Internal audit innovation has been saved

Perspectives

Internal audit innovation

Applying Doblin’s Ten Types of Innovation®

The need for internal audit functions to do more has intensified in a disruptive and continually evolving business environment. Learn how Doblin’s Ten Types of Innovation framework can help internal audit adopt new methods and provide more value for their organizations.

Explore content

- A forward-looking approach

- What’s the problem?

- The four I’s of internal audit innovation

- Ten Types of Innovation®

- Setting a course

A forward-looking approach

Organizations are demanding more from internal audit. Senior executives, audit committees, and boards are expecting the function to take more forward-looking approaches to providing assurance, advisory, and risk anticipation services. At the same time, chief audit executives (CAEs) want to increase their functions’ impact and influence in the organization.

The need for internal audit to do more has intensified in a disruptive and continually evolving business environment. Evolution takes the form of innovation, with organizations constantly developing new methods, technologies, and structures to increase performance and deliver timely strategic insights and enhanced value.

If internal audit is to continue to evolve, it too must innovate to also meet the needs of the organization. The function must develop new approaches as businesses are created and divested, processes evolve, technologies are adopted, and regulatory demands fluctuate.

What’s the problem?

Traditionally, the need and expectation for innovation in internal audit hasn’t been particularly high. Now, however, internal audit groups and their stakeholders recognize that the function must evolve in order to meet the needs of the changing organization. A good number of audit committees, boards, and management teams now expect internal audit to anticipate key issues and decisions, risks, and be more forward-looking. Given internal audit’s historical role, innovation can be a challenging endeavor. However, the 4I’s of innovation provide a useful structure to follow when implementing innovation within Internal Audit.

The four I’s of internal audit innovation

Internal audit can benefit by developing a view of innovation that considers the activity in the context of the function and its role in the organization. This view, through a lens that we call the “four I’s of internal audit innovation,” links innovation to the work of internal audit and aligns internal audit innovation with the needs of the organization.

This view suggests that innovation in internal audit must be:

- Integrated

- Iterative

- Incremental

- Independent

When understood and embraced, the four I’s can help internal audit shift its view of innovation, identify useful initiatives, and scale its efforts appropriately.

Ten Types of Innovation®

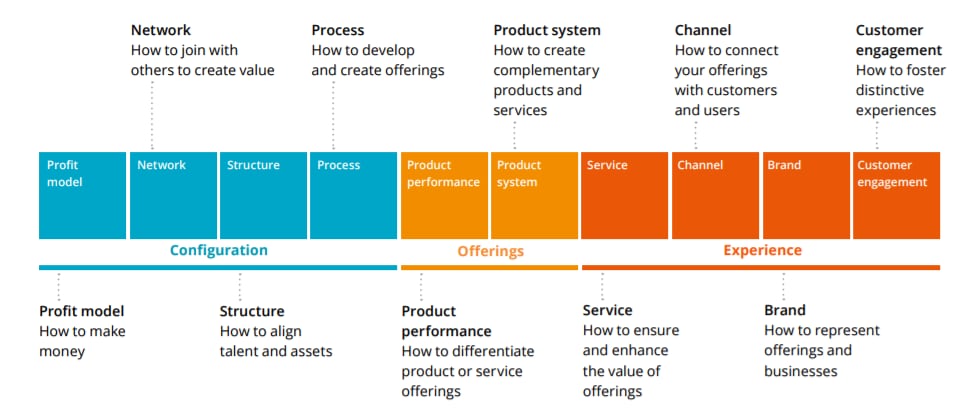

In helping companies identify and capitalize on new opportunities, Doblin has developed a flexible approach to innovation that’s applicable to internal audit—the Ten Types of Innovation framework. When selectively applied to internal audit, the framework is well-suited to the function’s need for integrated, iterative, incremental innovation, as opposed to radical change produced in isolation.

These aren’t steps, nor should they be viewed as such. Rather, they’re elements that can be combined and customized in various ways to generate new approaches, processes, and offerings for specific organizations in specific situations. It’s best to work with only a few elements—say three or four of the ten—to develop combinations that align available capabilities with the goal of fulfilling known user, customer, or (in the case of internal audit) stakeholder needs.

The Ten Types of Innovation lend order and structure to an endeavor—innovation—which strikes many internal auditors as non-traditional and risky. By configuring elements among the Ten Types to iteratively and incrementally alter its approach to internal audits, its service offerings, or the stakeholder experience, internal audit can harness new or existing capabilities to create new outcomes.

Learn more about the Ten Types of Innovation.

These aren't steps, nor should they be viewed as such. Rather, they're elements that can be combined and customized in various ways to generate new approaches, processes, and offerings for specific organizations in specific situations. It's best to work with only a few elements—say three or four of the 10—to develop combinations that align available capabilities with the goal of fulfilling known user, customer, or (in the case of internal audit) stakeholder needs.

The Ten Types of Innovation lend order and structure to an endeavor—innovation—which strikes many internal auditors as mysterious, disorderly, and risky. By configuring elements among the Ten Types to iteratively and incrementally alter its approach to internal audits, its service offerings, or the stakeholder experience, internal audit can harness new or existing capabilities to create new outcomes.

These aren't steps, nor should they be viewed as such. Rather, they're elements that can be combined and customized in various ways to generate new approaches, processes, and offerings for specific organizations in specific situations. It's best to work with only a few elements—say three or four of the 10—to develop combinations that align available capabilities with the goal of fulfilling known user, customer, or (in the case of internal audit) stakeholder needs.

The Ten Types of Innovation lend order and structure to an endeavor—innovation—which strikes many internal auditors as mysterious, disorderly, and risky. By configuring elements among the Ten Types to iteratively and incrementally alter its approach to internal audits, its service offerings, or the stakeholder experience, internal audit can harness new or existing capabilities to create new outcomes.

Setting a course

These four steps can help you get started:

- Identify the most significant wants, needs, or expectations that internal audit stakeholders have expressed. If they haven’t expressed any, issue a quick survey of stakeholders or simply ask them

- Consider the Ten Types of Innovation framework and how you might select a combination that would work to help you identify a specific innovation to get started on

- Develop and then share a picture of how integrated, iterative, incremental, and independent innovation might look in your internal audit function

- Identify the resources requirement to begin working on that initiative or to structure a more comprehensive response to the need for new approaches in your internal audit function

To learn more about taking an innovative approach to internal audit, download the full report.

Recommendations

Becoming Agile: Elevating internal audit performance and value

Innovating in internal audit to enhance collaboration and deliver timely insights

Detonate

Why—and how—corporations must blow up best practices (and bring a beginner’s mind) to survive