Modernizing transaction banking has been saved

Analysis

Modernizing transaction banking

Service externalization and the right technology portfolio

Regulatory burdens, disruptive technologies, changing customer expectations, and innovative banking competitors are signs that the industry needs to modernize transaction banking. Service externalization and the right mix of technology can help banks retain transaction banking profits and empower customers.

Explore content

- Modernizing transaction banking

- A profitable business, under threat

- Don't just automate, eliminate: Service externalization

- Service externalization: The rewards

- The new transaction banking: Five guidelines

- Conclusion: Are you ready for service externalization?

- Delivering client value in transaction banking

- Get in touch

- Join the conversation

Service externalization in transaction banking

Transaction banking1 has for years been a reliable, stable source of revenues (figure 1). But regulatory expectations, disruptive technologies, changing customer expectations, and the rise of new competitors are potential signs that the industry may need to modernize with a greater sense of urgency.

A more modern, agile, and profitable transaction banking business likely won’t come about by simply automating existing processes. Instead, banks should seize a new opportunity to rethink how work is done and empower clients to gain more control of service delivery. This new model, which we call service externalization, enables customers to fill many of their needs exactly how and when they want to.

Service externalization has four components, which together can form a potentially powerful portfolio of innovations:

- A digital front end designed for maximum user-friendliness and efficacy

- A core infrastructure built for agility and resilience

- Cognitive technologies for intelligent automation and scalability

- APIs (application programming interfaces) to expand banks’ strong connections with the ecosystem

These four components often work best when implemented together, not in silos or increments. A digital front end needs cognitive technologies to meet customers’ needs; it should connect with APIs to customers, counterparties, and vendors for speed and responsiveness; and it typically needs a robust backend to support these technologies and the performance that customers demand.

This modernized transaction banking infrastructure may not only increase customer satisfaction but also create a new competitive advantage. And since customers will likely own many processes that banks currently do internally, banks’ costs and risks may fall. This paradigm could also work with counterparties and vendors.

This paper will look at the challenges in the transaction banking space, explore the approach that can empower banks to overcome these challenges, and offer examples of success.

A profitable business, under threat

It’s been said that no good thing can last forever. Most banks have enjoyed resilient revenues from transaction banking, as figure 1 shows, but they shouldn’t rest on their laurels. Here are some of the challenges that many

- The regulatory climate. The pendulum in the US is swinging toward a lighter touch, but requirements persist in know your customer (KYC), anti-money laundering (AML), the European Market Infrastructure Regulation (EMIR), single euro payments area (SEPA), Basel III and the Foreign Account Tax Compliance Act (FATCA), among other areas. Nearly 45 percent of corporate banking respondents consider meeting regulatory demands as one of the top three business challenges, according to 2016 Ovum ICT Enterprise Insights data.

- Infrastructure is often outdated and poorly integrated. Manual processes, siloed systems, batch-based processing, and other obsolete infrastructure can perpetuate inefficiencies. Many banks spend enormous resources on additional controls and on remediating errors through rekeying and queries. This old technology also often inhibits the real-time, holistic view of clients and transactions that

is so valuable to banks. - Too many clients barely worth the cost. The Pareto Principle, also known as the 80/20 Rule wherein 20 percent of the invested input yields 80 percent of the output, applies: a small number of clients produce most of the revenue.3 For the rest, costs and the need for risk management often eat up a large chunk of profit. Efforts to “de-risk” the customer base mostly haven’t gone far enough.

