Select the right lease accounting vendors and technology has been saved

Perspectives

Select the right lease accounting vendors and technology

Gearing up to meet ASC 842 requirements

For public companies, the new lease accounting standard ASC 842 goes into effect starting January 1, 2019. Achieving compliance within a tight time frame could be challenging, and it may require major changes to systems and processes. Find out how to choose the right approach and gear up to meet the new requirements.

Explore content

- Accounting for the challenges ahead

- Choosing the right lease accounting approach

- Which lease accounting platform and vendor are right for you?

- Short on time? Choose an interim solution

- Take action now.

Accounting for the challenges ahead

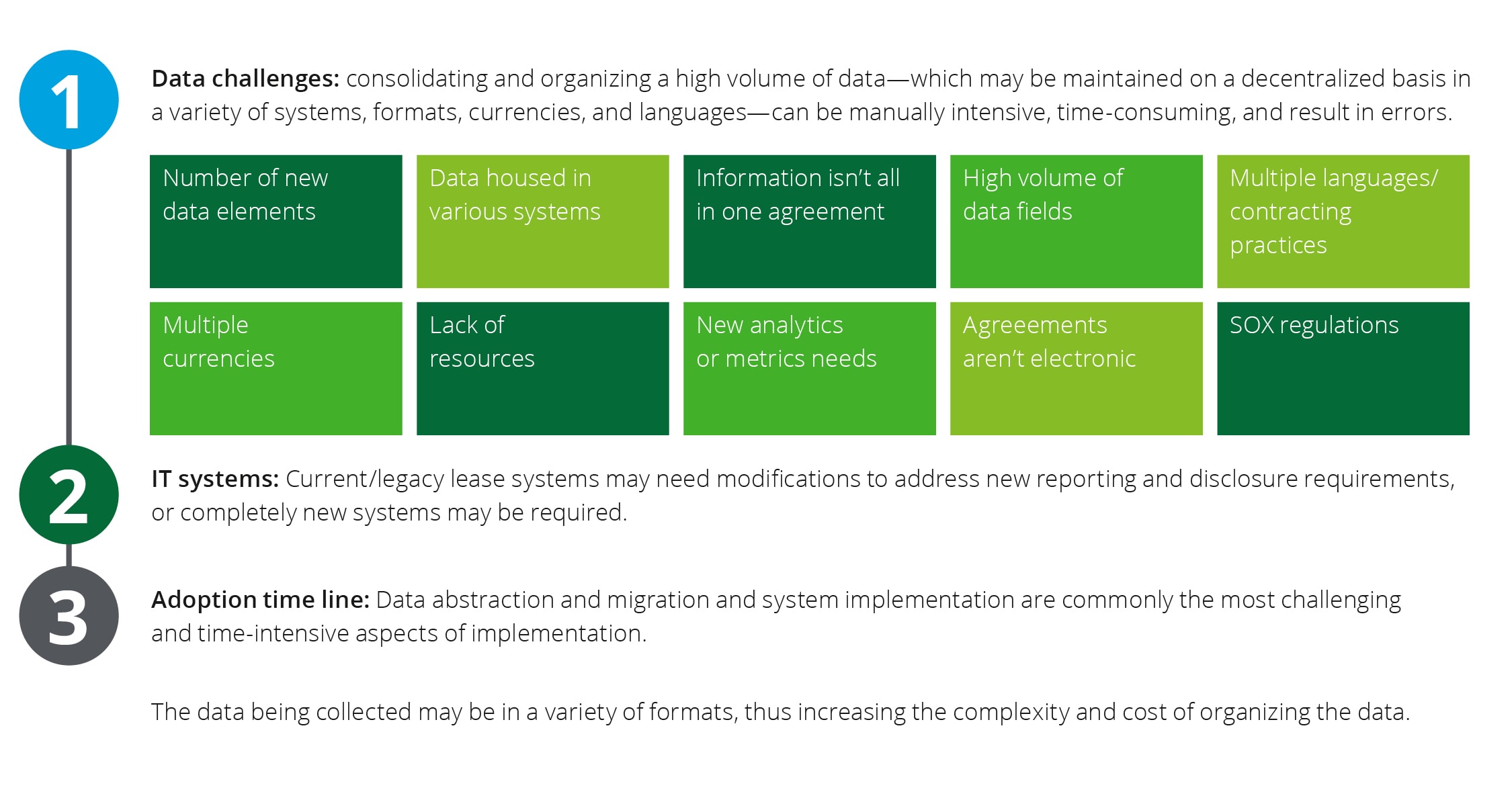

The new lease accounting standard could provide investors and other stakeholders with a more transparent view of a company's financial position. But for many, achieving compliance will be no easy feat. For starters, companies will likely need to revise their internal controls and related business processes for capturing, calculating, and accounting for lease agreements. In fact, depending on the nature and complexity of a lease agreement, up to 100 data elements may need to be captured (some of which aren't contained within the lease contract).

Many companies don't currently have systems or technology solutions to effectively manage lease agreements. Even among those that do, however, leases often aren't administered centrally. And in many cases, lease contracts exist only in hard copy—in multiple languages, locations, and currencies. This makes it difficult to ensure that all agreements have been identified and to extract the information necessary for the accounting and reporting requirements under the new standard.

In an accounting and financial reporting symposium that Deloitte hosted at the end of 2017, we asked participants about their challenges in implementing the new lease accounting standard. Of the 282 attendees, more than half responded that collecting data on organization leases in a centralized inventory was their biggest challenge.

Choosing the right lease accounting approach

Deciding how to comply with the new standard means making the right decisions for your company. And those decisions will likely have a significant impact on other key decisions, including vendor selection and process redesign. Here are some key considerations:

- Lease accounting or lease administration? The real question is should you limit the scope of the technology solution to lease accounting or to pursue a solution that covers the broader scope of lease administration. The latter option can offer more benefits and enhancement opportunities. But it likely will require more time, effort, and investment.

- Centralized or decentralized? A decentralized approach is typically more flexible and responsive to local needs, but it tends to be less efficient and consistent. It may also require more time and effort to implement, due to the increased challenges of coordinating and driving multiple initiatives across organizational and geographic boundaries.

