The inflation outlook has been saved

Perspectives

The inflation outlook

Four scenarios for 2023-2025

New drivers of uncertainty emerged over the last year, including interest rates moving from nearly 0% to 5%. Here are four scenarios for how inflation might evolve in the next three years and actions your organization can take to be resilient in each.

Inflation continues to cloud the future economic outlook

In early 2023, unemployment is at a 50-year low, and the labor market remains tight even after a year of rising interest rates. Meanwhile, the war in Ukraine may further disrupt commodity markets and US–China trade tensions threaten the stability of global trade.

So, while the drivers of inflation and the contributors to economic uncertainty have changed over the last year, the need to understand these drivers, analyze their impact and prepare for a world of high uncertainty remains critical to the success of any future-focused enterprise. The question remains:

What can business leaders do to prepare their organizations to prosper no matter what the future of inflation holds?

In continued collaboration with Deloitte’s US and global economists, we have updated our inflation scenarios—stories about the future designed to spark insight and spot opportunity and risk—and extended our hypotheses through the end of 2025 to incorporate key changes to the economic environment.

Learn more about the futures of inflation

Critical uncertainties

Four critical uncertainties are likely to impact the future inflation in the United States:

- How will consumer spending habits evolve?

- What will be the Fed’s next steps be in response to the changing economic outlook?

- How will the labor market evolve?

- How long will supply chain disruptions last?

Recommended courses of action

Each of these scenarios creates unique opportunities and challenges requiring business leaders to act responsibly:

Soft landing

Prepare for growth by focusing on development of novel offerings and expansion into adjacent markets. Consider pricing strategy to prepare for new consumer expectations.

Optimize for: Growth, market share, and resiliency

Bumpy landing

Mitigate risks to input costs, especially those related to fuel and transport, by maneuvering away from sources that are directly impacted by the war in Ukraine. Shift talent strategy to increase employee loyalty and reduce attrition.

Optimize for: Stability and consolidation.

Hard landing

Prepare for decreased customer spending with focus on marketing and sales efforts. Maximize delivery and fulfillment capabilities through process improvements, automation, and AI. Consider finance options to capture opportunity of reduced interest rates.

Optimize for: Process efficiency, innovative sales, and marketing initiatives.

Implications and actions

Additionally, business leaders may consider taking the following “no-regret” moves, regardless of which scenario plays out:

- Develop robust cost analytics capabilities: Analyze major drivers of spending to understand trends, allocate funds toward strategic priorities, and reduce nonessential consumption.

- Optimize workforce delivery models: Revamp work performance models through automation, off- and near-shoring, and rationalization of roles.

- Build a strategic market sensing function: Develop internal capability to monitor how the future is evolving, especially with regard to evolving customer needs and pricing opportunities.

- Realign real estate strategy: Take advantage of expected changes in real estate prices and COVID-driven adaptations to support business objectives.

- Diversify supply chains: Minimize dependence on single countries or regions, to develop hedges that enhance resiliency in all conditions.

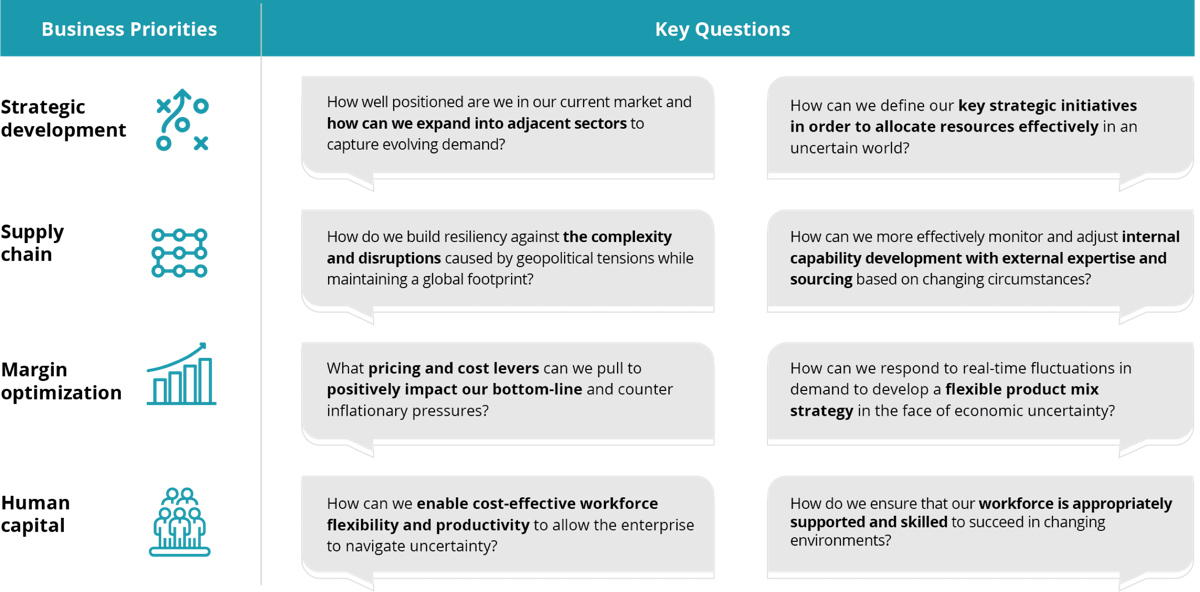

Key questions future-focused leaders should consider

While these scenarios address the data available as of April 2023, they do not exhaust all future possibilities. The interplay between evolving global conflict, the varied responses of governments around the world, the evolution of the public’s inflationary expectations, and the possibility of other, yet-unknown shocks, makes it impossible to declare with certainty the most likely inflationary outlook in 12, 18, or 24 months.

To prepare for future uncertainty, business leaders should consider asking the following questions:

Get in touch

Tom Schoenwaelder

Strategic Growth Transformation Leader

Recommendations

ERP strategy and digital finance

transformation

Getting the fundamentals right

ERP selection and vendor criteria for core financials

Choosing ERP software to drive sustainable long-term value