Semiconductor sustainability: Emissions reduction by design has been saved

Perspectives

Semiconductor sustainability: Emissions reduction by design

Four energy efficiency solutions for semiconductor products

Among industry leaders, a cooperative, ecosystem-wide effort is under way to reduce energy use, and emissions, across the entire semiconductor life cycle. Driven by demand, these semiconductor companies are working with each other, with customers and from within to prioritize energy efficiency—from manufacturing through to end use.

Context:

Semiconductors have become ubiquitous across the modern economy, with applications ranging from their use in artificial intelligence to 5G communications, from automobiles to medical devices, and more. 1 As semiconductors become an essential component of nearly all electronic devices, their associated impacts on product energy use and emissions are critical to global decarbonization.2 The chip industry’s annual revenue is expected to almost double from $515 billion in 2023 to $1 trillion globally in 2030. Semiconductor manufacturers have recognized a new imperative to meet increasing demand while decreasing energy use and emissions.

Indeed, global energy use by products containing semiconductors has doubled every three years since 2010, and this trend is expected to accelerate as the global economy continues to electrify and more energy-intensive computing applications such as artificial intelligence3 continue to be adopted. The underlying design and specifications of semiconductors have a direct impact on the energy efficiency of the larger products into which they are incorporated, making them a key leverage point for reducing the energy used to power, control, and cool myriad products throughout their life cycle use.

Learn how the semiconductor industry is working proactively to reduce energy use across the full product life cycle.

How are these factors manifesting for semiconductor manufacturers?

Energy efficiency drivers and solutions in today’s semiconductor sector

Energy efficiency pressure

Deloitte’s experience suggests that the varied pressures to reduce the life cycle energy needs of semiconductor products can be expressed via three main drivers:

