Insurance regulation and technology has been saved

Perspectives

Insurance regulation and technology

InFocus: Optimizing digital transformation in the insurance industry

While new insurance technology (InsurTech) and regulatory technology (RegTech) present risks and challenges for insurers, they are also enabling transformative shifts that signal a sea change in insurance compliance. Using RegTech to automate processes, compliance professionals can respond more effectively to changing regulatory demands, focus on higher-order activities, and become more valuable business partners and advisers.

Explore content

- Top takeaways

- What’s driving insurance RegTech’s growth?

- Key insights

- What should insurers know?

- Sea change in insurance compliance operations

- Potential insurance RegTech solutions

- How and where to invest?

- What's next?

- Get in touch

- Follow @DeloitteFinsvcs

Top takeaways

- Rapid technology advancements are transforming the insurance industry. Insurers’ regulatory compliance organizations are being challenged by the risks associated with insurance technology (InsurTech) advancements, as well as the opportunities to harness new regulatory technology (RegTech) capabilities.

- Drivers for modernizing the insurance compliance function are coming from three directions: Emerging RegTech technologies, internal cost challenges, and continual regulatory changes.

InFocus: Insurance regulation and technology

- By using RegTech to automate more costly human functions and do routine processes more intelligently and costeffectively, compliance professionals can respond to changing regulatory demands and focus on higher-order activities to become more valuable business partners and advisers.

- Within the next three to five years, we expect that insurance RegTech solutions using sophisticated analytics, data integration, robotic process automation, natural language generation/processing, artificial intelligence, and other emerging technologies will be positioned to produce a sea change in how insurance company compliance organizations operate.

Rapid advancements in technology are transforming the US insurance industry. Companies are embracing the use of advanced and predictive analytics, robotic process automation (RPA), artificial intelligence (AI), and cognitive technologies in their quest to improve business operations.

Insurers’ regulatory compliance organizations are being challenged by the risks associated with InsurTech advancements, as well as opportunities to harness new RegTech capabilities—to change their focus from hindsight to foresight and better align with business strategy in a drive toward greater efficiency and effectiveness.1

By using RegTech to automate routine processes—thereby potentially improving quality and reducing costs—compliance professionals can better respond to changing regulatory demands and apply analytics to advise business functions and determine areas of heightened regulatory risks, such as agent sales practices, rate and form filings, customer and third-party fraud, and business operations.

What’s driving insurance RegTech’s growth?

RegTech is designed to help firms automate the more routine compliance tasks and reduce operational risks associated with meeting compliance and reporting obligations. In the longer term, it should empower compliance functions to make informed risk choices based on data and provide insight

– Sean Smith, Risk Advisory partner at Deloitte Ireland

Drivers for modernizing the insurance compliance function are coming from multiple directions (see figure 1). Increasing regulatory mandates, perpetual talent squeezes, mounting demand for increased cost reductions, and a growing need for additional capacity for new and emerging risks and regulations are challenging insurance companies’ ability to respond in a timely and cost-effective manner.2

Figure 1: Drivers for modernizing compliance

Source: “Modernizing compliance: Enabling and moving with the speed of business,” Deloitte, 2017.

Insurance companies want to be more predictive and analytical in their compliance efforts—to be able to proactively evaluate risks and address issues before they become problems. This capability is important because many companies’ business functions are using

RegTech allows insurance company compliance professionals to work over and around legacy infrastructure impediments to connect and analyze information more smartly in order to understand where the organization may have risks and exposures based on a larger data population than was previously accessible. For example, insurers traditionally have used small sample file audits to identify potential distribution/sales channel issues or policy rating accuracy; this method consumed significant resources and addressed only a limited portion of the population. RegTech and analytics may help make the process more efficient because insurers can monitor an entire population and pinpoint areas that may be problematic.

Key insights: Insurance regulator technology adoption survey

The Deloitte Center for Financial Services sent its online Insurance regulator technology adoption survey6 to all 56 jurisdictions in the National Association of Insurance Commissioners in late August/early September 2017; 28 jurisdictions responded. The survey’s intent was to see what insurance regulators thought about regulatory technology, how they might use it, and how they saw insurers using it. Findings show:

- State insurance regulators expect their use of technology to increase, both to improve oversight of the market and to respond to market changes in an increasingly digital, tech-driven industry.

- Drivers include automating manual processes (77 percent); replacing and/or integrating legacy systems (69 percent); responding to changing regulatory demands (58 percent); reducing costs of operations (54 percent); responding to insurers’ increased use of technology (54 percent); and increasing speed and quality of oversight (42 percent).

