Semiconductor sustainability: Uncovering new revenue streams has been saved

Perspectives

Semiconductor sustainability: Uncovering new revenue streams

Five solutions for value creation and brand differentiation

Semiconductor companies are responding to various consumer, corporate, and other demands, implementing five key strategies to drive business value through sustainability-related brand differentiation, as well as new business lines and revenue streams.

Context:

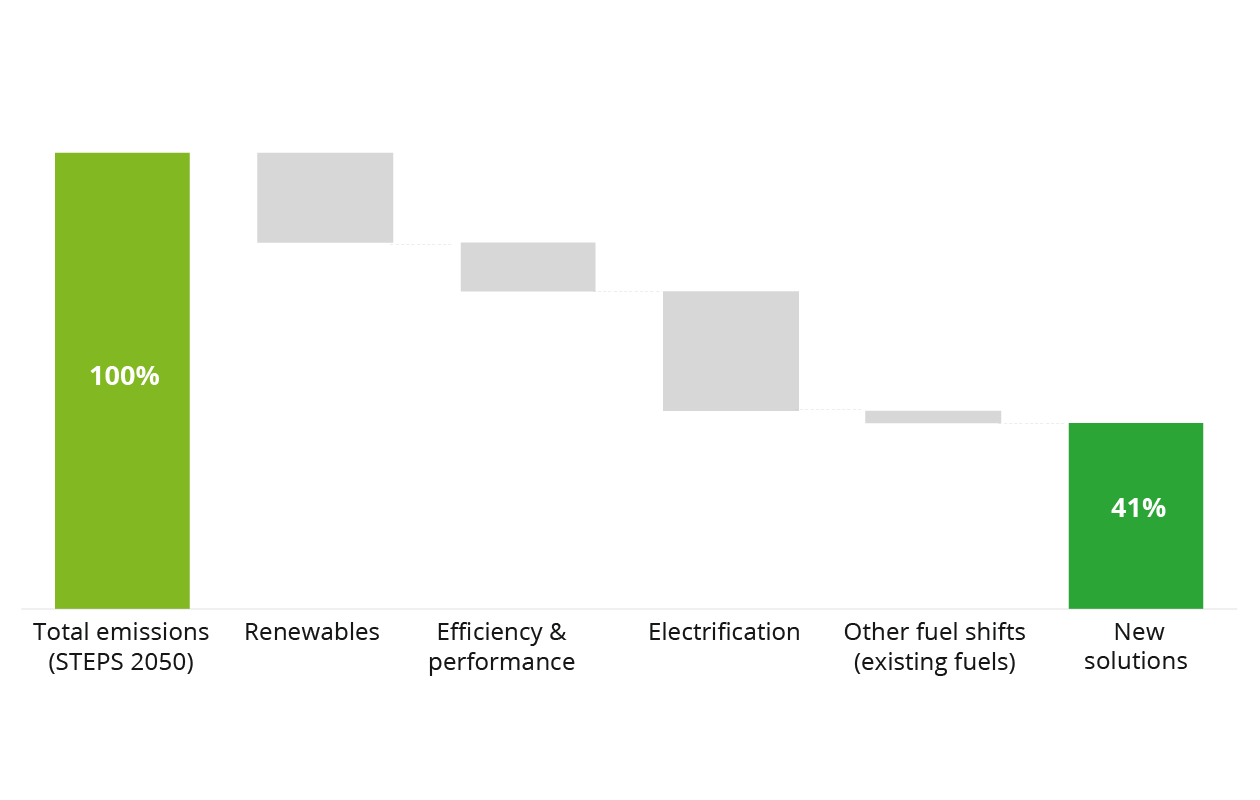

In a recent global survey of business executives,1 75% of CxOs said their organizations have significantly increased sustainability investments, while 61% reported that climate change will have a high or very high impact on their company’s strategy and operations in the next three years. The market for new sustainability solutions seems set to grow rapidly: Estimates suggest that around 40% of carbon reductions needed to achieve 2030 Paris Agreement commitment goals will rely on new technologies, indicating significant demand for new climate solutions.2 Deloitte predicts this “hardtech” climate market spending will require more than $2 trillion of financing.3

|

Both pure play and vertically integrated semiconductor companies are exploring ways to harness consumer and corporate demand for sustainable products as a value driver, in both product and service markets. They are creating new revenue streams such as emissions reduction advisory services and premium pricing for versions of their products with sustainable features such as use of recycled materials. Some industry players are also experimenting with “as a service” delivery of their products’ capabilities, which can reduce energy and transportation impacts while generating additional service-related revenue.

