Implications of the revitalized Superfund tax for chemicals has been saved

Perspectives

Implications of the revitalized Superfund tax for chemicals

How to prepare now for 2022 excise tax changes

As part of the Infrastructure Investment and Jobs Act signed into law November 15, 2021, the Superfund Excise Taxes go into effect July 1, 2022. Here’s how to analyze the implications and plan now for the revitalized Superfund Excise Tax.

Revitalized Superfund Excise Tax

We provide an overview of the origins of the Superfund Excise Tax and take a closer look at the revitalized tax (effective July 1, 2022), as included within the Infrastructure Investment and Jobs Act (the “The Infrastructure Bill”), signed into law on November 15, 2021.1 Through this lens, we highlight issues to consider in evaluating the Superfund tax on chemicals and chemical substances.

History of the Superfund

The Comprehensive Environmental Response, Compensation, and Liability Act of 1980 (CERCLA) established the Hazardous Substance Response Trust Fund (the Superfund), which was to be administered by the Environmental Protection Agency (EPA).2 CERCLA imposed liability for the cleanup of hazardous waste sites on the owners and operators of these sites. When the owner or operator was not identified, or the site cleanups needed to be expedited, financing for the cleanup was to be provided by the Superfund.

The Superfund was to be financed through environmental excise taxes, including: (1) excise tax imposed on domestic crude oil; (2) excise tax imposed on imported crude oil and petroleum products; and (3) domestically produced and imported petrochemicals and inorganic chemicals. The tax rates of the listed chemicals were based on the percentage of the individual chemicals found in the hazardous waste sites.

During 1979 Senate discussions, it was estimated that expenditures for hazardous waste disposal sites related to chemicals would be $200 million (versus $40 million for sites related to crude oil).3 During this congressional hearing, it was determined that the proposed system of fees would cover: (1) crude oil; (2) petrochemical feedstocks; and (3) “certain highly toxic and/or high-volume inorganic materials including heavy metals, halogens, acids, bases, and ammonia.”4

The chemicals selected to be subject to the fee were based on two categories: petrochemical feedstocks and inorganic raw materials. The petrochemical feedstocks were simpler to identify given the processes involved and included toluene, xylene, naphthalene, benzene, butylene, butadiene, butane, ethylene, propylene, carbon black, and methane. However, the inorganic raw materials required a multi-tiered rubric:

(1) the material must be hazardous in a number of forms; (2) the material in some form must be hazardous if spilled; (3) the material must be produced in a large amount; and (4) the material must be capable of increasing the hazard potential of other elements.5

Congress intended for the fees to be imposed "at the beginning of the commercial chain of production, distribution, consumption, and disposal of hazardous substances." The rationale for the fee collection point was so that the fee would be equally distributed among all hazardous waste generators and suppliers.6

CERCLA (and therefore the Superfund Excise Taxes) expired in 1985 but was extended for another five-year period through the Superfund Amendments and Reauthorization Act of 1986 (SARA), effective January 1, 1987.7 SARA expanded the Superfund Excise Tax on chemicals to include an additional tax on imported substances derived from taxable chemicals, effective January 1, 1989.8 This additional tax on taxable substances was structured to ensure that the amount of the tax correlated to the composition of the chemicals within the taxable substances.9 In other words, had the substance been purchased domestically, the Superfund Excise Tax on chemicals would have been included as part of the overall price of the substance. Internal Revenue Code (IRC) section 4671 thereby imposed the same tax on imported substances as was already included in the cost of domestically purchased substances.

IRC section 4672 additionally directed importers and exporters to request a determination from the IRS as to whether a specific unlisted chemical substance should be included in the list of taxable substances. Specifically, the statute provides that to qualify as a taxable substance, taxable chemicals listed in IRC section 4662 must constitute more than “50 percent of the weight (or more than 50 percent of the value) of the materials used to produce such substance (determined on the basis of the predominant method of production).”10

Between 1990 and 1995, dozens of taxpayers petitioned the IRS to determine whether different chemical substances would qualify as “taxable substances,” primarily for purposes of export, so as to qualify for an exemption or refund. However, since the IRS ruled that these substances met the definition of taxable substance, these new substances were also subject to the tax if imported by taxpayers, thereby effectively increasing the list of taxable substances of IRC section 4672.

The Revenue Reconciliation Act of 1990 further extended the Superfund Excise Taxes through December 31, 1995, after which point the Superfund Excise Taxes expired.