- Regulators today use technology primarily to monitor insurer solvency and audit insurer financials, areas that require analyzing quantifiable and mostly formatted financial data. Going forward, regulators expect to ramp up technology use in market conduct-related areas such as investigating noncompliance and data manipulation, and in consumer education and response.

- More than one-half of the regulators surveyed felt that insurers’ use of technology could be a motivation for using the same technology to regulate them.

What should insurers know and do as they move forward with their RegTech plans?

How quickly and effectively insurers put RegTech solutions to work may be crucial to their future success as they seek to reduce costs, enhance efficiency and, ultimately, establish more robust compliance programs that withstand regulators’ evolving expectations.

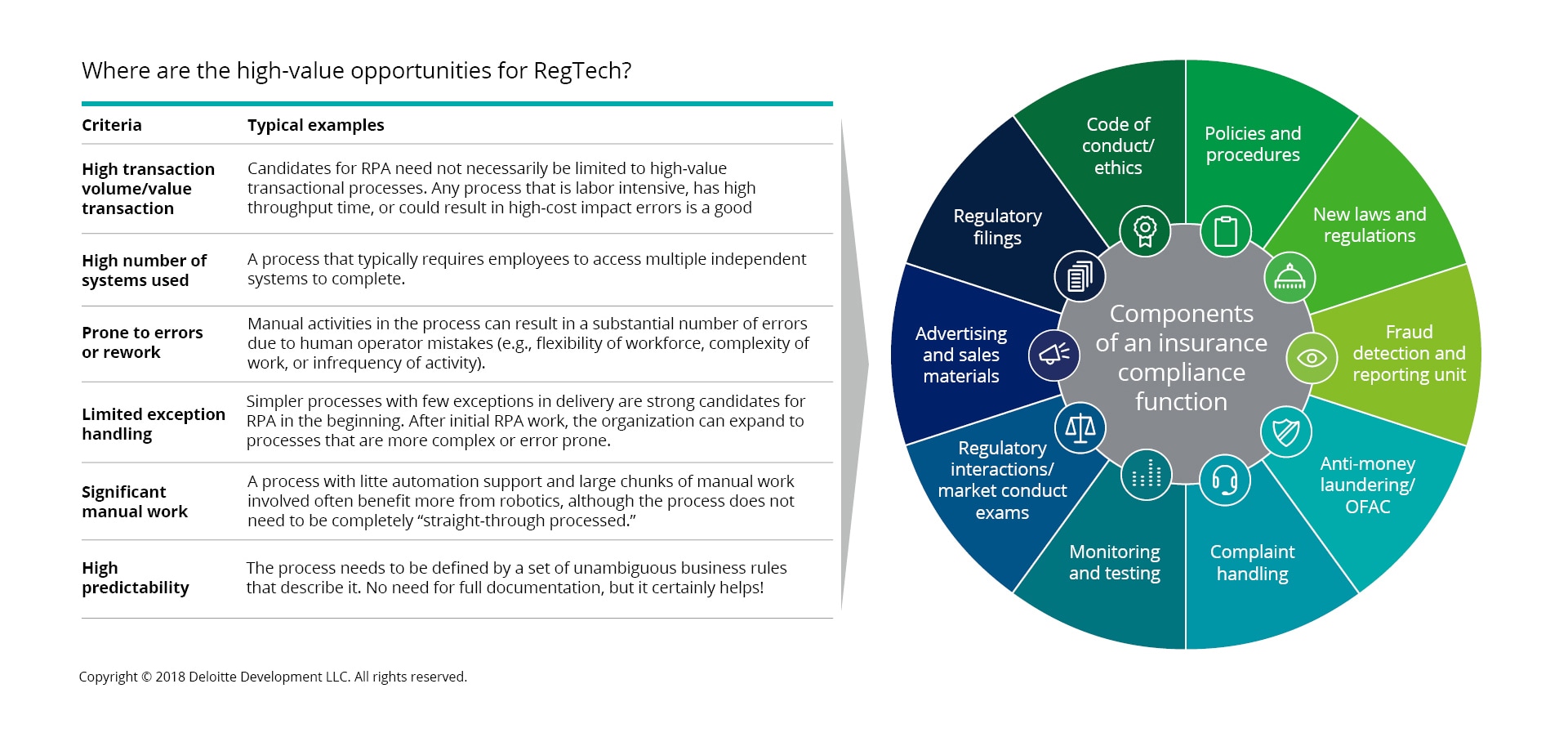

What should insurers know and do as they move forward with their RegTech plans? Looking across the typical components of an insurance compliance function reveals numerous, high-value opportunities for applying RegTech (see figure 2). Companies may want to begin with lower-cost, high-impact projects that can help bolster the business case for more expensive, long-term investments.

