also in its significance within the oil and gas knowledge network.

Deloitte’s analysis also identified individual patents that were frequently cited by oil and gas patents. Surprisingly, a significant focus of quite recent metalworking patents remains in the field of kerogen, which is extensively leveraging the work done in 2008–2009 around low-temperature barriers for in situ processing of the immature hydrocarbon deposits of oil shale fields. Sample metalworking O&G patents produced between 2006 and 2015 that have received a large number of citations by other oil and gas patents are:

Patents most frequently cited in O&G patents

Metalworking in the knowledge network (2006)

Access the interactive graph for more details about the knowledge flow by year for each technology.

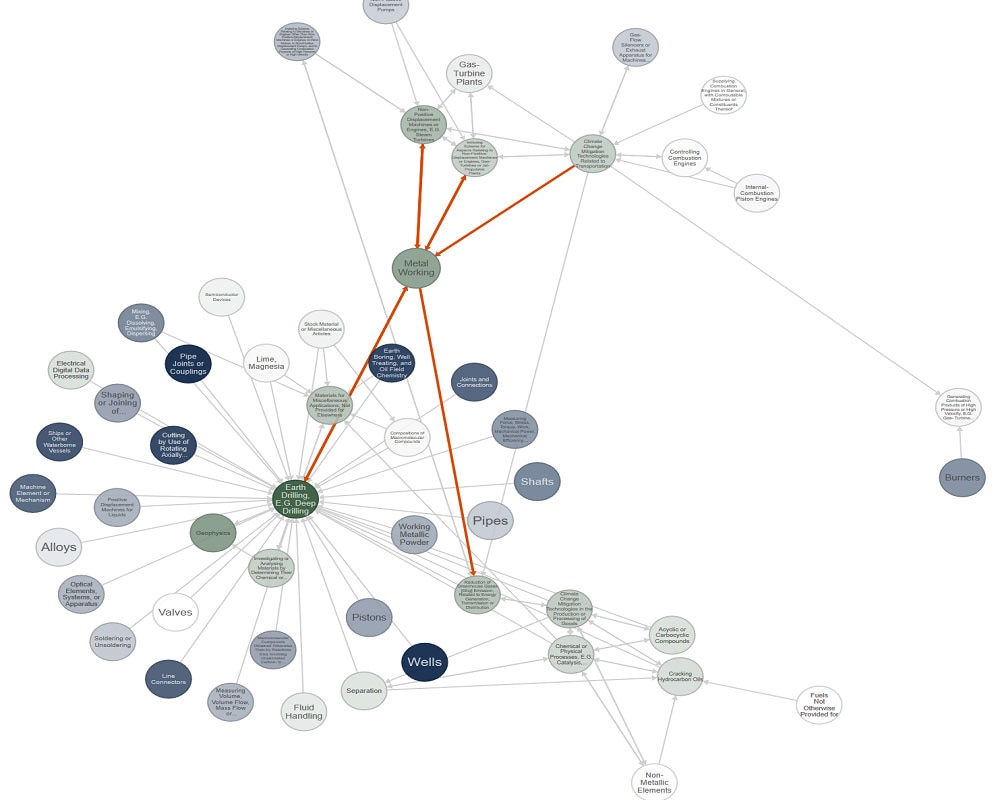

This important position for metalworking remained consistent in 2015 as it provided the link between earth drilling and other technologies including gas turbine plants, non-positive displacement machines, and non-positive displacement pumps.

Metalworking in the knowledge network (2015)

Access the interactive graph for more details about the knowledge flow by year for each technology.

Metalworking and other bridging technologies (like chemistry, shown in a smaller network in the bottom right of the above diagram) should not be regarded simply as sideshows in the growth of knowledge at oil and gas firms. They represent key strategic “bridges” of intellectual property that connect back to the singularly important task of earth drilling.2

Companies seeking flexibility in their development path should consider additional investment in these bridge technologies—which we refer to “technological pressure points”—as areas with the potential to have disproportionate impact. These changes in the shape of the O&G technology network indicate vibrancy and dynamism within the O&G patent universe.

