The vaccinated ‘in-store’ future of retail after COVID-19 has been saved

Perspectives

The vaccinated ‘in-store’ future of retail after COVID-19

Retail industry trends provide a shot of optimism

Nearly three years into the pandemic, retailers are ready for a shot of optimism. The numbers provide it, as surveys show consumers are now comfortable going into a physical shopping environment. But they want the features and conveniences of online shopping. See the retail industry trends and what the future of retail after COVID-19 looks like.

The future of retail after COVID-19 is promising

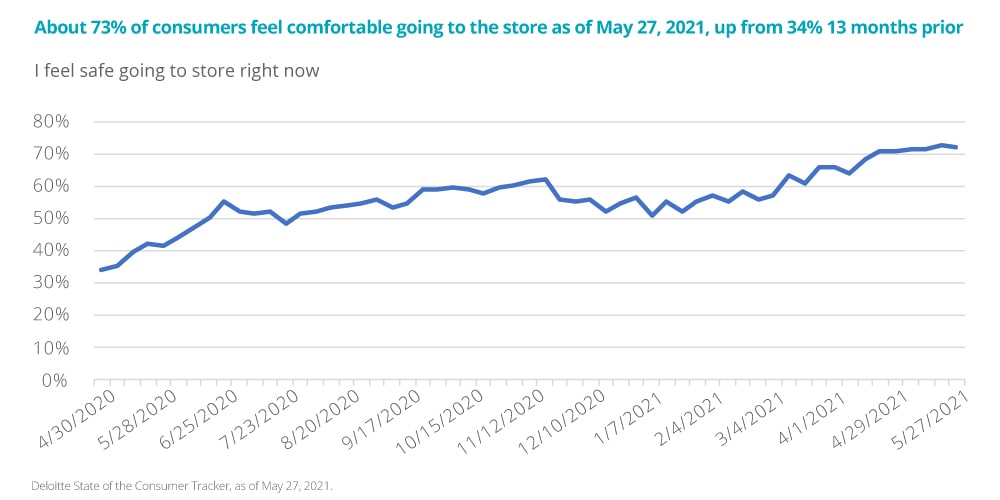

More than half of Americans are now fully vaccinated. States and businesses are relaxing COVID-19 restrictions in line with new CDC guidance. And consumers are rapidly returning to public life. That’s all good news for the future of retail, as nearly 3 out of 4 consumers felt comfortable going into a physical store in May 2021, up from just one-third over the previous year.1

This injection of optimism can’t come soon enough for retailers, as the vast majority rely on physical locations to serve many of their customers and drive topline results.

What’s ‘in store’ in a vaccinated world

Published July 2021

COVID-19’s initial impact on spending

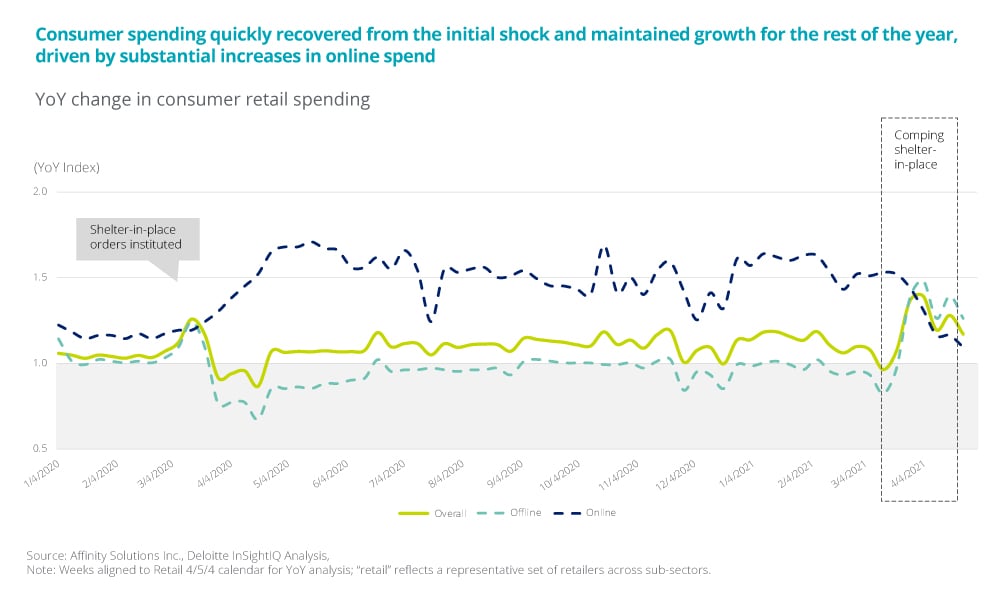

As US cities imposed lockdown and quarantine measures in early 2020, there was a substantial short-term drop in consumer spending, and the impact on brick-and-mortar stores was dramatic. While overall sales and revenue recovered from the initial shock and maintained growth for the rest of the year, driven primarily by substantial increases in online spend, physical retail continued to see muted growth or slight declines.