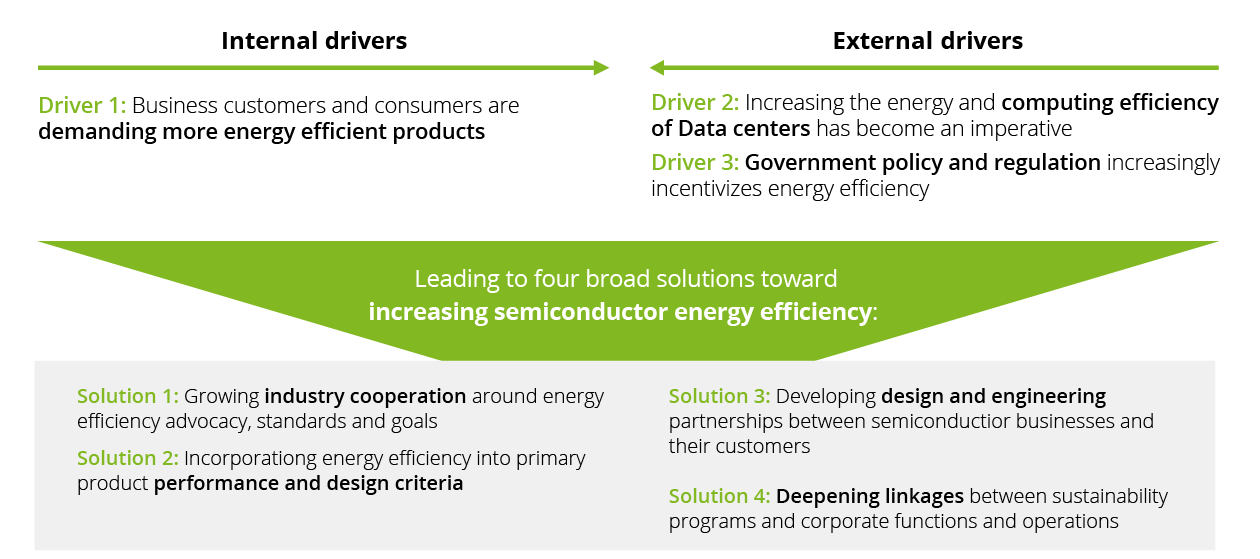

- Driver 1. Business and consumer demands for more energy-efficient end products

As the markets for semiconductor-powered products mature, competition for highly efficient products has intensified. Consumers want electric vehicles with longer ranges and laptops with longer battery life, among countless other use cases. At the enterprise level, businesses demand improved efficiency of renewable energy production and storage, vehicle fleets, and their computing and communications infrastructure, all of which rely on semiconductors.4 To meet these industry shifts and the changing preferences of their end users, manufacturers of products containing semiconductors are increasingly demanding high-efficiency chips—and they are increasingly incorporating these into procurement criteria and pricing. The market for semiconductor sensors and control devices that can more efficiently modulate the energy use of industrial and consumer machinery is also rapidly growing

- Driver 2. Increasing the energy efficiency of data centers has become an imperative

Data centers consume massive amounts of energy—roughly 10–50 times more per square foot than typical commercial buildings,5 and approximately 1.0% to 1.3% of total global electricity consumption.6 While data center workloads increased by 340% from 2015 to 2022, their energy use increased by only 20% to 70% during this time, due to strong efficiency improvements in IT hardware and cooling and a shift toward more efficient cloud and hyperscale data centers.7 As the number and energy intensity of internet users increases with population growth and shifts toward more computing-intensive uses such as generative AI and broadband wireless communication, additional gains in energy efficiency will be essential to offset the expected increases in data center computing and transmission requirements.

In addition to the business benefits of reduced energy costs, these expectations are amplified by the fact that most data center owners have ambitious climate goals that they will be expected to meet, and municipalities in which data centers are located are introducing stringent sustainability requirements. Microsoft, Google, and Meta all have set targets for reaching net-zero by 2030 (carbon negative for Microsoft), and Amazon by 2040. Nevertheless, these players have more than doubled their combined energy use between 2017 and 2021.8 Semiconductors—a primary component of data centers—have been and will continue to be a central part of making data centers more energy efficient.

- Driver 3. Government policy and regulation increasingly incentivizes energy efficiency

A range of government policies and incentives in the United States and Europe are driving a transition to greater energy efficiency, which in turn, is strengthening demand for more efficient semiconductor products. In general, these types of policies work in one of two ways: by directly incentivizing greater energy efficiency, or indirectly by requiring greater transparency and reporting of energy use.

In the United States, the Environmental Protection Agency’s (EPA) Energy Star program has for some time provided specifications for certification of data storage products and scores data centers on a 100-point energy-efficiency scale.9 These incentives have been greatly strengthened by the Inflation Reduction Act, which includes significant grants and other incentives for energy efficiency in buildings, corporate fleet electrification, and renewable energy expansion, among other areas. Each of these relies on enabling semiconductor technologies. These direct incentives are complemented by the recently passed California Climate Corporate Data Accountability Act (SB 253) as well as the European Union’s Corporate Sustainability Reporting Directive (CSRD). Broadly, these require companies to publicly disclose and verify their Scope 1, 2, and 3 greenhouse gas emissions, thereby creating pressure to reduce energy use and the related emissions.When these incentives are viewed in the context of the CHIPS Act, which is prompting semiconductor companies to investigate opportunities to expand their R&D, manufacturing, assembly, packaging, and testing in the United States, one can anticipate increased investment in the design and production of increasingly energy-efficient semiconductor products.

In response to these drivers, semiconductor companies are pursuing a strategy of designing their products to use less energy over their full life cycle. What solutions are they pursuing to advance this strategy?

Deloitte sees semiconductor companies improving the energy efficiency of their products and end uses using four broad solutions:

Solution 1: Growing industry cooperation around energy efficiency advocacy, standards, and goals.

The semiconductor industry has shown significant interest in reducing life cycle energy use and thus emissions from use of their products. The Semiconductor Climate Consortium, for example, was founded in 2022 and consists of more than 70 companies, including all the largest chipmakers, to develop decarbonization solutions in support of the Paris Climate Agreement’s goal of limiting the increase in global temperatures by 1.5 degrees Celsius.10

Solution 2: Incorporating energy efficiency into primary product performance and design criteria.