Measuring innovation: The Energy Innovation Index

While noting historical trends in O&G patent filings, the question remains whether innovation is fundamentally changing how O&G relates to the broader non-O&G patent universe.

A unique way to measure the impact of innovation is to consider the extent to which oil and gas patents are being leveraged over time by non-O&G patents. Just as technologies combine in unique ways over time within the O&G patent universe, technologies developed by O&G companies are also cited outside of the O&G universe. Higher synergies between disparate technologies move them into stronger and more central locations within the broader patent universe.

Location in the knowledge network is important, because the more centrally located technologies have a greater chance of quickly incorporating innovations from neighboring technology areas. By way of contrast, technologies that are at the fringe of the knowledge network have fewer chances of bridging into totally new knowledge areas and creating genuinely disruptive innovations.

In the figure below, all patents from 2015 are used to form a map of human knowledge (as embodied by patents). Technologies are circles, and lines appear when technologies draw on each other. In the 2015 example shown below, semiconductor devices, which were among the fastest growing patent area in the oil and gas industry at the time (Growth and volume by technology), connect widely within the patent universe because of their cross-sectional applications across industries.

Semiconductor position in the patent universe (2015)

Access the interactive graph for more details about the knowledge flow by year for each technology.

In contrast, earth drilling, O&G’s highest volume area of patenting, appears on the knowledge map with some connections but not as deeply connected to as many other technologies. Also, some of the technologies it links to are not centrally located in their own right (such as oilfield technology, which only connects to two other technologies). This makes it less likely that the oil and gas industry’s current stock of granted earth drilling patents will result in advances based on bridging technologies from genuinely different fields of science.

Earth drilling position in the patent universe (2015)

Access the interactive graph for more details about the knowledge flow by year for each technology.

While the movement of individual O&G technologies is of interest, we can measure the drift in aggregate of innovation within the O&G industry as a whole by producing a weighted average across all technologies to produce what Deloitte refers to as the "Energy Innovation Index."3 Technologies with high O&G contributions and a commanding location in the patent network contribute positively towards the O&G aggregate score. When a core technology in the oil and gas industry drifts away from the center of the patent universe, or has a decreasing contribution from the O&G industry, it causes a decline in the Energy Innovation Index.

Higher values on the Energy Innovation Index reflect a trend toward highly connected technologies that, many times, might lie outside of the O&G industry’s traditional areas. Lower values on the Index indicate may be technology areas with a narrow focus within O&G, located toward the fringe of the overall knowledge network. As such, the Energy Innovation Index helps us understand whether the industry is trying to expand into highly connected technologies or is focusing on innovation from within.

When we compute the Energy Innovation Index it shows a slight decline over time. This means that the overall O&G industry seems to be moving toward the edge of the overall patent universe. This should not be interpreted as a slowdown in the pace of innovation within oil and gas, but rather that other industries have likely accelerated their intensity and interconnectedness of innovation faster over the past decade or so—a decade in which advances in IT and communications technologies have become pervasive. It also reflects the fact that many of the meaningful innovations in the oil and gas industry have come from combining existing O&G technologies rather than “moon shot” innovations combining more distant technologies.

Energy Innovation Index

What explains the move of O&G technologies toward more inner-focused innovation, and away from the center of the patent universe? One explanation might be the decline of patent network page rank (which measures how much a technology area gives and takes knowledge from areas outside of itself via patent citations) for two traditionally important O&G technologies: earth drilling and Chemistry: colloid chemistry.

