Accounting for GHG emissions has been saved

Perspectives

Accounting for GHG emissions

On the Radar: Greenhouse gas protocol reporting considerations

Explore our new roadmap publication to understand key issues in GHG emissions accounting and reporting under the GHG Protocol. Get guidance on how to classify GHG emissions into scopes 1, 2, and 3; define your company’s organizational boundary; and set GHG emissions targets as the landscape evolves.

On the Radar series

High-level summaries of emerging issues and trends related to the accounting and financial reporting topics addressed in our Roadmap series, bringing the latest developments into focus.

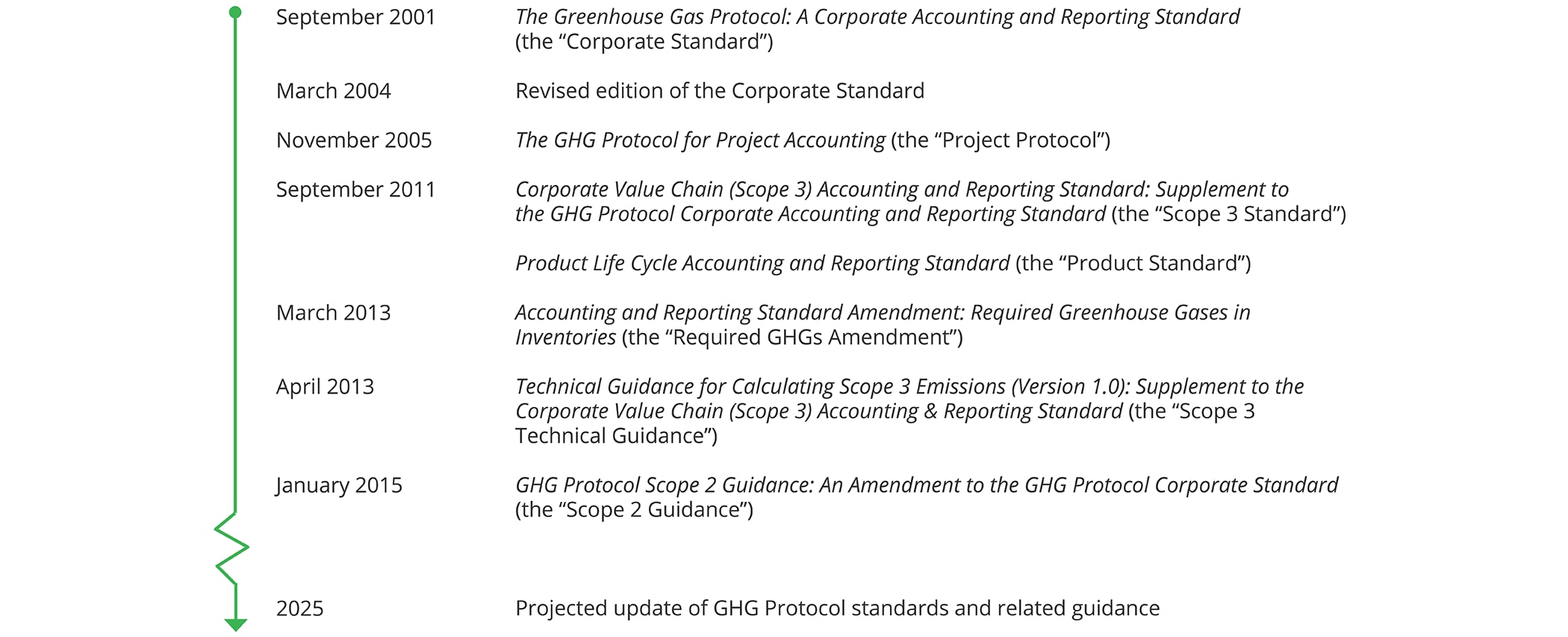

The Greenhouse Gas (GHG) Protocol is a set of standards and related guidance on accounting for and reporting GHG emissions. Its ongoing development, which has spanned more than two decades, represents the work of a multistakeholder partnership (the “GHG Protocol organization”) consisting of businesses, nongovernmental organizations (NGOs), governments, and other entities convened by the World Resources Institute (WRI), a US-based environmental NGO, and the World Business Council for Sustainable Development (WBCSD), a Geneva-based coalition of nearly 200 international companies. The timeline below illustrates the issuance dates of key GHG Protocol standards and related guidance.