Infrastructure Investment and Jobs Act

The Infrastructure Bill reinstated the Superfund Excise Taxes on chemicals and taxable substances, effective July 1, 2022.11 In addition to the reinstatement of the taxes, the Infrastructure Bill doubled the prior rate of tax on the 42 listed chemicals. This effectively doubled the tax rate of the imported taxable substances as well, and the Infrastructure Bill further increased the alternative method of calculation of the taxable substances to 10% the value of import. Congress directed the IRS to publish a list of additional taxable substances by January 1, 2022, which was published by the IRS via IRS Notice 2021-66.12

In addition to increasing the tax rate, the Infrastructure Bill lowered the threshold as to what is considered a taxable substance for importers or exporters who wish to request a determination from the IRS. Prior to the expiration of the Superfund Excise Taxes, a chemical substance that was composed of at least 50% of chemicals listed in IRC section 4662 could be found to be a taxable substance. The Infrastructure Bill lowered this threshold to 20%. Therefore, a chemical substance could qualify as a taxable substance if taxable chemicals listed in IRC section 4662 constitute more than “20 percent of the weight (or more than 20 percent of the value) of the materials used to produce such substance.”13

The Superfund Excise Taxes are currently set to expire on December 31, 2031, and are expected to generate $14.4 billion of revenue (or approximately $1.2 billion annually).14

Taxable chemicals

IRC section 4661(b) lists 42 chemicals, identified in Exhibit A. Each chemical has a specified rate of tax, imposed on a per-ton basis, as identified in Exhibit A. The Superfund Excise Tax is imposed on the manufacturer or importer of the listed chemicals, and the tax becomes due upon the first use or sale in the United States.15

Various exemptions exist for taxable chemicals, including:

- Methane or butane used as a fuel;

- Chemicals used in the production of fertilizer (including nitric acid, sulfuric acid, ammonia, or methane);

- Sulfuric acid produced as a by-product of air pollution control;

- Substances derived from coal;

- Substances used in the production of motor fuel, diesel fuel, aviation fuel, or jet fuel;

- Substances having transitory presence during the refining process;

- Separated isomer of xylene;

- Recycled chromium, cobalt, and nickel;

- Substances used in the production of animal feed; or

- Hydrocarbon streams containing mixtures of organic taxable chemicals.

Additionally, the export of taxable chemicals is eligible for a refund of any tax paid on the chemical.16

The IRS published proposed Treasury Regulations in 1983 specific to the taxable chemicals to further detail the methods of reporting the tax, as well as provide more detail on all the provisions concerning the tax.17