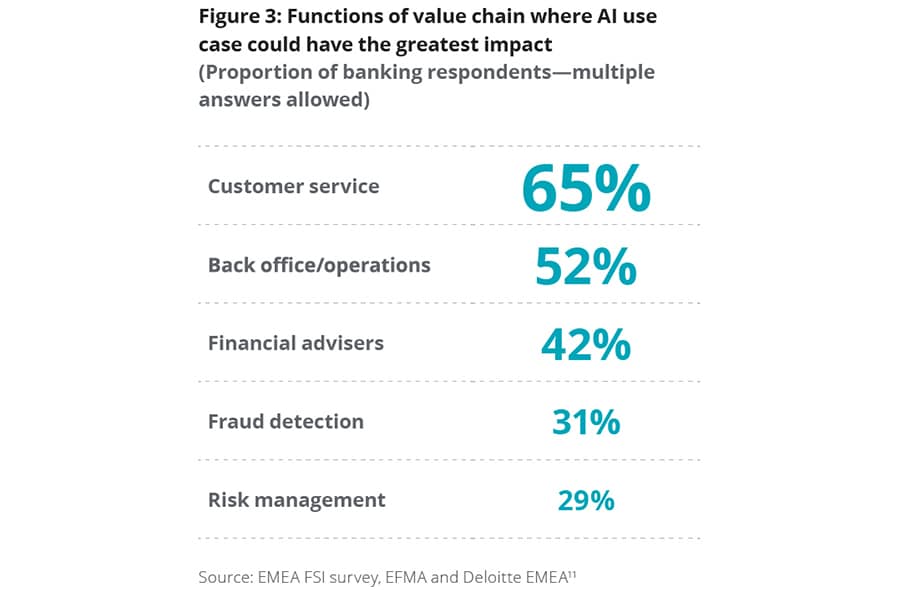

- Digital clients typically expect digital bankers. Transaction banking clients are increasingly sophisticated. Corporate treasurers, for example, often use customer analytics (360-degree counterparty analysis) and automated fraud management. Supply chains are digitizing using blockchain and the Internet of Things (IoT). Yet many banks are still shuffling pieces of paper around. Improving the customer experience was one of the top three challenges for 38 percent of corporate banking respondents, according to the 2016 Ovum ICT Enterprise Insights.

- New threats seem to be rising. Many fintech firms and nonfinancial companies are competing with banks more fiercely. Shipping company Maersk, for example, has begun to offer trade finance solutions to its customers. Maersk doesn’t need to ask for collateral (the shipped goods are already in its possession) and it often already has extensive data on borrowers and buyers.4 Banks appear to be taking note of this new competitive pressure. Corporate banks consider innovation, in the form of new services and payments platforms, as the strongest factor influencing payments in the long term, according to the 2016 Ovum ICT Enterprise Insights survey.

Transaction banking businesses should go beyond incremental automation and suboptimal technology upgrades to keep their competitive edge. By using the service externalization model to reimagine how work is done, they can operate at a lower cost while also enhancing the customer experience.

This model, which has little in common with traditional outsourcing, requires the right technology portfolio—a modern core infrastructure augmented with new technologies—to be truly effective.

Don't just automate, eliminate: service externalization

Most transaction banks do enormous work to complete even simple transactions. Think of all the keystrokes, queries, back and forths, and do-overs that a routine payment file requires. Think of the resources reconciliation demands. And think of these inefficiencies’ consequences for timely, accurate information. When delays in accessing accurate information are great enough, they can do more than

A part of the answer may lie in service externalization. It’s a different approach from traditional outsourcing, much as outsourcing will likely continue to play a useful role in many organizations.

Service externalization isn’t about having a third-party perform the activities for the organization. On the contrary, it’s about providing customers with a digital experience that empowers them to get what they want, how they want it, and when they want it. In the process, they won’t just enjoy quick, customized service—they’ll also own much of the work that banks currently do in-house.

Service externalization means that banks aren’t simply streamlining and automating work. They’re often eliminating it altogether. The four components

1. A digital front end

What they want, how they want

Service externalization typically requires a highly user-friendly digital front end, where customers are able to request, customize, and deploy the services they need, quickly and easily. HSBC, for example, has partnered with Tradeshift to create an “integrated proposition” with which buyers would be able to digitize procurement, accounts payable, supply chain financing, and settlement.5 The platform would help customers digitize their manual and paper-intensive supply chain processes, manage supply chain financing, and reduce costs through electronic invoicing. One key part of this solution is a digital front end—“one simple online platform”—that would foster transparency and real-time collaboration between buyers and suppliers.

So how do banks develop a digital front end? Banks should consider these measures:

- Examine the processes involved, from start to finish, in a particular activity.