Page rank over time

The concept that O&G innovation is looking increasingly inward might seem at odds with the success reported by O&G firms in many areas of operation through new and better technology. An explanation might be that oil and gas firms are succeeding by increasing innovation within focused technology areas like earth drilling—and not from more connected areas (like semiconductors). These new technologies may yield headlines and genuinely drive profits in the future but are not currently a major source of patent-protected innovation within O&G firms. Bottom line: firms that can buck this inward-looking trend and successfully adopt distant, patentable technologies have the chance of leapfrogging competition and experiencing greater upside.

No matter which way the industry leans, past evidence suggests that there will be substantial and meaningful innovation in oil and gas related to expanding relatively new technologies like hydraulic fracturing. In the next section, we examine the progress of innovation in hydraulic fracturing and its related technologies to provide a detailed, specific and impactful example of how innovation continues in a key technology underpinning a period of extraordinary success in developing and producing unconventional oil and gas, particularly in North America.

Part 2: Hydraulic fracturing: A case study in innovation

Studying growth: A look at patent filing trends

Hydraulic fracturing is a stimulation process in which water, chemicals, and proppants are injected at high pressure to fracture impermeable tight rock formations, leading to an increased flow of hydrocarbons to the wellbore. This technology, along with horizontal drilling and related technologies, has enabled the extraction of large oil and gas reserves trapped in shale and other source rock formations, leading to the shale revolution in the United States. “Shales” now account for over 40 percent of US crude oil and natural gas production, up from a mere two percent in 2001.

Patents related to hydraulic fracturing have gained prominence in the oil and natural gas industry throughout the past decade. O&G companies (primarily oilfield service majors, followed by equipment manufacturers, niche suppliers of proppants and compositions, supermajors, and a few large E&P independents) have filed nearly 1,000 hydraulic fracturing related patents since 2006, with the pace of filing increasing year over year. In 2015, for example, these companies filed over 150 patents, more than double the number in 2006.

The majority of the fracturing-related patents lie in the (a) earth drilling category (E21B43, patent classification code), followed by (b) drilling compositions and related aspects (C09K8, C09K2208) and (c) well treatment and oilfield chemistry (Y10S507,Y10T428). A deep dive into these three groups reveals where fracking-related innovation specifically is taking place, and helps determine if the industry’s technology focus has changed over the last few years.

Within the (a) earth drilling category of patents, our research shows that there are two dominant areas of fracking-related patenting activity:

(i) Tools and methods to create effective fractures (increasing penetration, isolating zones, seismic monitoring, well treating, etc.), and

(ii) Technologies and solutions that reinforce the already created fractures (different materials, shapes, and sizes of proppants; preventing flowback of particles, etc.).

About 40 percent of the hydraulic fracturing related patents we researched fell in one of these two areas of innovation. For example, the “Multi-stage fracture injection process for enhanced resource production from shales” patent, US8978764B2, filed by Maurice B. Dusseault and Roman Bilak, is an invention that generates “a network of fractures and induces it by injecting a plurality of slurries comprising a carrying fluid and sequentially larger-grained granular proppants in a series of injection episode.”

Hydraulic fracturing related patents

The second largest hydraulic fracturing-related group in terms of patents, seems to (b) drilling compositions and related aspects, has seen a boost in attention among O&G innovators, especially over the last few years. A large part of the innovation in this group is centered on fracture fluids composition containing organic compounds (fluid loss control agents, system stabilizers, viscosity reduction, etc.), composition of proppants and related fluids used to keep fractures open, and use of coated proppants to enhance conductivity. The ongoing learning and innovation in drilling fluid composition, along with new methods to create and reinforce fractures, are a major factor in explaining the rising productivity in shale plays [In the Eagle Ford play in Texas, for example, new well oil production per rig has increased from less than 40 barrels per day in 2007 to more than 1,400 barrels per day by early 2017].

Major patents categories

Notes:

1. The percentage of patents filed in various categories are not mutually exclusive, same patent can have multiple group tagging.

