CFOs Share Perspectives, Priorities, and Plans for 2023 has been saved

Perspectives

CFOs Share Perspectives, Priorities, and Plans for 2023

As published in the CFO Journal for The Wall Street Journal

One in three surveyed CFOs point to economic challenges and a possible recession as the major constraint to achieving their companies’ financial performance goals in 2023.

Pessimism appears to be the prevailing sentiment among CFOs regarding their companies’ finance prospects for 2023, according to Deloitte’s fourth-quarter 2022 North American CFO Signals™ survey. Amid high levels of inflation, rising interest rates, fears of a possible recession, and geopolitical tensions on several fronts, CFOs project a gloomy picture.

“When comparing the most recent results against third-quarter 2022, CFOs lowered their year-over-year growth expectations across the board for key metrics, including revenue, earnings, dividends, capital spending, domestic hiring, and domestic wages,” says Steve Gallucci, national managing partner for the U.S. Chief Financial Officer Program at Deloitte LLP, and global leader for the CFO Program of Deloitte Touche Tohmatsu Limited. The greatest drop-offs were in revenue and earnings growth at 4.2% and 2.9%, respectively, down from 6.2% and 6.4% in third-quarter 2022. Looking to 2023, one in three CFOs point to economic challenges and a possible recession as the major constraint to achieving their companies’ financial performance goals. CFOs also indicate—although to a lesser extent—inflation and rising costs, shrinking consumer purchasing power, and inability to attract and retain talent/labor as constraints to meeting their financial performance goals this year. Amid such concerns, only 29% say now is a good time to be taking greater risk, the lowest level since the second-quarter 2020 CFO Signals survey.

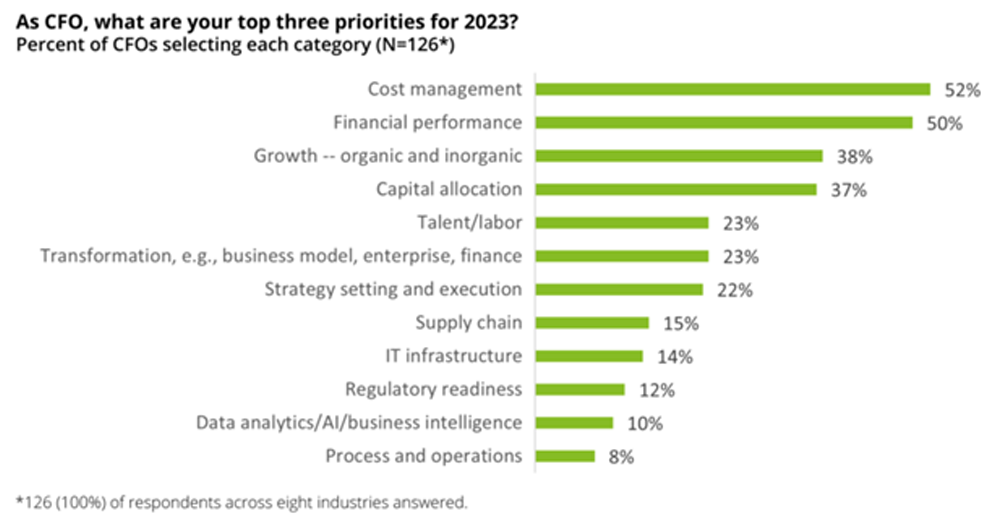

More than half of surveyed CFOs are making cost management and financial performance their top two priorities in 2023, followed by growth, cited by 38% of CFOs. “Going further into 2023 with the continued uncertainty, cost management is going to be critical,” Gallucci says. “For example, CFOs are spending more and more time with their supply chain leaders to understand the drivers of costs and explore ways to stabilize them,” he adds, “and there will likely be some continued passing of costs in prices to customers.” In fact, 57% of CFOs in the most recent CFO Signals survey indicate their companies plan to raise prices for a substantial portion of their products/services to offset inflation.

Other plans for 2023

More than half (57%) of CFOs report their organizations expect to pursue M&A and joint ventures. Fifty-seven percent also plan to expand their range of products and services, with more planning to do so inside North America than in other regions. Two-thirds of surveyed CFOs agree that they will allocate or reallocate capital to new business investments next year, and 49% say they intend to increase investments in ESG.