- Differentiate processes that rely on core strengths from those that customers (and other partners such as vendors and counterparties) can do themselves.

- Determine advantages (such as convenience, speed, reliability, and customizability) that customers and vendors would gain if they performed these activities themselves.

- Identify the tools, data, and capabilities needed to enable this transformation.

- Plan for the impacts on related processes, security, and regulatory compliance.

- Consult customers on how to make the digital front-end work best for them.

This last part is very important. Successful service externalization implies giving customers what they want, though (for example) auto-filled fields, reminders of due dates, customized reports, and real-time tracking.

2. A modern core

Strengthening the back end for agility and resilience

Many transaction banking units appear behind the technology curve. Corporate customers accustomed to payment transactions through systems such as FedWire seem increasingly disgruntled at having to wait days for cross-border payments. Many banks use memo-posting in batch-processing systems to give the illusion of real-time processing, but this method has its limits in the digital age.

Core systems transformation (CST) can be expensive, but with challenges rising, the failure to act may cost even more.

And without a modern core, service externalization may have limited impact. A transaction bank’s digital front end needs a backend that can give customers a quick, convenient experience with all functions, from data gathering to payment processing to reconciliation. Some banks are already prioritizing a core upgrade: nearly a quarter of corporate banking respondents to the 2016 Ovum ICT Enterprise Insights survey considered modernizing legacy systems the most important IT trend for their organization for the year.

Multiple approaches are available for transforming or modernizing core systems, ranging from retooling existing systems to replacing or retiring them altogether (figure 2). The choice of approach should start with understanding the different solutions’ business and technology value. Banks may also adopt a mix of approaches to complete their core systems transformation, rather than trying for a single approach to success.

![]()

Modernizing the core requires preparation since so many other systems and applications connect to it. To do it successfully, banks should consider the following:

- Map out the data flowing into and out of the core, where it comes from upstream and where it goes downstream.

- Catalog the existing applications that the core touches, including treasury and liquidity, credit, and payments.

- Examine clients’ and counterparties’ impact from the chosen approach to core systems transformation—which of their data and activities the core modernization could affect.

- Prepare for regulatory compliance on a revised core system.

And of course, the new core has to be flexible and scalable, able to power the latest set of cognitive technologies and analytics.

3. Cognitive technologies

Enabling smarter decisions

Cognitive technologies use statistical models that constantly improve as the system “learns” and extracts more relevant, timely, and granular insights from massive pools of data.7 Applications of these technologies and artificial intelligence (AI) typically fall into three categories:8

- Cognitive engagement: Applications such as chatbots use cognitive technology to interact with customers in a personalized manner in natural language.

- Cognitive insights: Cognitive technologies accomplish “offense” functions, such as revenue generation. In addition, these technologies support “defense” functions, including fraud prevention, risk management, and AML compliance (e.g. natural language generation technologies that produce AML-suspicious activity reports).9

- Cognitive automation: By generating “digital breadcrumbs” that train precise statistical models, machine learning products can automate tasks that previously required human expertise.10

Unfortunately, in transaction banking, many of these efforts are run in silos, often with little regard for a “sum of the parts” vision that includes possible synergies from the integration of different automation efforts.

But when well-integrated and powered by a modern core, these smart systems can bring service externalization to a new level. For example, cognitive technologies can decide on the right content to push to the right partners, whether customers, counterparties, or vendors. They can look for errors and flag or resolve them. Natural language generation software can also analyze the data and present the results in plain English.

Smart robots like these, powered by a modern core, can make the digital front end responsive and speedy—if it’s also connected through APIs.

4. APIs

Stronger connections with the ecosystem

Many banks have used APIs for years to enable internal systems to “talk” to each other and share information.12 But now many banks are increasingly sharing and integrating APIs externally with systems of clients, vendors, and other stakeholders.

Citibank, for example, recently launched APIs for its treasury clients to link their respective treasury workstations and systems with those of the bank.13 Such API-based integration can improve corporate clients’ experience and provide them with the flexibility to access the bank’s services as needed.