Figure 2. RegTech solutions: Adding value to a compliance function

Source: “Insurance regulation and technology: A rapid transformation underway?,” Deloitte, 2018.

Back to top

Sea change in insurance compliance operations

Within the next three to five years, we expect that insurance RegTech solutions using predictive analytics, data integration, RPA, natural language generation/processing, artificial intelligence, and other emerging technologies may produce a sea change in how insurance compliance organizations operate.

In addition to enabling improved compliance, insurance RegTech solutions can work in concert with other back-office systems to positively impact insurers’ broader business operations by helping to streamline the input, handling, processing, and completion of operational tasks supporting policyholders.

Even regulators think that insurers will benefit from RegTech technology. Seventy-six percent of respondents to Deloitte’s survey cite increased operational effectiveness and 71 percent expect increased efficiency for the overall market as likely results.

Potential insurance RegTech solutions

- Audio monitoring solutions—Audio monitoring can be enhanced using audio processing, analytics engines, and dashboard reporting to gain greater insights into audio data (e.g., call center operations, outbound sales calls, transactions with seniors).

- Regulatory reporting—RPA can be used to prepare regulatory reports (e.g., market conduct annual statements, data calls, etc.).

- Sales surveillance—RPA can be used to automate surveillance and identify noncompliance instances (e.g., insurance replacement transactions, anti-money laundering, etc.).

- Regulatory extraction—Natural Language Processing (NLP) can be used to extract regulations and identify regulatory and control requirements.

- Compliance testing aggregation—RPA, analytics, and integrated data repositories can be combined to provide an enterprise-level view of compliance risk and testing.

- Anti-money laundering (AML)—Natural Language Generation (NLG) can be used to automate the generation of regulatory AML reports (e.g., suspicious activity reports).

- Policy and procedure mapping—NLP can be used to perform

mapping between policies and procedures and regulatory requirements. - Advanced analytics—Predictive models and data visualization can be used to analyze rate and forms, sales practices, compliance and ethics culture, and occurrences of fraud (internal and external).

- GRC solutions—Shared risk and compliance language can help enhance risk portfolio and risk treatments.

- Blab*—Social intelligence platform can use statistical analysis to forecast volume and velocity of social conversations to sense emerging and reputational risks.

- State rate accuracy tool*—Rating engine technology combined with advanced analytics can determine if your charged rates equal your filed and approved rates.

*Deloitte proprietary solution

How and where to invest?

Most insurance companies planning to use technology to modernize their compliance process are proceeding with caution as they consider how and where to invest to attain

- Which compliance functions are candidates for automation, as ranked by value measures (time savings, capacity enhancements, error resolution, efficiency gains) and complexity measures (scope, size, variability)?

- Does our company have the right operating model to move to a more analytics-driven and predictive focus

with our compliance effort? - Do we have the right people to develop and lead a technology-driven approach to compliance? Do we need external assistance?

- Should we develop or acquire the capabilities we need?

- How do we create the RegTech business case to drive greater executive and organizational buy-in?

- How do we stay abreast of the ways that regulators and peer companies are deploying advanced technologies and data analytics so we don’t fall behind?

What’s next?

Insurance companies’ regulatory compliance functions have an opportunity to better align with business strategy in a drive toward efficiency and effectiveness. Organizations should consider the numerous, high-value opportunities RegTech provides to improve compliance and support broader operational efficiencies.

If you want to learn about how and where your organization can employ RegTech solutions, we should talk.

Explore additional financial services perspectives in the InFocus series

Staying on top of new financial services industry trends, emerging technologies, and changing regulations isn’t easy—it’s not enough to rely on the headlines to understand the complete picture. Our InFocus series takes a deeper dive into the issues that affect financial services organizations and gives you the insights needed to make more informed decisions.

Endnotes

1 “Modernizing compliance: Enabling and moving with the speed of business,” Deloitte, 2017.

2 Ibid.

3 “Insurance regulators in an era of advanced technologies: Challenges and opportunities in oversight,” Deloitte Center for Financial Services, 2018.

4 https://www2.deloitte.com/insights/us/en/industry/insurance/advanced-technologies-insurance-regulators-challenges-opportunities.html.

5 https://www.naic.org/state_ahead.html.

6 https://www2.deloitte.com/insights/us/en/industry/insurance/advanced-technolo-

* Deloitte proprietary solution.

Recommendations

Shaping the future of payments

Trends and insights for 2025

Alternative data adoption in investing and finance

InFocus: Collective intelligence investing creates new rewards and risks

Latest news from @DeloitteFinSvcs

Sharing insights, events, research, and more