A well-executed sustainability-related business can help achieve many benefits, including growing and diversifying revenue streams, improving brand and employee perceptions by addressing stakeholder expectations for sustainability, and helping customers achieve their sustainability goals. It can also help to drive innovation and operational excellence as semiconductor business leaders develop new solutions and business models.

Learn how the semiconductor industry is driving value and sustainability objectives in parallel.

How are the market drivers and opportunities for delivering new sustainability-related offerings manifesting for semiconductor manufacturers?

Drivers and solutions for developing business value from sustainability investments

Deloitte’s experience highlights the varied reasons for semiconductor companies to seek sustainability-related business value to generation being expressed via four main drivers:

- Driver 1: Growing sophistication of semiconductor companies in sustainability.

Many semiconductor corporations now have several years’ experience with their own environmental and social sustainability programs. They are often increasing the integration and collaboration between their sustainability capabilities and their corporate functions and business units. Both midsize and large semiconductor manufacturers reorganize their sustainability teams to involve leadership from business unit executives, for example.4 This is equipping them to identify potential sustainability markets. - Driver 2: Pressure to grow and diversify revenue streams.

Perhaps especially in a potentially slowing economy, there is an interest in offsetting investments made in sustainability, and in generating new revenues that leverage sustainability capabilities. There is growing recognition of the market opportunity to provide sustainability-related offerings to customers. Some of the largest semiconductor brands have launched initiatives to explore this market potential.5 - Driver 3: Consumer demand for products that cause less environmental harm.

Semiconductor companies are finding that consumers are willing to pay a premium for sustainability attributes in some product segments. A 2019 study6 found that students in Sweden and Norway were willing to pay an average of 18% more for a mobile phone marked with environmental or social sustainability labels, while German students were willing to pay 12% more. Companies in the semiconductor sector have an incentive to capture a brand and pricing premium by adopting sustainability practices and promoting them as a feature of their products. - Driver 4: Increasing demand from corporations for sustainability-enabling products and services.

Semiconductor companies are finding that many of their biggest corporate customers have sustainability and energy use goals, which creates the potential for new semiconductor products and services that help to achieve those goals and/or report on progress toward them. In the business-to-business space, willingness to pay a premium for green products is significantly higher than in the consumer sector, nearing 30%.7 For example, green data centers are growing rapidly with a CAGR of 16% through 20308 as a result of ever-growing global computing and storage needs and a heightened focus on sustainability as a cost-reduction driver.

In response to these drivers, semiconductor companies are pursuing a strategy of providing sustainability-related products and services. What specific solutions are they introducing?

- Solution 1: Positioning products with sustainable features for premium branding and pricing.

Some consumer segments are increasingly willing to pay a higher price for products built with sustainability in mind, whether it be low energy use, inclusion of recycled materials or design for easier repair or recycling.9 Certain products with reduced environmental impact can attain the “Lower CO2” label from the Carbon Trust as an additional credential for their product. As consumer-facing companies with semiconductor-powered products respond to these preferences, they are likely to exert pressure on their suppliers to meet increased standards for sustainable design as well. Vertically integrated companies that manufacture and sell both semiconductors and consumer products that contain them have been some of the fastest movers to capitalize on this trend. Samsung, for example, markets its commitments to reach net-zero by 2050, keep water withdrawal to 2021 levels in 2030, recycle 99.9% of waste by 2030, and keep air/water pollutants to a natural state by 2040.10 Dell similarly aims to achieve net-zero by 2050; use 100% recycled or renewable materials for its packaging; and use more than 50% recycled, renewable, or reduced carbon materials for its products.11 In addition to leveraging the benefits of company-level commitments and supporting investments for direct brand uplift with consumers, companies that lead on sustainability will likely position themselves as suppliers of choice for customers with increasingly ambitious product-level sustainability goals.

- Solution 2: Introducing products designed to help reduce customers’ emissions.

Across industries, there has been a shift toward investing in increased sustainability and efficiency. This has been driven by both a desire to address sustainability demands and the opportunity to reduce energy and other input costs. Semiconductor sensors and controllers are frequently used to drive greater efficiency of industrial processes and products, and as a result, semiconductor companies are increasingly developing and introducing new products to supply this fast-growing market.12

A good example of this is in semiconductor products designed to enable data center efficiency. As use of artificial intelligence and machine learning grows exponentially, the world is expected to create and replicate 163 zettabytes of data by 2025, a tenfold increase from 2016.13 Data centers—which will house most of this data—have strong incentives to reduce the energy, water, and waste associated with their operations as they scale to meet rising demand. This pressure comes from regulations, the increasingly limited availability of electricity and water, and local municipality demands. Accordingly, green data centers are outpacing traditional data center growth, growing at a CAGR of 16% through 2030,14 compared to a projected 9.6% CAGR for the total global data center industry.15