- In-house or outsourced? A third strategic question to consider is whether to handle lease accounting and related activities in-house or to outsource some (or many) to a third party. Outsourcing can allow a company to capitalize on a vendor's deep experience and economies of scale. Insourcing provides more direct, hands-on control, but it requires dedicated resources as well as technical and lease accounting experience.

Which lease accounting platform and vendor are right for you?

Should you use a cloud-based platform (e.g., Software-as-a-Service) or build and maintain an on-premise solution? One potential advantage of the cloud is that software updates tend to be more timely and efficient, making it easier for a company to stay compliant. Some platforms are broader and more capable than others, so it's important to choose wisely. And don't ignore fundamental vendor-selection criteria, such as:

- Financial and technical resources. Does the vendor have sufficient financial and technical resources to keep its platform and features up to date and viable?

- Testing and certification. Has the platform been tested and certified? The requirements of the new lease standard are detailed and highly complex, so it's important to know that the underlying accounting rules are being applied correctly.

- Total cost. What will be the platform cost to implement and operate on an ongoing basis? To make a more informed decision, all expected costs should be considered, including first-year implementation expenses, annual licenses, and maintenance fees.

If a vendor is gaining popularity in your industry, it may be a sign that its platform is a good fit. But that doesn't replace the need to conduct your own careful selection process. Trends come and go, but nothing should matter more than how well a platform fits a company's unique needs.

Short on time? Choose an interim solution

Companies may benefit most from a comprehensive, fully integrated platform for lease accounting (or lease administration, which is even broader). But depending on the complexity of a company's needs—and the stage of the decision process—there might not be enough time to fully implement such a platform before the new lease accounting standard adoption deadline. Therefore, some companies may need to implement a temporary technology solution that can promptly satisfy the new standard's minimum reporting requirements by layering on top of existing systems and processes.

Take action now. Start achieving compliance with the new lease accounting standards

The deadline is approaching. For public companies, the new standard goes into effect for the calendar year starting January 1, 2019. But the required systems and processes should be up and running well before that date to allow sufficient time for testing, training, and debugging.

Any company that's not already well down the path to implementation should consider promptly developing a clear strategy and timeline for achieving compliance—and then aggressively

The clock is ticking. It's time to get in gear.

Get in touch