Breaking ground without breaking the bank has been saved

Perspectives

Breaking ground without breaking the bank

Modernize your core with Converge™ by Deloitte BankingSuite

Disruption is dominating the banking industry, and patchwork solutions to larger core modernization problems are no longer enough. As costs continue to rise, how can banks implement digital solutions without breaking the bank? Transform your bank—starting at the core—with BankingSuite.

Banking transformation reaches an inflection point

Welcome to the new digital era—but we’ve been here before. Any time new tools emerge, new solutions, strategies, and human behaviors follow—and digital banking is no different. The first mobile phone paved the way for the first mobile wallet, accelerating the adoption of digital banking interactions. A 2023 survey showed that 78% of Americans prefer to bank digitally via web or mobile app.1 An estimated 4.2 billion people around the world are using digital banking services—and that number is only expected to grow.2

In the face of this evolution, banks are working hard to keep up. But patches to existing legacy core banking systems can’t keep up with customer needs and competitors’ innovations. As banks attempt to quickly modernize their core, many are layering patchwork fixes on top of outdated legacy systems. This can leave organizations vulnerable to increased costs, while also limiting the ability to adapt quickly to changing compliance and customer needs.

Breaking ground without breaking the bank

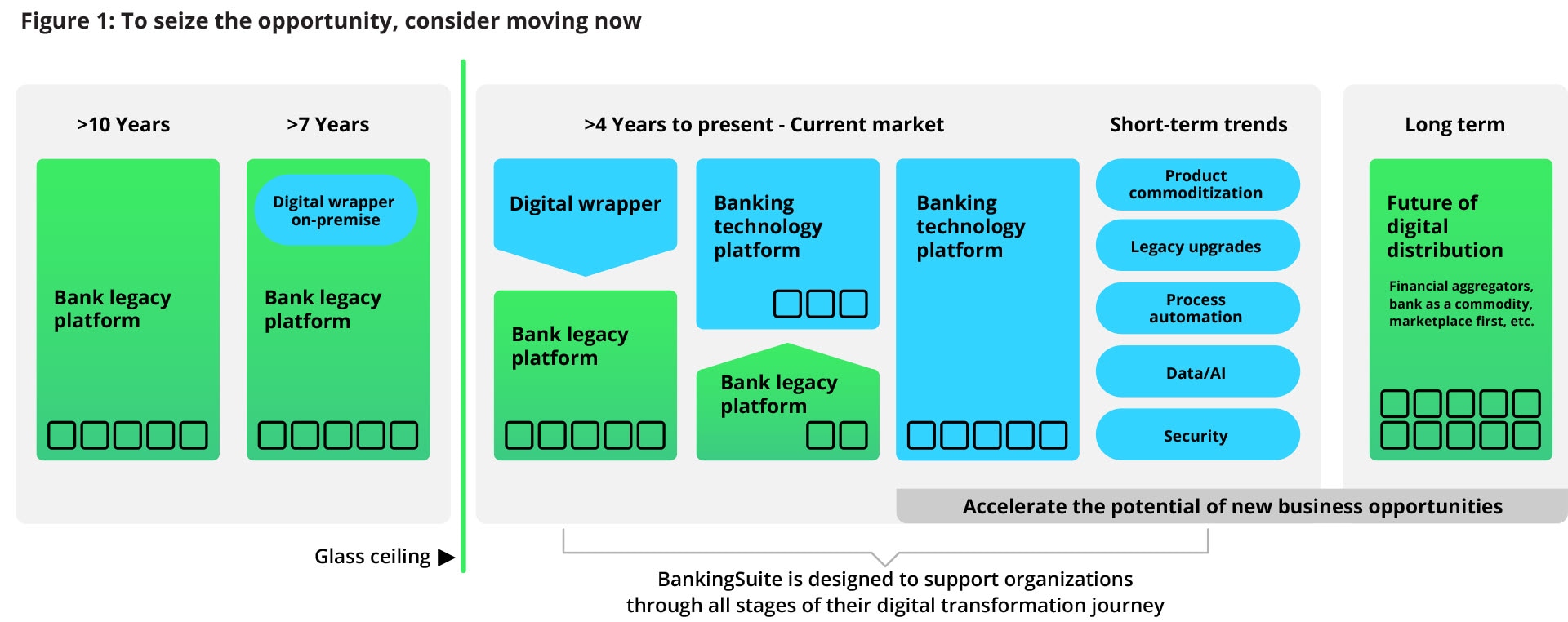

Banks need to power up their core—but it can be daunting to figure out first steps without thinking they must reinvent the wheel (figure 1). No organization needs to do that. The tools for banks to safely leverage next-generation cores for a competitive edge already exist. The key is to move fast and seize the opportunity.