The push to real-time or faster payments may also be a driver for sharing or launching more APIs.14 And, of course, banks could use APIs to transform their intra-day reporting to real-time reporting of cash positions for their clients—one of the biggest pain points for corporate treasurers.15 According to the 2016 Ovum ICT Enterprise Insights, 34 percent of corporate banking respondents prioritized cash visibility and forecasting services as the top IT project in cash and treasury management over the next 18 months.

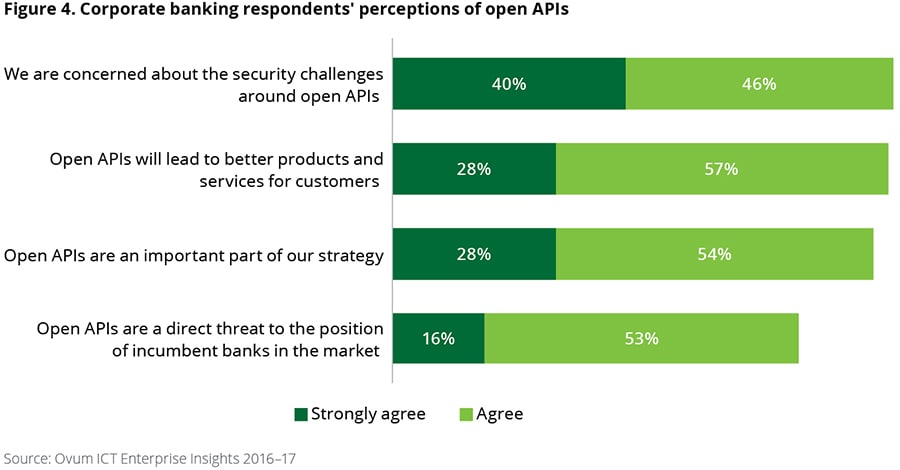

Many banks are also sharing information through open APIs, which enable external developers to build applications around the information and services. Open APIs can help further service externalization’s objective of maximizing clients’ ability to get the exact services they want, when and how they want them. Standard Chartered, for example, recently opened its Banking API Portal for developers to create new solutions for its corporate clients, with a focus on transaction banking and cash management.16

Regulatory developments also seem to be driving the adoption of open APIs. In Europe, the Revised Payments Services Directive (PSD2) mandates banks to open APIs to third-party applications, such as those facilitating payments.17 In Singapore, the Association of Banks has launched a “Finance-as-a-Service: API Playbook” to guide financial institutions, fintech players, and other stakeholders to develop and implement open API-based architectures.18 Australian officials are also encouraging open APIs.19

Yet corporate banks appear concerned about how open APIs might impact data and systems security (figure 4). The response to these concerns does not have to be to resist open APIs; it could be to deploy a resilient risk management mechanism. Banks should start looking more closely at data formats, security formats, issue resolution protocols, common risk factors, indemnification protocols, common standards (or the lack thereof), identity access management, and permissioning, among other factors.

Service externalization is about providing customers with a digital experience that empowers them to get what they want, how they want it, and when they want it.

Service externalization in action in payment processing

An international bank had a familiar problem: processing payment files was time-consuming and costly. It had different formats that were prone to different errors, and it had multiple channels rerouted through internal systems, creating further complications. On a typical day, the bank received hundreds of payment instructions from clients, usually in a random fashion. The bank then reviewed the error-prone data, mostly manually, and entered it into its payments processing platform. Error identification was often delayed, and whenever the data for a particular client had errors, the bank usually had to manually intervene and stop the process for all batches for all clients. For most errors, the client had to be contacted, often manually. Frequently the bank then had to reissue the payment instructions. Multiple back-and-forths ensued, demanding manpower and other resources.

The overall result was high costs, frequent delays, and a broken user experience.

After implementing service externalization, here’s how the bank’s clients became more engaged in the service delivery process:

- Clients upload payment files through an API into the bank’s platform through a portal, enabling the client to review transactions in real time.

- Cognitive technologies instantly check for errors, notify the client, and offer options for resolution—all through APIs.

- The client chooses from among the resolution options, issues instructions through an API, and owns the choices.