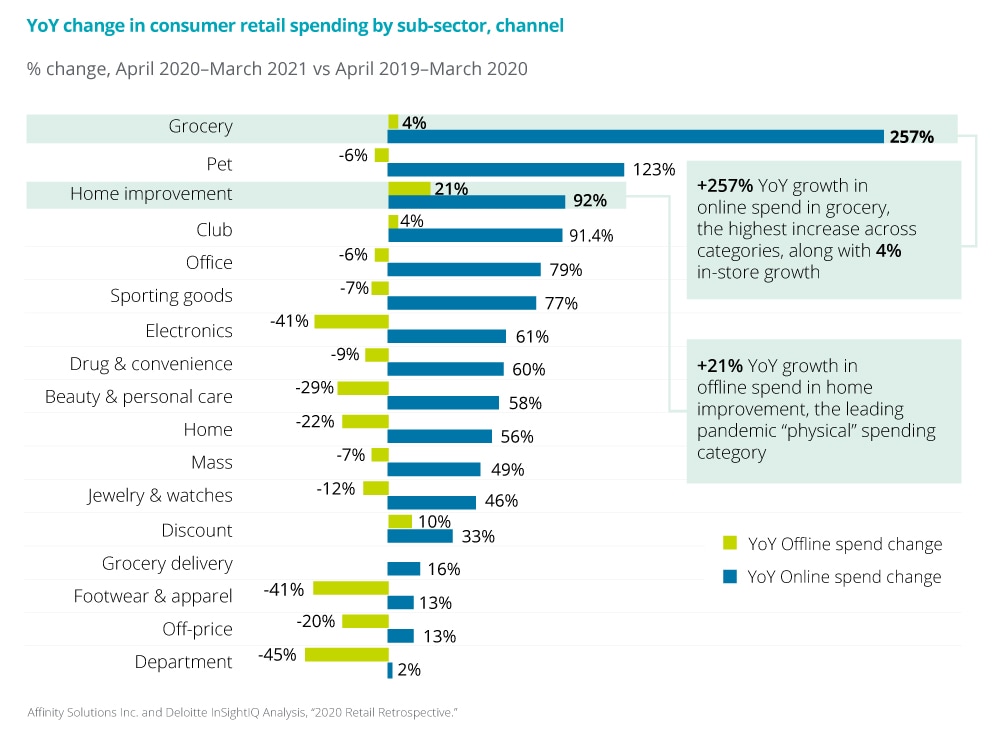

Not all categories are created equal, and not all retailers had the same experience in 2020. As initial lockdowns forced discretionary retailers to shutter thousands of stores, many categories saw a substantial decline in offline spending, with department stores, footwear and apparel, and electronics taking the toughest blows.2

But retailers that reopened their doors in summer 2020 (after any temporary city- or state-forced closures) saw their in-store spend rebound to pre-pandemic levels—and other retailers even enjoyed great gains. Home improvement experienced 21% year-over-year growth in offline spend. And grocery saw more than 257% year-over-year growth in online spend (the highest increase across categories), along with 4% in-store growth.

With Americans returning to travel and event-based life, retailers face additional competition. Restaurants, leisure, and other sectors are also vying to provide renewed in-person experiences that will compete for share of wallet (and for grocery retailers, competition for share of stomach). As the role of the physical store evolves to meet shifting demand, retailers must fight for the attention of the energized consumer and capitalize on Americans’ renewed desire for social connection while providing them with the products and services they expect in the shopping modality they prefer.

However specific retailers fared during the pandemic, the priorities and expectations of the post-pandemic consumer have irrevocably shifted. As a result, all retailers must now consider transforming their store offerings to serve customers in the “next normal.”

All retailers must consider transforming their store offerings to serve customers in the “next normal.”

Digital and physical are here to stay

Digital shopping gave consumers a safer way to buy the goods and services they needed during the pandemic, and their digital behaviors seem to be sticking. Online spend now accounts for 37% of total retail spend, up from 27% pre-pandemic.3 The pandemic has rapidly accelerated consumer shifts that were expected to take hold over the next several years, but this past year certainly raised the bar.

Despite the dramatic increase in overall online spend, many consumers still prefer physical retail for some or even all of their shopping. They value the experience: a personalized, engaging immersion with the brand. They visit to touch or try the product and feel confident in their purchase decision or to engage store associates for specific services. And they enjoy the convenience of the physical channel, which allows for the real-time, immediate purchase (or return) of a good.

As consumers return to physical stores, they also want digital options to stay, with nearly 90% of consumers looking for a digitally enhanced shopping journey, whether engaging at home, via mobile, or inside a physical location.4 Retailers are compelled to embrace these changes to serve the post-pandemic consumer.