Deloitte’s modern core banking practice has worked with many clients to develop strategies to find opportunity, set tailored goals, and safely move fast to get their banking programs off the ground. The results are achievable, modernized cores, and a competitive edge for the future.

Why consider core modernization now?

We’re at a tipping point as disruption becomes the name of the game and competitors gain an edge. Many banks are investing aggressively to modernize their core and entire technology stack. But for banks that are on the fence about investing, here’s why they should act now:

Legacy core banking systems can no longer keep up with consumer product innovation. Products and features such as saving pockets, smart interest rate credit cards, real-time payment processing, real-time consumer spending analytics, real-time marketing offerings, and real-time fraud detection are all in focus for forward-thinking banks that want to provide business and customer experience benefits.

Legacy core operational challenges will mandate modernization for banks. Legacy core providers will no longer support first-generation mainframe solutions. As the older workforce nears retirement, young engineers are interested in learning modern coding languages, not supporting legacy systems. A modern core requires a tech investment and an evolution in talent. The resiliency of legacy core tenants is also being challenged as daily issues keep many operational back offices up at night.

Digital innovation investment is high, but returns can be diminishing. Many peripheral systems such as online banking have implemented cloud-native solutions. But investments at the edge of a stack are expensive, are time-consuming, and can stifle a bank’s ability to evolve. Integrating new systems with legacy mainframe cores requires high investment and can create diminishing returns when considering the opportunity cost of modern cores. A roadmap for organizations’ individual challenges and needs is vital to success.

Choosing a path toward core banking modernization

Banks are increasingly getting comfortable with implementing new technologies at scale. But how? Two key ideas: vendor maturity and a carefully designed implementation strategy that addresses executional and operational concerns across the institution. Acknowledging the need for a modern core is not the central challenge for banks. Instead, a bank must decide how to move forward and implement a new core that’s curated and designed for its goals, helps achieve business outcomes, and solves organizational challenges.

When designing a digital solution, banks should consider these issues:

- Legacy vs. greenfield: Consider whether legacy or modern peripheral capabilities will support the core.

- Customer transition: How should banks handle legacy customers and legacy products?

- Finances: Prioritize revenue generation and cost optimization across the IT and business landscape.

- People impact: Consider the appetite for changing the business operating model.

- Organizational change: The bank’s risk appetite will determine whether it moves faster or slower.

- Regulatory posture: Prioritize outcomes needed to improve the bank’s ability to address challenges.

