Carbon Capture, utilization, and storage hubs has been saved

Perspectives

Carbon Capture, utilization, and storage hubs

A necessity to achieve emissions goals in hard-to-abate sectors

Carbon capture, utilization, and storage (CCUS) technology is an essential tool in the fight against climate change. Explore the differences between its two forms—direct air capture and point capture—and read the cost and business implications from detailed quantitative modeling and analysis of industrial point sources in the state of Louisiana.

The two types of carbon capture and storage technology

Carbon capture, utilization, and storage (CCUS) is a process aimed at reducing greenhouse gas (GHG) emissions to curb global warming. It involves capturing carbon dioxide (CO2) emissions from sources such as the atmosphere, power plants, and industrial processes—utilizing the captured CO2 for beneficial purposes or storing the remainder underground in stable geological formations.

Today most carbon capture and storage technology is deployed against so-called point sources of CO2*, such as natural gas processing and industrial facilities. Another form of carbon capture, known as direct air capture, aims to remove CO2 directly from the atmosphere. Point capture is a relatively mature CCUS technology. Though not yet very widely deployed—around 40 commercial facilities are operating—hundreds of CCUS projects are in various stages of development.1 Direct air capture is a newer CCUS technology and currently much more costly per ton of CO2. It has recently received increased investment from private and public sectors.2

CCUS is gaining attention because it is considered one of the key strategies to achieve global climate goals by reducing atmospheric CO2 levels. The Intergovernmental Panel on Climate Change (IPCC) foresees a critical role for carbon capture and storage technology in getting to net-zero emissions and for carbon utilization in the production of critical materials.3 The International Energy Association (IEA) projects that around 1.2 Gt CO2 of CCUS per year will be required to reach net-zero emissions by 2050, up from less than 45 Mt CO2 per year today.4

Carbon capture and storage hubs: A necessity to achieve emissions goals in hard-to-abate sectors

The debate around CCUS technology

Like many topics related to climate change, CCUS is not without controversy. One critique is that implementation of CCUS technology will prolong the use of fossil fuels and that—to date—most captured CO2 is used in enhanced oil recovery (EOR). Putting aside any potential future use of CO2 for EOR, the fact remains that economically essential activities, including the production of hydrogen, chemical building blocks and intermediates, concrete, and steel, are expected to continue to generate CO2 emissions for the foreseeable future—necessitating carbon capture and storage technology in some form.

The chemical sector is highly illustrative of this point, as its products are crucial for building a sustainable global economy. The chemical and materials industry currently accounts for about 5% of global gross domestic product (GDP), and over 96% of all manufactured goods are directly touched by the chemistry business.5 The industry provides critical materials to other major industries, such as health care, transportation, communications, and retail. Even as the world faces the challenge of reducing GHG emissions to “decarbonize,” it is not desirable to “dematerialize” but rather to use materials most efficiently to sustain and advance the human condition.6 This is why the IPCC states: “It is important to close the use loops for carbon and carbon dioxide through increased circularity.”7

And while there is consensus among climate modelers on the general need for point source carbon capture, the agreement breaks down when it comes to specific use cases. Industrial processes where there is no alternative technology—a classic example is cement manufacturing—are widely accepted, even by opponents of CCUS technology. More debated are use cases where there would be alternatives to CCUS. An example would be blue hydrogen. Opponents argue there is an alternative green hydrogen and that all investments should flow to electrolysis routes to hydrogen rather than steam methane reforming (SMR)—the most common production route to hydrogen in the United States and globally—plus CCUS. Another example would be the production of key chemical building blocks, such as ethylene, which require temperatures above 800°C that are achieved only in combustion furnaces. In principle, there are alternatives such as bio-based ethanol dehydration and early-stage efforts in cracker electrification.8 And while these arguments are may be true, they neglect the low-technology readiness (cracker electrification), current costs (electrolysis hydrogen) of alternatives, long capital planning cycle of industrial investments and, particularly, the urgency to lower the emissions curve of heavy industry sooner rather than later. One does not have the luxury of time to wait for perfect solutions when the world has not even achieved peak GHG emissions.