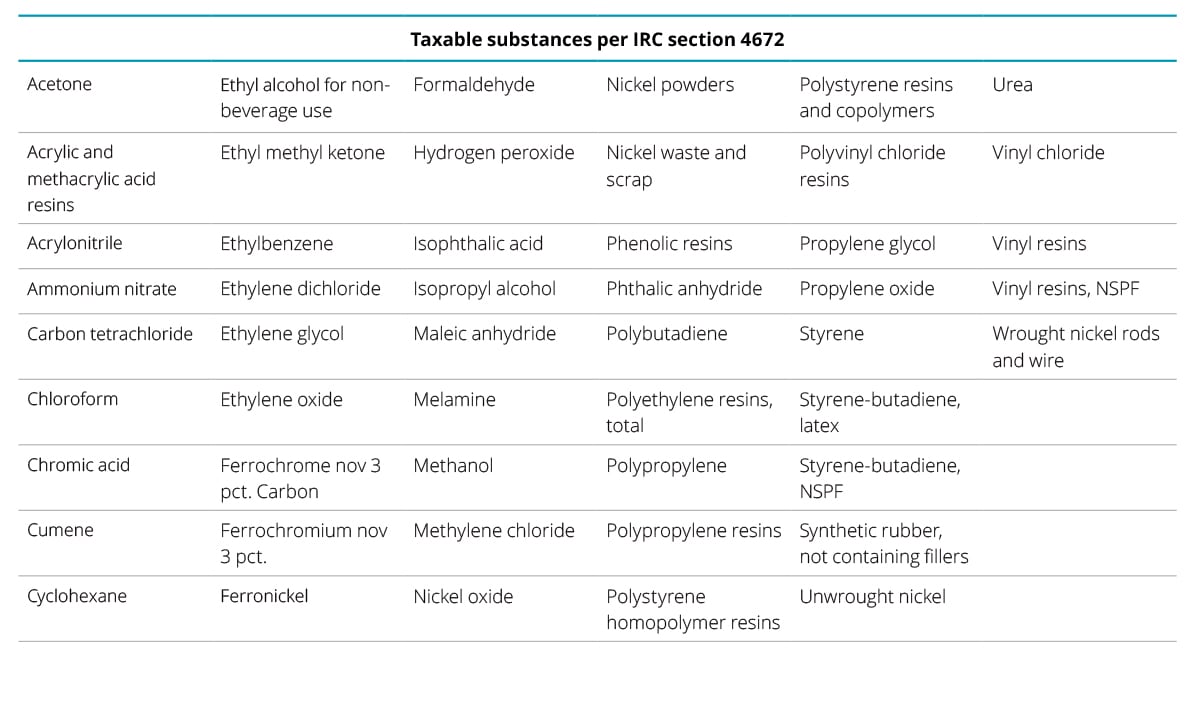

Exhibit A

Taxable substances

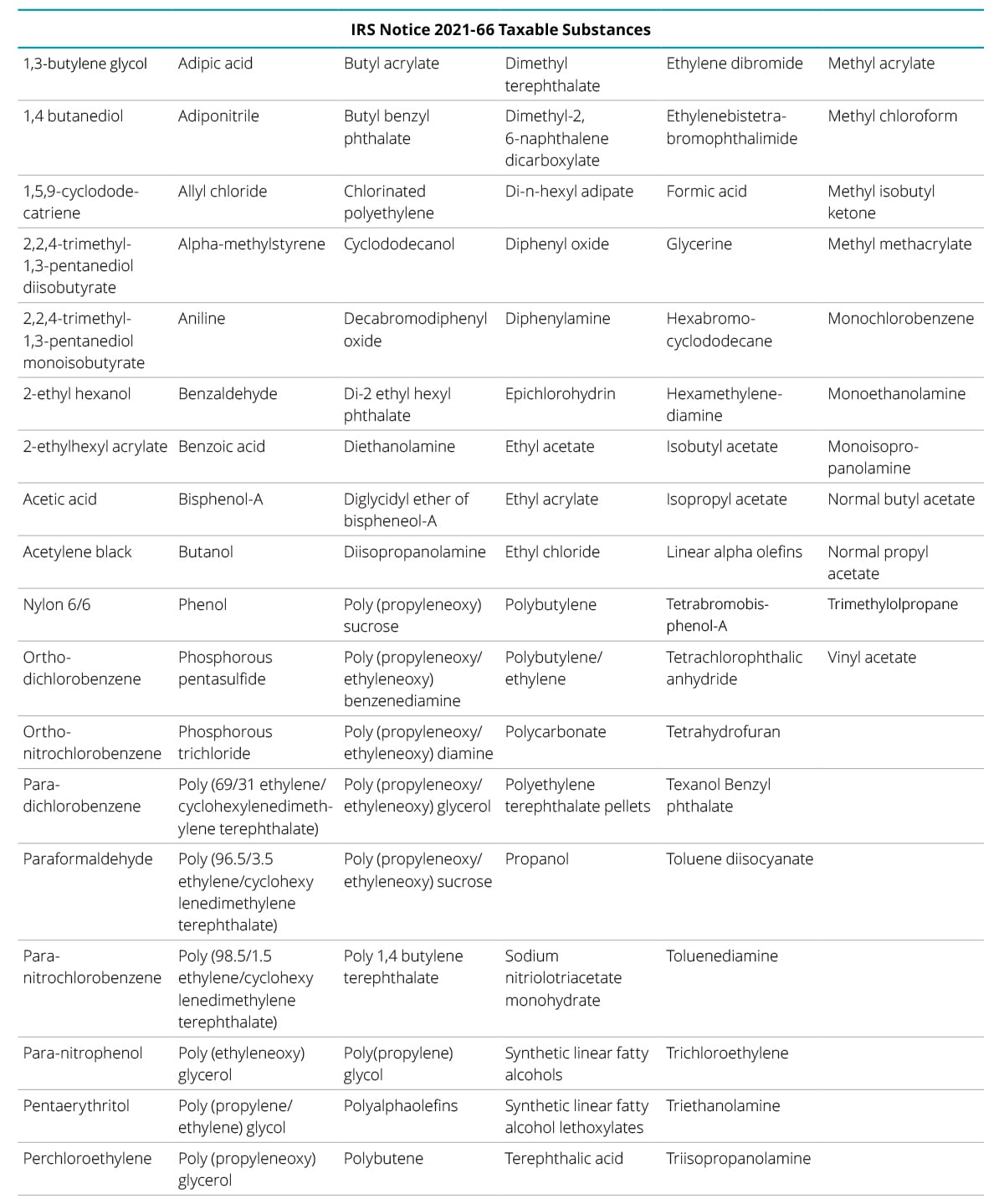

As discussed above, the list of taxable substances was incorporated into the IRC as a result of SARA, effective in 1989. The current list is published in IRC section 4672(a)(3) and attached as Exhibit B. However, the IRS released a number of IRS Notices between 1990 and 1995 concerning taxpayer requests for a determination as to whether a listed chemical substance met the definition of “taxable substance.” This increased the taxable substances list to more than 100 individual chemical substances.