Just a decade ago, increasing the speed and computing performance while reducing physical size often took priority over reduced energy use when chip companies optimized their products. Today, companies optimize PPA (power, performance, and area) and energy efficiency is a key consideration. More efficient chips enable lower lifetime climate emissions, but also longer battery life for mobile devices and less waste heat produced in data centers. They also have the business benefit of reduced total cost of ownership due to lower energy costs. Supply chains and manufacturing processes are fast evolving to enable these efficiency gains.

Solution 3: Developing design and engineering partnerships between semiconductor businesses and their customers.

Energy efficiency has become a critical performance element of many products that incorporate semiconductors. Examples include increasing the range of electric vehicles, extending the battery life of myriad “smart” products, the use of semiconductor sensors and drive modules to increase the energy efficiency of industrial machinery and internal combustion engine cars, and designing processors optimized for the latest data center cooling technologies and energy distribution systems. Achieving ever-higher energy-efficient performance of end products increasingly demands that the specification and physical layout of semiconductors and integrated circuits (ICs) is matched to end-product design at increasingly finer tolerances. This is driving ever-closer design and engineering partnerships between semiconductor companies and their customers to co-develop energy-efficient solutions, such as those recently announced between GM and its supplier Global Foundries.11

Solution 4: Deepening linkages between sustainability programs and corporate functions and operations.

Deloitte observes that many semiconductor companies are increasing the role of functional, operations, and business executives in leading corporate sustainability strategies and are also embedding sustainability proficiency and capabilities into each of these business areas. This level of integration of sustainability into the business supports both the attainment of market-leading energy performance, and the capture of potential branding, pricing, and other indirect benefits to the business.

Take a deeper look at industry drivers and solutions in our Semiconductor Sustainability series

In conclusion

The solutions outlined above are being adopted with broad consistency across companies. Deloitte anticipates that leaders in the semiconductor sector will continue to innovate and raise the industry’s standards for energy efficiency in their products, making overall product life cycle emissions a differentiator in the marketplace. Relative success may be driven by progress in implementing solutions 3 and 4, which underpin the level of coordination across business functions and value chain actors needed to drive deeper change. In this decisive decade for climate change, few dispute that the time to act with innovative solutions is now. Semiconductor companies are in the unique position, with distinct responsibility, to influence the trajectory of the tech industry’s progress toward net-zero emissions.

Endnotes

1 Semiconductor Industry Association (SIA), “Building America’s innovation economy,” April 2023.

2 President’s Council of Advisors on Science and Technology, Report to the President: Revitalizing the U.S. Semiconductor Ecosystem, September 2022.

3 Margaret Mann and Vicky Putsche, Semiconductor supply chain deep dive assessment, US Department of Energy, February 24, 2022.

4 Ari Zoldan, “Small components, big improvements: How new semiconductor devices reduce energy consumption,” Nasdaq, April 4, 2022.

5 Office of Energy Efficiency & Renewable Energy (EERE), “Data centers and servers,” accessed January 17, 2024.

6 Ibid.

7 International Energy Association (IEA), “Data centres and data transmission networks,” last updated July 11, 2023.

8 Ibid.

9 US EPA, OA. 2021, “ENERGY STAR Expands Efforts to Improve Energy Efficiency of U.S. Data Centers," August 16, 2021.

10 Dashveenjit Kaur, “The Semiconductor Climate Consortium’s timely goals,” Tech Wire Asia, June 7, 2023.

11 Jamie L. LaReau, “New GM partnership gives automaker long-term supply of semiconductor chips,” Detroit Free Press, February 9, 2023.

Get in touch

Recommendations

Semiconductor | Deloitte US

Deloitte's semiconductor consulting practice can solve critical issues. Explore semiconductor industry trends, from M&A to cloud to IoT, to help drive growth.