An introduction to central bank digital currencies (CBDCs) has been saved

Perspectives

An introduction to central bank digital currencies (CBDCs)

Drivers, design, and impact on commercial banks

Businesses and consumers are adapting to digital forms of monetary interactions faster than ever imagined. What are the drivers and key design considerations for central bank digital currencies, an electronic form of central bank money? And what’s the corresponding impact on commercial banks? While there’s no single answer, it’s evident that the evolution of CBDCs will affect the whole financial ecosystem.

Explore content

- An introduction to CBDCs

- Drivers of CBDCs

- Design considerations for CBDCs

- Current global landscape of CBDCs

- Impact of CBDCs on commercial banks

An introduction to CBDCs

A CBDC is an electronic form of central bank money with potential wide use by households and businesses to store value and make payments. It’s central bank digital money in the national unit (e.g., the US dollar) representing legal tender with the liability of the central bank, similar to physical currency in circulation. This makes CBDCs more secure and less volatile than other digital currencies. The following table presents an overview of the purpose of and common misconceptions about CBDCs.

Central bank digital currency is . . .

- Traditional money, but in digital form;

- Issued and governed by a country’s central bank;

- Influenced in terms of supply and value by a country’s monetary policies, trade surpluses, and central bank; and

- Based on a digital ledger, and may or may not leverage blockchain or distributed ledger technology.

Central bank digital currency is not . . .

- Cryptocurrency (like Bitcoin) governed by distributed autonomous communities instead of a centralized body;

- Value-dependent and determined entirely by the market; or

- Equivalent to electronic cash (e.g., balance in a digital wallet or a prepaid card) with claim against an intermediary such as a commercial bank.

CBDCs are rapidly evolving, and different central banks can take different approaches in implementation. There are a number of design decisions that lack broad consensus, including the following:

- Ability of CBDCs to completely replace notes and coins

- Degree of anonymity or privacy

- Access and availability

- Interest-bearing ability

Overall, CBDCs would offer both a new form of central bank money and a paradigm change in payments infrastructure. That’s why it becomes important to understand the benefits of CBDCs and their impacts on the wider payments landscape.

For an exploration of policy and regulatory considerations for CBDCs, see Deloitte’s paper.

Central bank digital currencies: The next disruptor

Drivers of CBDCs

The need for CBDCs is driven by the rapid digitization of economies, push for real-time payments and settlement, and need for more efficient domestic and cross-border monetary interactions. According to the International Monetary Fund (IMF), centralized technology such as CBDCs can reduce expenses, facilitate seamless flow of money, improve financial inclusion, and provide safer access to money through digital channels. On the other hand, many central banks are also realizing the increasing influence of digital currencies and are concerned about potential impacts on the financial system.

We have identified the following four key drivers that have pushed central banks to explore CBDCs:

- Supporting digitization of economies

- Streamlining current payment systems

- Enhancing monetary and fiscal policy

- Improving financial inclusion

Overall, CBDCs would provide a more resilient payments landscape, supporting competition, efficiency, controls, and innovation in payments. They would also address declining cash usage by improving the usability and availability of legitimate central bank money.

Design considerations for CBDCs

Central banks around the globe are exploring variations in CBDC design while weighing factors such as access, privacy, and distribution method. There are two common design formats for CBDCs: token-based and account-based. Each approach has a different technical infrastructure, as well as varying levels of access and privacy.

Token-based CBDCs use a digital token, and access and claims require users to have knowledge of the token (public-private key pair). This approach typically offers a high degree of anonymity; however, central banks can choose to implement identity requirements to use the network. Token transfers rely on the sender’s ability to verify the validity of the payment object and therefore require a form of distributed ledger technology for verifying the chain of ownership in each token and validating payment transactions. This also means higher end-user risk of losing a key or token held in a noncustodial wallet.

In a token-based approach, commercial banks would need to be the first line of defense for compliance with know your customer (KYC) and anti-money laundering/combating the financing of terrorism (AML/CFT) regulations. This method can provide universal access to CBDCs but also makes law enforcement more challenging compared with other designs.

Account-based CBDC access and claims are linked to a bank account tied to the identity of the account holder. This method is challenging for universal access because it still requires a banking relationship. To transfer funds, banks would process each payment by debiting the sender’s CBDC account and crediting the beneficiary’s CBDC account. Transactions need to be verified using user identities, and therefore, robust identity management systems are required to maintain a unique identifier per individual across payment systems.

In an account-based approach, compliance with KYC and AML/CFT regulation is the responsibility of the central bank. Verification of transfers in an account-based system depends on establishing appropriate safeguards against identity theft, fraud, and unauthorized transfers from valid accounts.

There are many design considerations, including distribution, access, and privacy, that need to be carefully considered to determine the right CBDC implementation. Reviewing lessons learned from existing CBDC and crypto approaches, intended benefits, and trade-offs can help a central bank determine the best approach.