Congress directed the Department of Treasury to publish an additional list of the taxable substances by January 1, 2022. The IRS published IRS Notice 2021-66 on December 13, 2021, which included the list of approximately 100 taxable substances previously considered by the IRS in the early 1990s via individual IRS Notices, which will now be subject to the Superfund Excise Taxes (see Exhibit C).18

The tax is imposed on the importer of the taxable substances and becomes due upon the first sale or use after import. The tax rate for taxable substances is dependent on the individual chemical composition of the substance.19 For example, if polypropylene is composed of 50% propylene (a listed taxable chemical), then the rate for polypropylene would be $9.74 x 50%, or $4.87. Alternatively, a taxpayer may base the rate for taxable substances on 10% of the value of the import.20

Additionally, similar to what happened between 1990 and 1995 when importers and exporters petitioned the IRS to determine whether various chemical substances would qualify as taxable substances, taxpayers may again request a written determination from the IRS as to whether a product they export or import qualifies as a taxable substance, if its chemical makeup includes at least 20% of a listed taxable chemical in IRC section 4661.21 However, IRS Notice 2021-66 suspended prior guidance (IRS Notice 89-61) as to how to request this determination, and taxpayers await additional guidance from the IRS as to the procedure to do so.

Exhibit B

Issues and considerations

There are several potential issues related to taxpayer liabilities, refund considerations, and other recordkeeping requirements to consider with regards to the Superfund Excise Taxes.

Chemical manufacturers and importers

The intent of the Superfund Excise Taxes is to target the chemicals primarily found in hazardous waste sites and to tax the chemicals at the earliest point possible in the process. Accordingly, the chemicals are taxed upon the first sale or use after import or manufacture in the United States, and the importer or manufacturer is liable for the excise tax, which it may pass along to its customers.22

Butane and methane users

The unique considerations of butane and methane require taxpayers further down the supply chain to be aware of the procedural issues affecting chemicals. While the majority of the 42 listed chemicals are taxable by the manufacturer or importer upon the first sale or use, butane and methane only become taxable upon the first use other than as a fuel.23 This creates a potential liability for downstream product sales such that the first company that uses the methane or butane in a manner other than as a fuel will have to report and remit the Superfund Excise Tax.

Importers

Companies that import taxable chemicals or taxable substances will be liable for the excise tax. Taxpayers may petition the IRS to determine whether a substance falls within the taxable substances list. The Infrastructure Bill lowers the threshold for a chemical substance to meet the definition of “taxable substance,” thus more imports may be subject to this tax.

Exporters

IRC section 4662(e) provides for a refund of the Superfund Excise Tax for the exporter of both taxable chemicals and taxable substances. Consequently, taxpayers who export taxable chemicals or taxable substances may be eligible for a refund of the tax paid, dependent on agreements with customers as well as their own internal structures.

Reporting

The Superfund Excise Taxes will be reported on a quarterly basis on IRS Form 720, Quarterly Federal Excise Tax. Additionally, Form 6627, Environmental Taxes, was previously used to report the Superfund Excise Taxes when the taxes were last in effect, and this form will be used again to report the taxes owed. Form 6627 must be filed alongside Form 720 on a quarterly basis.

Along with the quarterly reporting requirements, taxpayers with a quarterly liability greater than $2,500 will be required to make semi-monthly tax deposits of the Superfund Excise Taxes.

IRC section 4662 directs the IRS to release guidance as to the appropriate manner of reporting exempt sales or claiming refunds.

Technology/systems impacts

Companies responsible for collecting and remitting the excise tax will need to identify the source system to capture the transactional and master data for applicable transactions, and assess what data elements are captured and how to obtain necessary reports to support compliance filing.