2. Smaller bubbles are for indicative purpose that there are several other patent groups that are not specified.

Source: Deloitte analysis

Within (c) well treatment and oilfield chemistry patents, the invention focus appears to have changed over the years and remains highly fragmented. From 2006 to 2009, much of the innovation within the group focused on reducing the viscosity of fracturing fluids by including new additives and particulates. However, since then, the focus appears to have shifted toward fluid treatment systems and increasing fracture complexity. This patent group, which primarily consists of cross-sectional technical subjects, is likely to gain prominence and draw inspiration from increasing innovation in other industries.

Inspiring innovation: Past patents show the way for future innovation

Prior patents often act as a source of innovation for future research. Specific to recent fracking patents, their source of innovation goes as far back as the 1860s and comes from both within and outside the O&G industry. An O&G patent, “Improvement in revolving ordnance,” published in 1862, and a non-O&G patent, “Improvement in rock-drills,” published in 1865, were among the first patents to inspire more recent breakthroughs in the hydraulic fracturing processes.

Deloitte’s research of the top five patent technologies suggests that the mid-1980s–2000 period was, and continues to remain, a “golden age” for shaping innovation in fracturing. Approximately 60 percent of the total citations by recently filed fracking-related patents belong to the 1985–2000 period, as indicated by the blue line in the graph.

Furthermore, each patent in the 1985–2000 period was cited up to 20 times by the recently filed patents (red line in the graph), highlighting the strength and impact of innovation patented during the years from 1985–2000.

Yearly citations by recent hydraulic fracturing patents

Source: Deloitte analysis

The prime source of innovation for all of the recent fracking-related patents is the earth drilling category (E21B43). In other words, earth drilling is not only the top area of O&G patent filing but also the top source of innovation for other fracking patents. Specifically within this group, E21B43/267, which consists of methods or apparatus for reinforcing fractures by propping, has been the most cited subgroup since the 1860s.

Within this propping sub-group, however, citation trends for recently filed hydraulic fracturing patents have changed from decade to decade. For instance, the majority of the innovations cited in this subgroup during 1981–1990 concerned developing sintered proppants with low density, high strength, and increased conductivity. Over the period from 1991–2000, innovation centered around new methods and/or techniques to prevent the flowback of proppants or other fine particles from the formation to the wellbore. During the 2000s, the trend shifted again, showing more patent filing citations involving the use of new materials, especially composites, as proppants.

Simply put, a solid history and timely evolution explain the large-scale commercialization and success of hydraulic fracturing technologies. The role of past innovations on future research may become more important as the industry targets new subsurface challenges to improve well productivity without compromising safety and environmental performance.

Branching out: Hydraulic fracturing looking outward for inspiration

The focus of research in the field of hydraulic fracturing continues to evolve, rapidly. With shale technology starting to mature toward full-scale commercialization, and the growing need to increase shale well productivity and improve recovery, the industry seems to have shifted its research focus over the past 12–18 months toward:

- Monitoring of proppants, fractures, and fracturing fluids by using advanced tracking tools and techniques like opticoanalytical devices, hybrid transponder systems, real-time seismic monitoring, and DNA sequencing, and by employing conductive proppants containing dispersed piezoelectric or magnetostrictive fillers.

- Treating flowback water/fluids through electrocoagulation, chemical co-precipitation, and even employing microwave separation technology (“MST”) and ultraviolet light remediation (“UVLR”) units. Some research is also underway on treating and mixing oil-based drilling fluids, fracking fluids, and produced waters with mature compost, organic fertilizer, hydrocarbon-digesting microbes, etc. so as to produce fertile topsoil.

- Controlling the viscosity and heat resistance of fracking fluids by using more and more nanoparticles. Over the past few years, research has increased on the usage of nanoparticles like cellulose nanowhiskers, nano-sized phyllosilicate minerals, nano-encapsulated fluids viscosity breakers, and thermoset-nanocomposite particles for improving heat and environment resistance.