On the Radar: Greenhouse Gas Protocol reporting considerations

The GHG Protocol provides a framework for companies and other types of organizations preparing a GHG emissions inventory. Specifically, it addresses the accounting for and reporting of seven GHGs: carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs), sulfur hexafluoride (SF6), and nitrogen trifluoride (NF3).

The current GHG emissions reporting landscape is evolving. The number of companies that are reporting on GHG emissions is increasing and will continue to rise as a result of new climate and sustainability standards and regulations across the globe.

While the new climate and sustainability standards and regulations are driving change in the reporting landscape, it is also important to recognize the business value of monitoring a company’s GHG emissions. Such monitoring may allow companies to identify business and financial risks that arise from their operations and provide management with insight into how to effectively manage those risks. In addition, it may help companies identify opportunities for transformation and growth so that they can differentiate themselves in the market.

Companies within the scope of the European Union’s Corporate Sustainability Reporting Directive (CSRD) are required to report on GHG emissions in accordance with the European Sustainability Reporting Standards or equivalent standards to be determined. The reporting timeline for CSRD varies depending on the structure of the company; however, the earliest reporting requirement begins in 2025. For more information about the CSRD, see Deloitte’s January 9, 2023 and August 17, 2023 Heads Up newsletters.

Various companies will need to comply with the International Sustainability Standards Board’s recently issued IFRS S1 and IFRS S2 which require disclosures such as information about GHG emissions and sustainability- and climate-related opportunities and risks, subject to jurisdictional adoption. IFRS S2 specifically requires reporting of GHG emissions in accordance with the GHG Protocol. IFRS S1 and IFRS S2 are effective for annual reporting periods beginning on or after January 1, 2024, subject to individual jurisdictional mandates. For more information about IFRS S1 and IFRS S2, see Deloitte’s June 30, 2023, Heads Up.

In the United States, the SEC issued a proposed rule on March 21, 2022, to enhance and standardize the climate-related disclosures provided by public companies. Under the proposed rule, companies would be required to report GHG emissions in a manner similar to that prescribed by the GHG Protocol. For more information about the proposed rule, see Deloitte’s March 21, 2022 (updated March 29, 2022), and March 29, 2022, Heads Up newsletters.

Whereas the SEC’s proposed rule would only apply to public companies, three bills recently signed into law in California—SB-253, SB-261, and AB-1305 the first climate-related bills to be passed in the United States—will require both public and private US companies doing business in California to provide certain climate-related and GHG emissions disclosures. The California Air Resources Board must adopt regulations to codify the requirements in SB-253 by January 1, 2025, and to codify the requirements in SB-261 by January 1, 2026. The effective date of AB-1305 is January 1, 2024. For more information about SB-253, SB-261, and AB-1305, see Deloitte’s October 10, 2023 (Updated December 19, 2023), Heads up.

Under the GHG Protocol, GHG emissions are classified into three scopes as follows:

Figure 1 of the Scope 3 Technical Guidance, which is reproduced below, illustrates a reporting company’s value chain and the classification of GHG emissions into scope 1, scope 2, and the 15 categories of scope 3.

The organizational boundary provides the basis for identifying emission sources from assets owned or controlled by the reporting company. For this reason, it is critically important to correctly identify the organizational boundary.

Applicable climate and sustainability standards and regulations, such as the SEC’s proposed rule on climate-related disclosures, may prescribe organizational boundaries that differ from those delineated in the GHG Protocol. Therefore, if a company is reporting on emissions in accordance with a specific standard or regulation, it should carefully consider the organizational boundary requirements of that standard or regulation.

If a company is reporting on emissions in accordance with the GHG Protocol rather than a specific standard or regulation, it may choose one of three approaches to identify its organizational boundary. However, once the company selects an approach, it must apply that approach consistently across the organization. The three approaches are outlined below.