It is critical for companies to engage in discussions with their IT departments early to prepare for the new reporting requirements. Due to the complicated nature of the Superfund Excise Tax and the granularity of the tax rate structure, gaps in existing systems and processes may exist. For instance, necessary data elements may not be available to properly identify the taxable chemicals and components. Effectively tracking necessary data through the supply chain may be a challenge as well.

Companies with a large volume of transactions should consider automating their tax calculation and reporting processes to increase efficiency and accuracy. To accomplish this, the current system capability should be assessed. This assessment should include a review of the transaction life cycle, master data setup, cost computation and recognition, and general entry posting.

The Superfund Excise Tax becomes effective on July 1, 2022. It is important for companies to engage in early conversations with procurement, contracting, IT, and other internal departments to identify and assess their exposure and potential gaps in data gathering.

It’s also important to understand the tax calculation and reporting requirements and to align with other business functions to implement a process to meet data, process, and system requirements. In our experience, it generally takes at least three months to fully implement and test a new business process and system implementation.

Exhibit C

How Deloitte can help

In addition to having deep tax technical knowledge surrounding federal excise taxes, Deloitte leverages leading technology tools and processes. Our services include:

- Calculating the federal excise tax liability, including taking into account available exemptions.

- Assisting with development and implementation of technology solutions to enable identification of taxable chemicals and substances, as well as exemptions.

- Assisting with risk analyses and internal processes (design or documentation).

- Analyzing and assisting in documenting available exemptions (e.g., certain taxable chemicals used in the production of fuel).

- Assisting with filing the federal excise tax returns and semi-monthly deposit reporting.

- Assisting with filing refund claims and reporting requirements around exemption certificates.

- Analyzing Superfund Excise Tax calculations and reporting requirements based on a company’s unique business scenario.

- Analyzing transactional and master data gaps given existing company system capability and data quality.

- Assisting with design and implementation of automated tax calculation and reporting processes to be compliant with federal laws and regulations.

Takeaways

The reinstatement of the Superfund Excise Taxes will impact companies throughout the country in a wide variety of industries. Taxpayers should be proactive and carefully analyze and consider the potential tax liabilities, tax reporting requirements, and systems impacts as a result.

Endnotes

1Investment and Jobs Act, Pub. L. No. 117-58 (2021).

2Comprehensive Environmental Response, Compensation, and Liability Act of 1980 (CERCLA), Pub. L. 96- 510, 42 U.S.C. §§ 9601-9675 (2021).

3S. Rep. No. 96-125 at 14878 (1979).

4Id. (“All oil and almost all hazardous substances are products of the oil industry, chemical and allied industries, and heavy metals industries. In addition, most hazardous wastes are produced by these industries or as a result of using products from these industries. All organic chemicals are derived from petrochemical feedstocks. Heavy metals, halogens, acids, and bases are significant raw materials for many toxic inorganics.”)

5Id.

6Id.

7Superfund Amendments and Reauthorization Act of 1986, Pub. L. 99-499, 42 U.S.C. §11001 (2021).

8Id. See also I.R.C. § 4671.

9See I.R.C. § 4671.

10I.R.C. § 4672(a)(2)(B)(1995).

11Infrastructure Investment and Jobs Act, Pub. L. 117-58.

12I.R.S. Notice 2021-66.

13I.R.C. § 4672(a)(2)(B)(2021).

14Joint Committee on Taxation, Estimated Revenue Effects of the Provisions in Division H of an Amendment in the Nature of a Substitute to H.R. 3684 (Aug. 2, 2021).

15I.R.C. § 4661.

16I.R.C. § 4662(e).

17Prop. Treas. Reg. §§ 52.4661-1 – 4662-4, 48 Fed. Reg. 48839 (Oct. 21, 1983).

18I.R.S. Notice 2021-66.

19I.R.C. § 4672(b)(1).

20I.R.C. § 4671(b)(2).

21See I.R.C. § 4671(b). Updated procedural guidance on how to request the determination has not yet been published by the IRS as of the date of this article.

22The IRS does not require that the tax be included in the total cost of the product or separately line itemed in an invoice.

23I.R.C. § 4662(b)(1).

Get in touch

SaraBeth Smith

Tax Senior Manager

Deloitte Tax

sarsmith@deloitte.com

Frank Falvo

Tax Managing Director

Deloittte Tax

ffalvo@deloitte.com

Marshal Sulayman

Tax Principal

Deloitte Tax

msulayman@deloitte.com

Stephane Lunan

Tax Partner

Deloitte Tax

slunan@deloitte.com

Christina Gong

Tax Senior Manager

Deloitte Tax

chrigong@deloitte.com