Semiconductor companies are responding to this market, developing data center components that require less energy and less cooling, which are optimized to work in modern, high-efficiency data center architectures. Texas Instruments, for example, has developed denser, more thermally efficient power chips that improve energy efficiency.16 Gan Systems has similarly improved the power density of its chips, which allows for data center capacity growth without having to build more data centers,17 and Samsung has improved energy efficiency by approximately 50% over previous generation products through its high-performance SSD memory for data centers.18 While the design standards and materials vary by company, in general, silicon and wide-bandgap semiconductors such as silicon carbide and gallium nitride are critical to enabling these data center energy-efficiency improvements.19

The market for semiconductor products designed to enable energy efficiency goes far beyond data centers, however, and ranges from sensors that boost the efficiency of electric vehicles, to powering smart buildings, to devices that can “idle” industrial machinery when it is not in use. Navitas Semiconductor—historically known for its superfast phone chargers—is making a big bet on electric vehicles and has developed gallium nitride semiconductors that can deliver a purported three times faster charging and 70% energy savings.20 Allegro MicroSystems is similarly focused on improving the efficiency of electric vehicles and has partnered with BMW to deliver inputs that can extend driving range by minimizing power losses.21 These efficiency opportunities extend across Internet of Things (IoT) use cases and include smart controls to manage and optimize energy consumption. Infineon, for example, uses its hardware, software, and tools to enable appliances and systems for smart homes and buildings to dynamically adapt and react to their surroundings, which helps improve their energy efficiency.22

- Solution 3: Capturing more value by incorporating circularity into products, logistics, and business models.

As described in another article of this Semiconductor Sustainability Trends series, semiconductor manufacturers are piloting products, business models and logistics which embody a variety of aspects (e.g. reuse, recycle, resale) of circularity, with the intent of capturing additional value while addressing sustainability issues. Market growth projections are quite strong across a range of circularity approaches: 7% CAGR in the recertified PC market23 through 2030; 8% CAGR for Asset Recovery Services through 202824; and 11% through 202725 for Payment & Ownership Models. See our other article for more details.

- Solution 4: Complementing semiconductor products with as-a-service offerings.

In an as-a-service solution, the traditional sale and physical delivery of semiconductor products to the customer is replaced or complemented by remote access to a variety of services. This offers semiconductor businesses numerous advantages, including the potential to add incremental services and revenue; easier management of repairs and upgrades; and much easier logistics at the product’s end of life (i.e., reuse, recycling, disposal, etc.). As-a-service delivery also has several potential advantages for customers, including reduction of barriers to entry for new IT-dependent services, increased operating flexibility, improved quality of service, replacement of upfront capital expenditure with more flexible operating costs, reduced maintenance costs, easier upgrades, and greater continuity of service—and quite possibly also reduced climate emissions.26 By consolidating products that would otherwise be in use at multiple customer sites into a single efficient data center, operating costs and emissions can be reduced and service continuity improved for customers.

While the current silicon-as-a-service market is relatively small, it’s growing quickly as a result of the above-mentioned benefits. In a recent Deloitte survey, 33% of semiconductor companies expressed that they expect greater than 25% of their revenues to come from subscription-, outcome-, or usage-based models in the next five years.27 Specific business models include subscription-based services linked to usage of silicon devices; platform-based services that provide custom silicon solutions that are IP-centric; cloud-based services to meet rising compute requirements; software-based feature updates; manufacturing-based services, and more.28 Several industry leaders are already capitalizing on these opportunities. AMD’s Radeon™ Pro Graphics and NVIDIA’s GPU Cloud, for example, both offer services on their silicon in the cloud for AI and deep learning application.29 EDGE launched the industry’s first 5G chipset-as-a-service model in 2021, offering customers a platform positioned as future proof that it can scale 5G and AI features as a function of subscription payments. Other silicon-as-a-service offerings have been introduced by Qualcomm, NVIDIA, Intel, TSMC, ASE, Cadence, Synopsis, AMD, and more.

- Solution 5: Providing advisory and analytic services in sustainability.