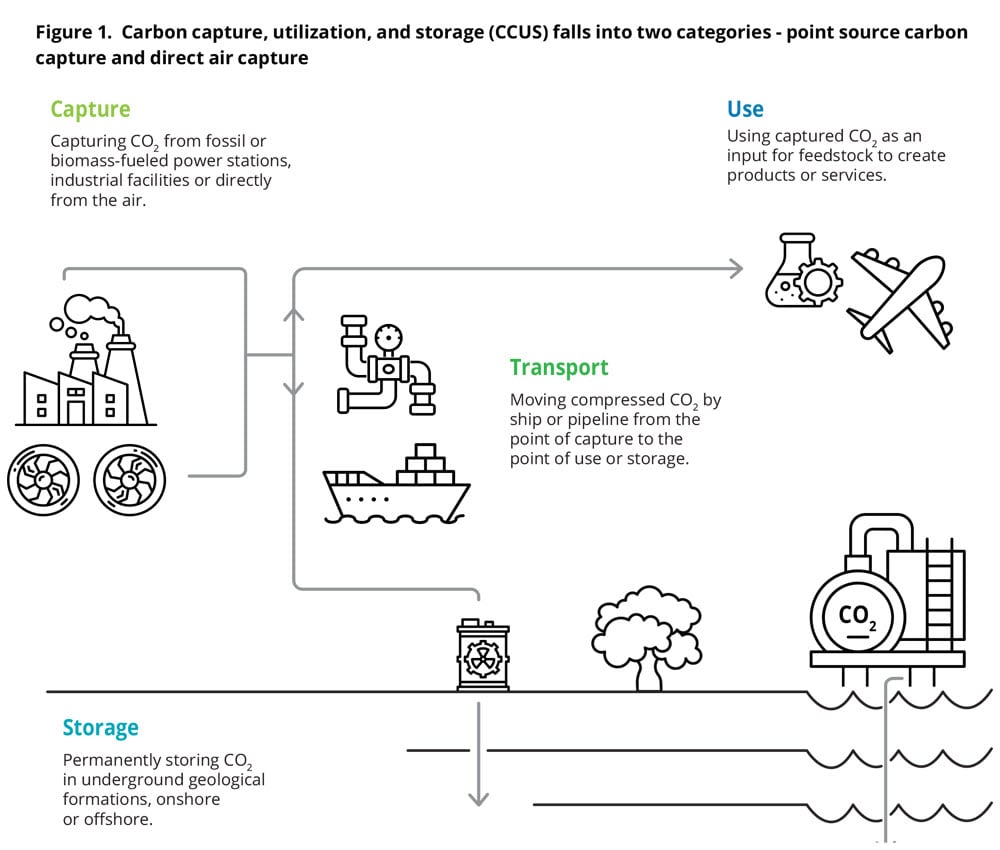

Overview of CCUS technology and CO₂ sources

The technology and use cases for gaseous CCUS fall broadly into two categories: point source carbon capture and direct air capture. These differ significantly in cost, technology, and application space.

Source: IEA

* Industrial CO2 sources, in reality, constitute multiple individual sources in a facility, but are treated as point sources for this discussion because they are fairly concentrated in comparison to direct air capture, in which the CO2 is captured from the vast atmosphere.

Learn more about the potential, practicalities, and costs of carbon capture and storage technology. Download the full report “Carbon capture and storage hubs: A necessity to achieve emissions goals in hard-to-abate sectors” for a detailed look across three major sectors and explore The Andlinger Center modeling study for early insights into a prototypical CCUS hub.

Endnotes

1 Sara Bundis, Mathilde Fajardy, and Carl Greenfield, “Carbon caption, utilization and storage,” International Energy Agency (IEA), last updated July 11, 2023.

2 See, for example, Ella Nilsen, “Biden administration to invest $1.2 billion in projects to suck carbon out of the air,” CNN, August 11, 2023.

3 Intergovernmental Panel on Climate Change (IPCC), “2023: Summary for policymakers,” Climate Change 2023: Synthesis Report. Contribution of Working Groups I, II and III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change [Core Writing Team, H. Lee and J. Romero (eds.)] (Geneva, Switzerland: IPCC), pp. 1–34.

4 Bundis et al., “Carbon caption, utilization and storage,” IEA, last updated July 11, 2023.

5 American Chemistry Council, "2021 Guide to the Business of Chemistry"

6 David Yankovitz, Robert Kumpf, and Aijaz Hussain, “Reducing carbon, fueling growth: Lowering emissions in the chemical industry,” Deloitte Insights, June 2, 2022.

7 Igor A. Bashmakov et al., “Industry,” Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change [P.R. Shukla et al. (eds.)] (Cambridge, UK and New York: Cambridge University Press, 2022).

8 BASF, “BASF, SABIC and Linde start construction of the world’s first demonstration plant for large-scale electrically heated steam cracker furnaces,” September 1, 2022.

Get in touch

${fourth-leader-name}

${fourth-leader-title}

${fourth-leader-additional-info}