- Enhancing field development plans through optimal positioning of horizontal laterals and drilling pads and even exploiting significant portions of a reservoir through a “horizontal well line-drive oil recovery” process. In this new in situ combustion process, adjacent horizontal wells are continually drilled in a direction along the reservoir and the penultimate lower production wells are converted into injection wells to drive hydrocarbons to an adjacent parallel production well for recovery to surface.

Summing up, hydraulic fracturing and related technologies have come a long way in sourcing and extending innovation from the parent O&G patent group of earth drilling and related aspects. More recent filings and ongoing research in the field of nanoparticles, monitoring and sensing, etc. suggest that hydraulic fracturing innovations are quickly building connections or borrowing from neighboring technologies outside the O&G industry, and will most probably be a source of inspiration for other industries, especially in the aspect of waste fluid management and treatment.

Looking forward: The future lies in building networks of innovation

Innovation in the oil and gas industry continues to center around traditional core applications such as earth drilling. However, the rapidly evolving networks and ongoing innovation in oil and gas are giving rise to several new bridging technologies that connect disparate technologies to the core. These connections are emerging both within O&G and outside O&G, and thus starting a new network of knowledge in the industry.

O&G companies contributing to and sourcing knowledge from these new networks of technologies could have an improved chance of leapfrogging their competition in a new world of energy where incremental innovation focused on improving an existing product's development efficiency and productivity may not be enough.

The networks and innovation indices presented in this paper could help companies track their standing and influence within their own specific innovation ecosystems. A deep dive into technology networks, and investigating the specifics and trails of newer technologies like hydraulic fracturing, could help companies identify new research themes and partners earlier, thus giving new direction to ongoing and future research pursuits.

How can we help you apply these findings to your business?

Get in touch

John England

Partner, Energy & Chemicals | Deloitte & Touche LLP

Contributors

Deloitte Research & Eminence team:

Vivek Bansal, senior analyst, Market Development, Deloitte Support Services India Pvt. Ltd.

Daniel Byler, manager, lead data scientist, Deloitte Services LP

Venkatesh Gangavarapu, analyst, Market Development, Deloitte Support Services India Pvt. Ltd.

Vamsi Krishna, senior analyst, data scientist, Deloitte Support Services India Pvt. Ltd.

Anshu Mittal, executive manager, Market Development, Deloitte Support Services India Pvt. Ltd.

Tiffany Schleeter, PhD, senior consultant, data scientist, Deloitte Services LP

Acknowledgements:

The authors would like to issue special thanks to the Deloitte Advanced Analytics and Modeling Data Center team and the following advisers and contributors whose insight and expertise were invaluable to the creation of this report:

Jim Guszcza, US chief data scientist, Deloitte Consulting LLP

Michael R. Petrillo, specialist leader, Deloitte Consulting LLP

Noah Lang, assistant general counsel, Deloitte LLP

Methodology

Access the Methodology report.

In our first patent publication, “Tracking innovation in oil and gas patents: The role and influence of the US Department of Energy,” we used US patent classification structure (USPC) to highlight and analyze the areas of innovation in the oil and gas industry. Recently, the US Patents and Trademark Office in a joint venture with the European Patent Office (EPO) agreed to harmonize their existing classification systems (European Classification (ECLA) and United States Patent Classification (USPC) respectively) and migrate toward a common classification scheme called The Cooperative Patent Classification (CPC). In this paper, we have used the new classification framework of CPC.

CPC uses the concepts of section, class, subclass, and group. The highest level is section; each section is subdivided into classes, which in turn are made up of one or more subclasses. Each subclass is broken down into main groups. Each part of this hierarchical structure is identified by classification symbols. For example, consider the following structure:

A01B33/00

“A” constitutes the section

“A01” is the class level

“A01B” represents the subclass level

“A01B33/00” is the group level

Considering that the filed patents, in both the new and existing structure, are not tagged by industries, the study used 42 unique oil and gas companies including the major oil and gas producing firms, oilfield services and drillers, downstream companies, and large equipment providers and automation companies serving O&G clients, as a representative set for patents filed in the oil and gas industry.