By and large, CFOs expect an onerous combination of substantially higher input costs and withering demand in 2023. Forty-one percent of CFOs anticipate oil/fuel prices to rise beyond 2022 levels, and one third of them expect inflation to impact costs to the same degree as in 2022. Just 11% each of CFOs expect consumer spending and business investment to increase in 2023, while only 8% anticipate individual investment to increase.

|

Source: “CFO Signals,” What North America’s top finance executives are thinking—and doing, 4th quarter 2022

When asked about their outlook on talent, most CFOs (74%) agree that their companies are likely to see talent/labor costs increase substantially in 2023. Interestingly, 41% say their organizations intend to hire more people than they let go. “We are in the midst of a very tight labor market with a labor shortage,” said Ira Kalish, chief global economist at Deloitte Touche Tohmatsu Limited, when speaking during Deloitte’s CFO 4Sight webcast on January 19. “Attracting people is therefore a very important issue, and so is retaining them,” he added.

While 84% of CFOs say their organizations expect to use automation and digital technologies to free people to use their talents for higher-value activities, 61% of CFOs say their organizations will implement automation and digital technologies to replace certain jobs previously performed by humans. In addition, 79% of CFOs expect their organizations to embed more automation/digital technologies into operations. More than one-third (37%) also report their organizations plan to reduce their real estate footprint. Less than one-quarter of surveyed CFOs (22%) indicate they will increase outsourcing of operations.

In addition, 40% of CFOs say they will repurchase shares in 2023, and 29% expect to reduce or pay down a significant proportion of their bonds/debt. Thirty-six percent say they will seek to reduce their cost of capital, and 26% expect their organizations to hold more cash in 2023.

Views on regional economies

For the year ahead, nearly all signs point downward as CFOs hold dimmer views of the future status of the economies in Europe, China, Asia excluding China, and South America, with North America as the exception. For North America, 29% of CFOs project the economy to be better in 12 months, the same proportion as in the prior quarter. Looking at Asia, excluding China, just 18% expect improvement a year out, compared to 25% in the third-quarter of 2022. In assessing South America’s economy, only 8% of surveyed CFOs expect an improvement in 12 months, down from 10% in the prior quarter.

CFOs are particularly pessimistic about the future states of the European and Chinese economies. Only 9% expect improvement in Europe’s economy one year from now, a decline from 11% in the prior quarter. In assessing China’s economy, 19% of CFOs anticipate better conditions 12 months ahead, a decline from 27% in the prior quarter.

Geopolitics and instability—the external risks CFOs cited as most worrisome, even more so than inflation or recession—are likely factors in their outlooks for the regional economies. CFOs also cite policies and regulations, macroeconomics, labor scarcity and cost, and interest rates and their impact among their most concerning external risks. Other external risks are prices and supplies of commodities, particularly with respect to energy.

—by Patricia Brown, managing director and CFO Signals leader, Deloitte LLP, and Jennifer Malin, manager, CFO Program.

Disclaimer and Copyright

About CFO Signals

Each quarter, CFO Signals tracks the thinking and actions of CFOs representing many of North America's largest and most influential organizations. This report summarizes CFOs' opinions in four areas: business environment, company priorities and expectations, finance priorities, and CFOs' personal priorities.

The CFO Signals survey for the fourth quarter of 2022 was conducted between November 7, 2022, and November 21, 2022. A total of 126 CFOs responded. This survey seeks responses from CFOs across the United States, Canada, and Mexico, and the vast majority are from companies with more than $1 billion in annual revenue. Participation is open to all industries except public sector entities. For more information about Deloitte CFO Signals, or to inquire about participating in the survey, please contact NACFOSurvey@deloitte.com.

PUBLISHED ON: Jan. 31, 2023 3:00 pm ET

This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor.

Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. In the United States, Deloitte refers to one or more of the US member firms of DTTL, their related entities that operate using the “Deloitte” name in the United States and their respective affiliates. Certain services may not be available to attest clients under the rules and regulations of public accounting. Please see www.deloitte.com/about to learn more about our global network of member firms.

Copyright © 2023 Deloitte Development LLC. All rights reserved.

Get in touch

Recommendations

Building Trust in Machine-Powered FP&A

As published in CFO Journal for the Wall Street Journal

Are You a SPAC-Ready CFO?

As published in the CFO Journal in The Wall Street Journal