Corporate customers of semiconductor products frequently have sustainability goals of their own and are aware that the energy consumption of their IT infrastructure can be a significant source of their scope 2 emissions. In response to this, some semiconductor companies are beginning to offer advisory and analytic services to help their customers and end users understand and plan for emission reductions from their IT infrastructure and other sources. Today, these services are offered widely by large technology product companies that purchase semiconductors. IBM, for example, offers a range of climate consulting services, green supply chain/logistics solutions, and energy management tools.30 Some vertically integrated companies that offer both semiconductors and larger technology products, such as Cisco, similarly offer consulting services related to energy efficiency, energy management, and sustainable product life cycle management.31 While few pure play semiconductor companies have entered the sustainability advisory space, it is likely that more will begin to consult their customers on how to use their products in more energy-efficient configurations to capitalize on growing demand for high-performance, high-efficiency inputs.

Take a deeper look at industry drivers and solutions in our Semiconductor Sustainability series

In conclusion:

Semiconductor companies that employ a range of creative business models can capitalize on sustainability as a significant driver of topline growth. Surveys and market experience show that customers are willing to pay more for sustainable inputs,32 and semiconductor companies can help them reduce both their upstream and downstream emissions by supplying low-carbon chips that improve the high energy efficiency of the products they power. New business models such as “as-a-service” offerings or sustainability advisory services can help semiconductor companies generate entirely new revenue streams and diversify their businesses.

Endnotes

1 Deloitte, Deloitte 2023 CxO sustainability report, 2023.

2 International Energy Association (IEA), CO2 emissions reduction by type of abatement measure, 2050 (GTCO2-e, %).

3 Dilip Krishna et al., “Could technology innovations help reverse the climate change trajectory? Not without a lot more money,” Deloitte Insights, July 27, 2023.

4 Deloitte client experience.

5 Ibid.

6 G. Grankvist, S. Å. K. Johnsen, and D. Hanss, “Values and willingness-to-pay for sustainability-certified mobile phones,” International Journal of Sustainable Development & World Ecology 26, no. 7 (2019): pp. 657–64.

7 Sinem Hostetter and Georg Winkler, “B2B growth is where it’s green,” McKinsey & Company, April 22, 2022.

8 Deloitte client experience.

9 Grankvist et al., “Values and willingness-to-pay for sustainability-certified mobile phones.”

10 Samsung, Sustainability page, accessed January 17, 2024.

11 Dell Technologies, “Our ESG goals,” accessed January 17, 2024.

12 Serena Brischetto, “Samsung Semiconductor plants seeds for sustainable future,” SEMI, November 23, 2022.

13 David Reinsel, John Gantz, and John Rydning, Data Age 2025: The evolution of data to life-critical – Don’t focus on big data; focus on the data that’s big, IDC, April 2017.

14 Deloitte analysis.

15 Industry Arc, Data center market – Forecast (2023–2030), 2023.

16 Texas Instruments, “How thermal efficiency is helping data centers run more sustainably,” October 25, 2022.

17 GaN Systems, “Meeting data center directives with GaN Semiconductors,” accessed January 17, 2024.

18 Samsung, “Efforts towards energy efficiency: Semiconductors,” last updated September 1, 2023.

19 Maher Matta, “Revolutions start with the green data center,” Forbes, August 31, 2022.

20 Navitas, “EV: Lowest weight, faster charging,” accessed January 17, 2024.

21 Allegro MicroSystems, “Allegro MicroSystems and BMW Group collaborate on high efficiency transaction inverters for battery electric vehicles,” press release, October 17, 2023.

22 Infineon, “Smart home & smart building,” accessed January 17, 2024.

23 KPMG, Survey of Sustainability Reporting 2022: Big shifts, small steps, 2022.

24 International Energy Association (IEA), “Data centres and data transmission networks,” last updated July 11, 2023.

25 Deloitte analysis.

26 Jérome Rampon and Vincent Mouret, “The case for silicon-as-a-service (SiaaS),” accessed January 17, 2024.

27 Brandon Kulik et al., Semiconductor Transformation Study 2.0, Deloitte, 2023.

28 Rochak Sethi, “Unlocking new frontiers: How semiconductor companies can leverage XaaS to drive value creation,” LinkedIn, April 2, 2023.

29 Jin Zhang, “Decipher the meaning of silicon-as-a-service,” Design & Reuse, June 20, 2018.

30 IBM, “IBM Consulting sustainability services,” accessed January 17, 2024.

31 Cisco, “Products and solutions for environmental sustainability,” accessed January 17, 2024.

32 Grankvist et al., “Values and willingness-to-pay for sustainability-certified mobile phones”; Hostetter and Winkler, “B2B growth is where it’s green.”

Get in touch

Contributors:

Fabian Pineda, Mackenzie Schnell, Pete Edmunds, Kayla Cherry, and Erle Monroe

Recommendations

Semiconductor | Deloitte US

Deloitte's semiconductor consulting practice can solve critical issues. Explore semiconductor industry trends, from M&A to cloud to IoT, to help drive growth.