The study extracted hydraulic-fracturing related patents through a full text keyword search of 35 keywords on the universe of patents. The keywords such as “hydraulic fracturing,” “slickwater technologies,” etc., were derived after multiple refinements and relevancy checks, including the reading of abstracts and summaries of randomly selected patents. To better understand the evolution of fracturing-related technologies, the hydraulic fracturing analysis covers the group level classification of technologies (i.e., the last available leg in CPC classification) and cited patents since 1860s.

For additional information on our methodology, please see this detailed technical write-up which contains information on how the data was processed and scores were computed.

Endnotes

All of the research in this paper was done by the Deloitte Research & Eminence team that screened and analyzed millions of patents data, dating back to the 1860s, from a variety of sources, including: The US Patents and Trademark Office, Reed Tech, and Google Patents. Our work focused on utility patents. All calculations and analysis were done internally and are based on the new patent classification scheme, the Cooperative Patent Classification (CPC).

Notes:

1. Each patent has a bibliography of other patents. When a patent in one area (say earth drilling) cites another (such as geophysics), we infer that innovations in geophysics led to innovations in new earth drilling technology. In this way, prior patents are a resource to future patents. When enough patents demonstrate the same link between two technologies, we can infer that they are connected and meaningfully contribute to each other.

2. Within our study, In order to form a ‘link’ between two technologies, we set a threshold that 75 patents from one area had to cite another area. This was kept consistent across all years. As a result, part of the increasing complexity of charts from later years is that there were simply more patents. However, more patent activity can genuinely reflect greater levels of innovation, and so the benchmark of 75 was kept consistent.

3. In network theory, nodes and links are measured by several variables. The ratio of oil and gas patents within the universe is applied to one of these values (called page rank) and summed up to quantify the centrality of oil and gas patents to the network. This is the foundation of the Energy Innovation Index. It is computed annually across the entirety of the patent space. For more details on the calculation of the index, please see our computational methods paper.

References:

i. United States Environmental Protection Agency, “The Process of Hydraulic Fracturing,” https://www.epa.gov/hydraulicfracturing/process-hydraulic-fracturing, accessed February 14, 2017.

ii. EIA, Short-term Energy Outlook and Drilling Productivity Report, January 2017.

iii. D.R. Cahoy, “The Changing Face of US Patent Law and Its Impact on Business Strategy,” April 30, 2013.

iv. Dusseault, M. B., & Bilak, R. (2015). US Patent No. 8978764. Washington, DC: US Patent and Trademark Office.

v. EIA, Drilling Productivity Report, January 17, 2017. http://www.eia.gov/petroleum/drilling/pdf/dpr-full.pdf.

vi. Moulton Joel (1865), “Improvement in rock-drills,” US Patent No. US47850 A, Google Patents, http://www.google.co.in/patents/US47850; Moses F. Hardy (1862), “Improvement in Revolving Ordnance,” US Patent No. US36148A, https://patents.google.com/patent/US36148A/en?q=improvement&q=revolving&q=ordnance.

As used in this publication, “Deloitte” means Deloitte LLP and its subsidiaries. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

This publication contains general information only and Deloitte is not, by means of this publication, rendering business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

The Deloitte Center for Energy Solutions (the “Center”) provides a forum for innovation, thought leadership, groundbreaking research, and industry collaboration to help companies solve the most complex energy challenges.

Through the Center, Deloitte’s Energy & Resources group leads the debate on critical topics on the minds of executives–from the impact of legislative and regulatory policy, to operational efficiency, to sustainable and profitable growth. We provide comprehensive solutions through a global network of specialists and thought leaders.

With locations in Houston and Washington, DC, the Center offers interaction through seminars, roundtables, and other forms of engagement, where established and growing companies can come together to learn, discuss, and debate.

Recommendations

Creating an innovation index from patent data

Tiffany Schleeter explains the methodology behind this approach