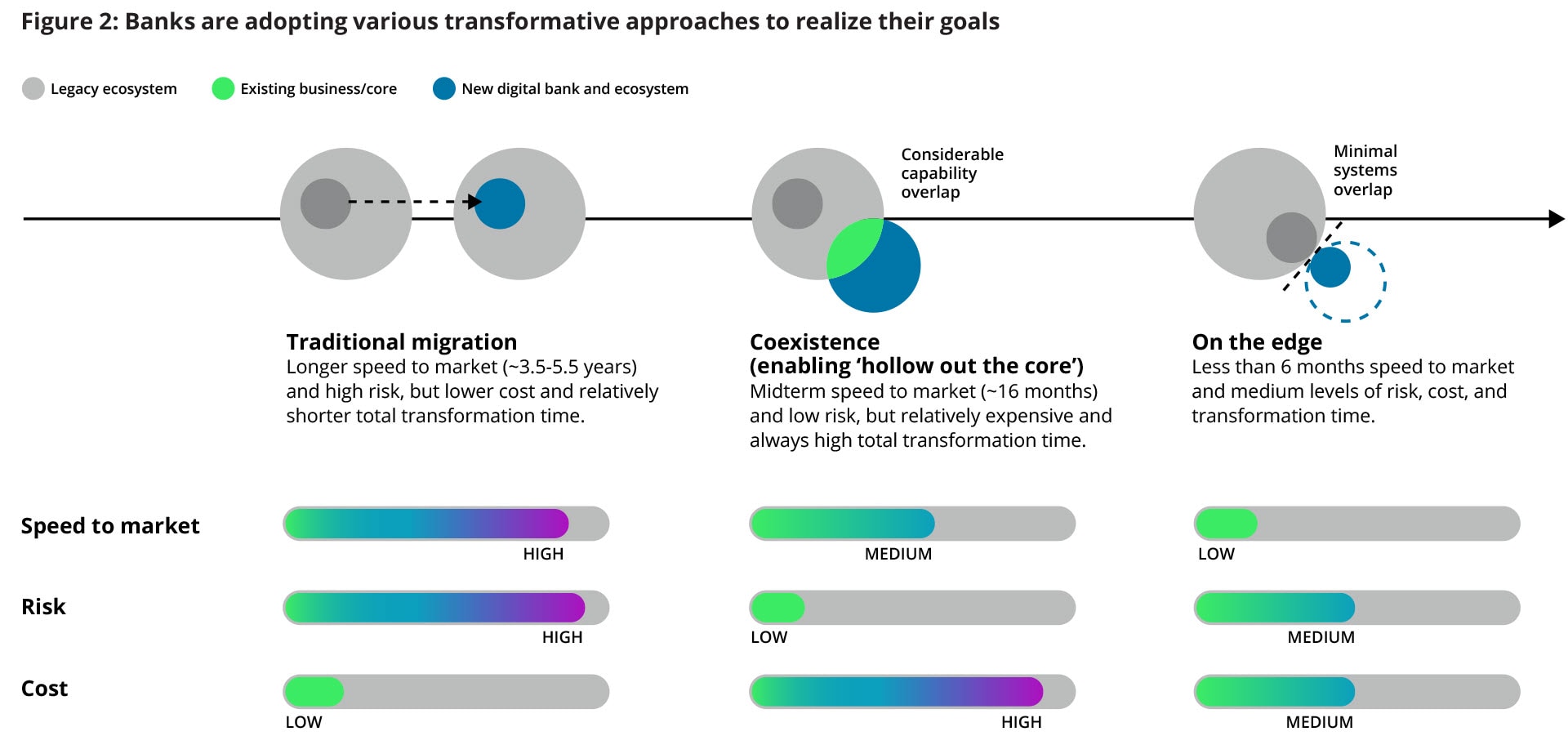

We’ve seen three popular emerging paths: a traditional migration, a dual-core coexistence, and an “on the edge” banking transformation. The path a bank chooses can help enable pragmatic, lasting modernization for front- and back-office experiences and solve near-term systems integration and infrastructure challenges. There’s a rationale for each path—but the choice depends on an organization’s goals.

The Converge by Deloitte BankingSuite approach

Core modernization is a big undertaking with a myriad of opportunities and challenges to consider, and navigating different programs and choices can be a windy road if a bank lacks a clear view of cost, organizational benefits, and time to realize those benefits.

Converge™ by Deloitte BankingSuite, our modern, composable banking platform, integrates the ecosystem with our cutting-edge software and fills the gaps between what is out there and what you need to succeed. Supported by the power and historical knowledge of Deloitte, our BankingSuite team gives clients better assurance that the investments they make will work for the future. Here’s some of the ways we are helping clients accelerate time to value during early-phase core modernization strategy and planning.

${header-title}

${column1-large-text}

Rapid core strategy definition

Deloitte’s proprietary desirability, viability, and feasibility (DVF) framework has helped clients of all sizes rapidly develop a fully integrated core strategy across product and innovation desirability; financial, operational, and regulatory viability; and technology architecture feasibility.

${column2-large-text}

Modern core proof of concepting

BankingSuite provides our clients with an immediately deployable, full-stack digital banking environment with integrated next-gen cores to quickly assess and provide proofs of concept for various product journeys to reimagine the vendor selection and architectural blueprinting process.

${column3-large-text}

Digital banking blueprinting

Deloitte’s digital banking architecture blueprints provide a starting point to the build of your unique fintech ecosystem and tech capabilities. This includes Deloitte’s library of coexistence architecture patterns and proprietary coexistence infrastructure that is fully integrated into BankingSuite.

${column4-large-text}

${column4-title}

${column4-text}

Potential benefits

As we move into a new digital era, one thing is certain: Banks that capitalize on these next-gen core opportunities can potentially see huge benefits in customer share and profitability, internal skill sets, ability, agility, and long-term plans.

- 20% to 40% increase in five-year revenue potential

- Up to 75% lower innovation costs for new product launches

- 40% to 60% reduction in operating costs across categories

- 30% increase in future digital banking features and product releases

- Less than six months to market thanks to leaner, agile delivery models

- 20% to 30% increase in IT and business operational efficiency from real-time transaction processing

- Up to 65% increase in staff efficiency, shifting focus to value-add work

Breaking ground without breaking the bank

Check out our full report for a deeper dive on how we got here, the current digital banking landscape, and why the time is now for core modernization. And visit Converge by Deloitte BankingSuite to see how our digital banking solutions can help you power up to modern banking.

Get in touch

Endnotes

1 Jenn Underwood and Elizabeth Aldrich, “U.S. consumer banking statistics 2023,” Forbes Advisor, March 24, 2023.

2 Juniper Research, “Over half of global population to use digital banking in 2026,” press release, July 19, 2021.

Recommendations

Converge Banking

Technology solutions to help you reimagine the future of banking.

Core banking solutions that capture the heart of your bank

BankingSuite and AWS set the stage for modern banking