- The front end provides clients with the data and cognitive-technology-powered tools to perform reconciliation.

- When reconciliation is complete, the client receives a customized report, which cognitive technologies help produce using historical patterns and templates.

- The entire process is usually complete within minutes.

The results are lower costs and clients who receive faster, more streamlined, and personalized service while assuming risks that the bank previously had.

Blockchain in trade finance

Take trade finance, for example. The Digital Trade Chain (DTC) initiative, a collaborative venture among seven European banks that began in January 2017, aims to digitize the trade finance process for small and medium-sized enterprises (SME).20

DTC uses blockchain to record a trade finance transaction, eliminating the need for paper-based documentation. With each bank bringing its pool of SME clients, who have already gone through KYC documentation and AML checks, the collaboration aids in building “trust” between counterparties, thus addressing one of the most important challenges for SMEs when transacting across borders.

SME executives and treasurers can access the DTC app on their smartphones and tablets. The app enables them to track the progress of trade flows (goods) and financing.

The launch of this app, scheduled for late 2017, should both mitigate risk and expand trade. Blockchain, with its immutable nature, facilitates tracking clear titles of ownership. And blockchain, combined with other technologies such as the Internet of Things and GPS, could help verify how goods match contractual requirements. For instance, should damage to goods occur, these technologies can help ascertain what caused the damage and when it occurred.

Service externalization: The rewards

- Lower operating costs. Banks would no longer face endless keying in, queries, reconciliation troubles, and other issues. With service externalization, a transaction bank’s customers perform these tasks while the bank’s platform confirms, collects, monitors, and analyzes data. This efficiency can make even low-revenue clients profitable.

- Greater customer satisfaction. Customers can get the speed, data, reliability, reports, customization, and integration with their own systems that they demand.

- Reduced risk. The digital system could eliminate many errors and identify others quickly. Clients would now be responsible for many activities that previously created risks for banks.

- Easier regulatory compliance. With so much information on the bank’s digital platform, complying with regulatory requirements would become more cost-effective. It may in the future be possible to open the platform for regulators to use.

As the examples show, service externalization could offer significant benefits.

The new transaction banking: Five guidelines

Nothing can typically replace a thorough analysis of an organization’s technologies, processes, human resources, competitive context, regulatory burdens, and consumer needs, but the following five guidelines can be a good start to consider:

- Organize for the big picture. Too many banks often miss synergies because they lack a holistic view. Testing technology proofs-of-concept in silos or increments may limit their full potential. Banks should also consider how best to sequence, staff, and deploy new technologies.

- Don’t just automate work, rethink and eliminate it. Identify core strengths and which processes a bank should empower customers, counterparties, and vendors to perform.

- Keep the customer journey front and center. The goal is

typically to give customers what they want, how theywant, when they want it. Failing to consult with customers while building the new system may risk replicating their current frustrations. - Partner with the fintech ecosystem. Whether through open APIs or formal agreements, take advantage of others’ innovations. Consider structuring partnerships to prevent disintermediation and manage risks to performance, reputation, and compliance.

- Refine enterprise data management capabilities. Understanding and using current data flows is key to creating and transitioning to this new operating model. Banks should upgrade abilities to gather and analyze data.

Modernizing transaction banking infrastructure may be a big investment, but if done right it doesn’t have to be daunting.

Conclusion: Are you ready for service externalization?

Service externalization is a new construct that will likely require investment and a new way of thinking. But done right and with a focus on the customer, the rewards can be substantial. Before beginning this journey, consider these questions:

- Do you have a plan to identify which processes are suited for externalization and which are core strengths that should remain in-house?

- Do you have a roadmap for modernizing your technology infrastructure that puts the customer experience journey front and center?

- Are you able to develop the necessary technology portfolio—a digital front end, new core systems, cognitive technologies, and APIs—together, not in silos and increments?

- Does your organization have the right skills and structures for this portfolio?

If the answer to any of these questions is no, then it could be time for a strategic look at how service externalization and the right portfolio of technologies can give a transaction bank a competitive edge, now and into the future.