A company may need to use judgment to identify subsidiaries, investments, and assets within its organizational boundary. Once a company identifies its organizational boundary, it will be required to identify the activities and sources of emissions, including how emissions are categorized (i.e., scope 1, scope 2, or scope 3)—also known as an operational boundary.

The GHG Protocol standards and related guidance provide latitude in application and related judgments, which has led to diversity in practice in how companies report GHG emissions. The WRI and WBCSD are currently evaluating this diversity through their transformation process, which is discussed below. Companies are encouraged to consult with their advisers on the application of the GHG Protocol to ensure that their accounting and reporting treatment is appropriate.

The GHG Protocol was initially developed over two decades ago to achieve multiple objectives, one of which, as stated in the Corporate Standard, is “[t]o provide business with information that can be used to build an effective strategy to manage and reduce GHG emissions.” Since that time, the regulatory landscape has evolved to reflect the capital markets’ heightened demand for disclosures about companies’ GHG emissions, resulting in an increased focus on transparency, consistency, and standardization. Such evolution has shifted how the GHG Protocol is being applied by companies to suit their purposes.

As business models evolve and transform, some companies may find that the current guidance in the GHG Protocol on accounting for emissions does not clearly address their circumstances. For example, since the GHG Protocol was developed before the introduction of circular business models (i.e., reduce and reuse), companies operating under such models must use greater judgment to apply the guidance. In such instances, companies are encouraged to provide clear and robust disclosures to ensure that users of their GHG emissions reports can understand the judgments, inputs, and assumptions on which their GHG emission calculations are based.

As companies evolve, investors shift their focus, and the economy transforms, companies are starting to set GHG emissions targets. These targets are widely focused on reducing scope 1 and scope 2 emissions.

Companies often cite their ability to more easily control scope 1 and scope 2 emissions as the primary reason for focusing GHG emissions targets solely on scopes 1 and 2. Management uses these GHG emissions targets in transforming their businesses but are also increasingly linking them to compensation and bonuses. Lenders are also using GHG emissions targets in debt covenant agreements and financing arrangements.

Companies may use renewable energy credits to offset their scope 2 emissions. Given the prevalence of renewable energy credits in the marketplace, companies may have the opportunity to completely offset their reported scope 2 emissions and meet GHG emissions targets even though they may still generate a significant amount of scope 2 emissions.

The heightened focus in the marketplace on GHG emissions and the increasing linkage of GHG emissions targets to compensation and bonuses make it important for companies to measure their GHG emissions accurately. Management and the board of directors may want to consider focusing on the GHG emissions targets set by the company and the targets’ potential impact on the company’s financial or operational metrics or other risks within the company. Specifically, they may want to ask themselves the following questions:

The WRI and WBCSD have undertaken a process to gather feedback from stakeholders to refine, amend, and provide enhancements to the GHG Protocol standards and related guidance. Feedback was gathered in the first quarter of 2023, and revisions to the standards and guidance are expected to be issued in early 2025.

The WRI and WBCSD have released a webcast recording discussing their findings on scopes 1 and 3, as well as a summary of findings on scope 2. Key themes and points raised by stakeholders are summarized in the figure below.

On the basis of the feedback provided to the WRI and WBCSD, a significant number of revisions to the GHG Protocol may lie ahead. Companies are encouraged to carefully monitor the activities of the WRI and WBCSD to stay informed of any developments related to implementation guidance and revisions.

Learn more about calculating for GHG emissions

Deloitte’s Roadmap Greenhouse Gas Protocol Reporting Considerations discusses how companies account for and report GHG emissions under the GHG Protocol.

Subscribe to the Deloitte Roadmap Series

The Roadmap series provides comprehensive, easy-to-understand guides on applying FASB and SEC accounting and financial reporting requirements.

Explore the Roadmap library in the Deloitte Accounting Research Tool (DART), and subscribe to receive new publications via email.

Let's talk!

Learn more about this topic

Get in touch for service offerings

Jamie Davis

Partner – Audit & Assurance | Deloitte & Touche LLP

Recommendations

How does your company’s ESG readiness measure up?

Take Deloitte’s ESG SelfAssess™

Sustainability regulation: A catalyst for transformation

ESG regulations are driving business opportunity and risk