As consumers return to physical stores, they also want digital options to stay, with nearly 90% of consumers looking for a digitally enhanced shopping journey.

Investing in physical assets: Three key steps for retailers

As physical traffic rebounds and retailers look to capitalize on the pent-up demand for shopping, there will be big opportunities, but also risks and implications for the brand and bottom line. Here are three areas retailers should consider as they prepare for the next normal:

As consumers return and accelerate in-store spend, their shopping patterns and behaviors are unlikely to mirror pre–COVID-19 examples. They’ll still expect a safe, seamless, and pleasant experience, but they’ll now also look to use their local store as a convenient curbside pickup location. Retailers should be prepared to reengineer store layouts and enhance their customer experience by:

- Expanding fulfillment areas and technology. Building on the sustained usage of BOPIS and stores as a delivery hub, retailers should consider reallocating sales floor space to enhanced customer pickup areas, allowing customers easy access to prepared orders. They should also explore expanding the back room, leveraging and prioritizing additional space to fulfill and stage incremental BOPIS and e-commerce orders. In addition, taking a closer look at micro-fulfillment centers and other automated fulfillment options can help retailers lower the cost to serve for each order, decrease the time and effort for associates to pick and pack an order, and improve the customer experience by reducing the number of mis-picked items.

- Reducing friction. With consumers seeking an overall shopping experience with less friction, retailers should accelerate technology investments to improve the shopping journey. Self-serve kiosks, mobile checkout and contactless payment, enhanced in-store Wi-Fi, and incremental mobile app features (such as shopper maps, augmented reality, etc.) can put the consumer in the driver’s seat of their shopping experiences and reduce some of the pain points typically experienced in-store.

Whether a retailer added associates over the past year or was forced to make labor cuts, many companies are facing significant staffing challenges as the recovery continues. Prospective employees are in high demand as the economy accelerates, not only in retail, but also in competitive sectors such as leisure and hospitality, which is forcing retailers to compete for talent.

As customers return, stores will need associates who are trained and ready for increased traffic and interactions. Retailers can help ensure they have the right staff in place by:

- Retraining and cross-training associates. With the current challenges in recruiting new associates to fill open roles, many retailers will look to retain and rapidly train existing employees to handle different or incremental responsibilities. Leveraging new technology, such as mobile microlearning, along with augmented and virtual reality, can enhance and accelerate training capabilities at scale across a large store footprint.

- Empowering store teams. Regardless of the retail category, store associates have had a long and challenging year. Reinvigorating frontline staff roles by empowering, engaging, and connecting their actions to the retailer’s overall success can improve the overall team environment and thereby the customer experience. Enhancing associate communications and providing access to daily metrics and insights can improve the overall associate experience, as well as engagement.

Consumers increasingly expect to be able to shop for any item, when and how they want it, faster than ever. The impact on retailers should be addressed not only in stores, but also upstream throughout the supply chain, which is undergoing its own omnichannel transformation as well. Retailers can capitalize on this end-to-end transformation by:

- Offering real-time inventory visibility for customers and associates. Retailers can use item-level tagging, computer vision, or other enabling technology to provide more transparency into whether an item is available. This will enhance a customer’s experience online and in the store and also help associates improve in-store location and fulfillment of items.

- Improving processes to limit and enable returns. Retailers can improve the customer experience by enabling in-store returns for e-commerce purchases, leveraging artificial intelligence and machine learning to optimize and standardize policies for costly returns. They can also consider investing in augmented and virtual reality technology for virtual try-ons and sizing, which could limit mistaken purchases and reduce return rates for products such as apparel and home goods.

Embrace what’s next

For retail, there’s no return to the past “normal” after the pandemic. Customer shopping preferences shifted greatly over the past year, and they now have a strong desire for flexibility and options.

As retailers put the “customer at the center” and focus less on binary channels, we believe we’re on the verge of a transformation of physical retail. This transformation will allow retailers to better connect with their customers and provide them with seamless options to shop whenever, wherever, and however they want.

For retail, there’s no return to the past “normal” after the pandemic.

Endnotes

1 Deloitte, State of the Consumer Tracker, as of May 27, 2021.

2 Affinity Solutions Inc., Deloitte InSightIQ Analysis, “2020 Retail Retrospective.”

3 Ibid.

4 According to Salesforce, State of the Connected Customer (4th ed.), October 27, 2020, 88% of consumers also expect retailers to accelerate their overall digital initiatives, especially with respect to the in-person experience.

Get in touch

Jean-Emmanuel Biondi

Principal | Retail, Wholesale & Distribution

The authors would like to thank Katelynn King, Carol Cui, Farzain Rahman, Eliza Brodie, Nilesh Phillips, and Megan Ames for their support and collaboration.

Recommendations

Retail trends: Customer centricity shift to stick

Rethinking retail stores for differentiation and growth

Post-COVID strategies for retailers: Reopening stores

Rethink in-store and online customer experience