Current global landscape of CBDCs

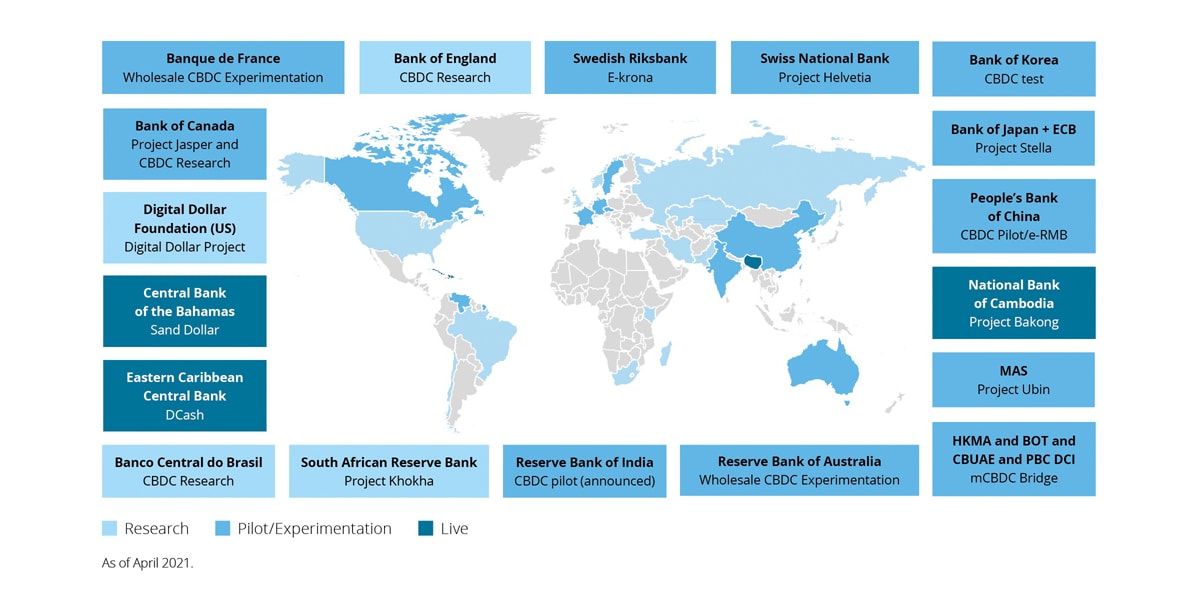

CBDCs aren’t just a theoretical concept; there are live CBDCs and many proofs of concept globally, as depicted in figure 1. Key highlights include:

- More than 60 central banks are exploring CBDCs at varying levels of maturity.

- Fourteen percent of central banks are moving forward to development and pilot arrangements.

- Three retail CBDC projects are live (Bahamas Sand Dollar, Bakong Cambodia, and Eastern Caribbean DCash).

Though countries like China, Sweden, Canada, and the United Kingdom have led research and pilot projects in the past few years, the actual execution of CBDC pilots is being led by smaller nations. In late 2020, the Central Bank of the Bahamas launched the Sand Dollar, a digital currency backed by that nation’s central bank. The Sand Dollar has facilitated easier monetary transactions across an otherwise vast archipelago. It’s also meant to improve ease of transaction, service delivery costs, and financial inclusion. The Bank started experimenting with CBDC in 2019.

Figure 1. Global CDBC landscape click to expand

Impact of CBDCs on commercial banks

Commercial banks are focused heavily on customer-facing operations, secure transactions, and regulatory reporting and are given CBDC design decisions, essential partners in successfully rolling out a CBDC. CBDCs introduce an electronic form of central bank money, adding significant complexity for commercial banks, and may imply a drastic change across the organization to keep up with the need to innovate compatible products.

As central banks embark on the digital currency journey with CBDCs, it could lead to a paradigm shift in the way domestic and global economies operate. While there’s a lot yet to be determined, the design of a CBDC will have implications for the entire financial ecosystem.

Depending on CBDC design, commercial banks will need to plan for changes in the following areas:

High-level scope of changes:

- Banks could innovate current products and services across portfolios to leverage and adjust to CBDC opportunities and behaviors.

- The rollout of a CBDC would generate large amounts of transaction data that can open opportunities for analysis and new real-time economic insights.

- If central banks go the way of account-based design, it will disintermediate correspondent banking networks, as central banks would directly provide liquidity in each market.

High-level scope of changes:

- Banks will need to maintain compliance with AML, KYC, and custodian-related regulation.

- Existing legal frameworks may be reformed based on CBDC design.

High-level scope of changes:

- Banks may need to adapt their infrastructure to process CBDC transactions; enhance digital apps to introduce CBDC functionality, leveraging existing processes; evolve customer interfaces; and enable open, compatible infrastructure or hardware.

- For cross-border, FX transactions, or multicurrency wallets, banks may also need to manage designs unique to individual CBDCs.

High-level scope of changes:

- Depending on the design decisions of a central bank, commercial banks may need to create real-time infrastructure for identity and access management.

High-level scope of changes:

- Customer privacy and data security are expected to become key concerns due to cybersecurity threats and vulnerabilities.

High-level scope of changes:

- Different accounting rules and audit and financial reporting requirements are expected for CBDC transactions.

High-level scope of changes:

- Organizations may need to develop training required to manage CBDC-related processes, technologies, and regulation.

Next steps

The introduction of CBDCs is a disruptor for the financial ecosystem, promoting payment efficiency and representing an additional alternative to the current money model from an operational and technological point of view. Central banks are moving rapidly toward implementation, and therefore, commercial banks should use this time to explore the digital currency landscape and reimagine it for emerging services, opportunity, and value creation.

Get in touch

Sohail Kagzi

|

Christopher Allen |

Recommendations

The use of cryptocurrency in business

Why companies should consider using cryptocurrency

Unleashing blockchain in finance

CFO insights