Discover more:

Delivering client value in transaction banking: Re-setting the price-value

How can transaction banking leaders adapt to the "new normal" by reexamining the ways in which value is delivered to corporate clients, better understanding the cost of serving them and building a clearer picture of the profitability of these relationships?

1 Please note that transaction banking, as used in this paper, includes activities such as cash management, treasury services, trade finance, corporate payments, custody, and securities services.

2 This analysis is based on the Coalition Transaction Banking & Lending Index, which tracks the performance of the 10 largest banks globally. For more information, please see the Coalition website (www.coalition.com).

3 Dave Lavinsky, “Pareto Principle: How To Use It To Dramatically Grow Your Business,” Forbes, January 20, 2014.

4 Aleya Begum, “Maersk sails into trade finance world,” Global Trade Review, June 14, 2017.

5 HSBC, “HSBC and Tradeshift Join Forces to Revolutionise Working Capital Financing,” press release, March 30, 2017.

6 “Legacy Systems and Modernization: Core Systems Strategy for Policy Administration Systems,” Deloitte Consulting LLP and LIMRA, June 16, 2017, https://www2.deloitte.com/content/dam/Deloitte/us/Documents/financial-services/us-fsi-legacy-systems-and-modernization.pdf.

7 “Data’s Big Leap: Cognitive Computing is Poised to Extend the Capabilities of People and Organizations,” Deloitte.

8 “AI and You: Perceptions of Artificial Intelligence from the EMEA Financial Services Industry,” Deloitte and EFMA, April 2017.

9 Tom Davenport and Dilip Krishna, “The Changing World of Technology in Financial Services,” Deloitte Insights, January 27, 2017, https://dupress.deloitte.com/dup-us-en/topics/analytics/analytical-cognitive-technology-in-financial-services.html.

10 Ibid.

11 “AI and You: Perceptions of Artificial Intelligence from the EMEA Financial Services Industry,” Deloitte and EFMA, April 2017.

12Susan Kelly, “A Bridge to More Bank Data,” Treasury and Risk, April 12, 2017.

13 “In Corporate Treasury, Apps are Out, APIs are In,” PYMNTS.com, March 21, 2017.

14 Susan Kelly, “A Bridge to More Bank Data,” Treasury and Risk, April 12, 2017.

15 “Understanding Today’s Corporate Treasurer: The Implications for Corporate Banking Services,” Ovum and Temenos, September 20, 2016, https://www.temenos.com/en/market-insight/2016/understanding-todays-corporate-treasurer/.

16 “In Corporate Treasury, Apps are Out, APIs are In,” PYMNTS.com, March 21, 2017.

17 Maikki Frisk, “PSD2 & Open Banking: The Perfect Marriage of Technology and Regulation,” Finextra (blog), September 1, 2017.

18 Association of Banks in Singapore, “The Association of Banks in Singapore Issues Finance-as-a-Service: API Playbook,” press release, November 16, 2016.

19 James Eyers, “Bank Inquiry Report: Banks Told to Share Data by Mid-2018,” Australian Financial Review, November 24, 2016, http://www.afr.com/technology/banks-told-to-build-apis-for-data-sharing-by-mid2018-20161124-gswno6.

20 Peter Lee, “Seven-bank Consortium to Deliver Trade Finance on Blockchain This Year,” Euromoney, February 6, 2017, https://www.euromoney.com/article/b12khnzj8hr504/seven-bank-consortium-to-deliver-trade-finance-on-blockchain-this-year.

Get in touch

Jim Eckenrode

Center for Financial Services leader | Managing Director | Deloitte Services LP

Val Srinivas

Senior research leader, banking & capital markets

Explore content

- Modernizing transaction banking

- A profitable business, under threat

- Don't just automate, eliminate: Service externalization

- Service externalization: The rewards

- The new transaction banking: Five guidelines

- Conclusion: Are you ready for service externalization?

- Delivering client value in transaction banking

- Get in touch

- Join the conversation

Recommendations

Patterns of disruption: Impact on wholesale banking

Can banks succeed within The Big Shift?

2020 Banking Industry Outlook

Optimism for banking and capital markets