Opening banking through architecture re-engineering has been saved

Perspectives

Opening banking through architecture re-engineering

The next frontier in digital banking

As the banking industry shifts towards digitization, the banking experience and operating model are aligning more with other industries and consumer expectations than ever before. Enter platform banking, a technology-enabled fusion of traditional and digital banking, fintech, and third parties that flips the traditional banking model into a customer-centric one. Here, we share our perspective on microservices-based banking architecture and how banks, through a deliberate approach, can open up to explore opportunities presented by the platform banking phenomenon.

Explore content

- Platform banking initiative

- Open banking versus platform banking

- Traditional versus platform banking

- Microservices-based architecture

- Embarking on the platform banking journey

Platform banking initiative

With a more mature digital foundation established, banks are now entering the next frontier: a more open and marketplace-based approach to offering and distributing products and services to customers. Platform banking transforms the traditional banking model into a customer-centric one that offers a marketplace of financial products and services sourced from multiple and independent institutions.

Before diving deeper into how platform banking can transform banking business models, it is important to understand the distinction between open banking and platform banking. A recently published paper by Deloitte, “Executing the open banking strategy in the United States,”1 provides a definition of open banking vs. platform banking and helps banks develop a strategy for moving to the new model.

Open banking versus platform banking

Open banking is when a bank, upon a customer’s request, shares customer data with third parties via APIs. 2Open banking does not use other, less secure methods of data-sharing, such as screen scraping, CSV3 files, or OCR-readable4 statements. There are two types of open APIs: read access, which only gives access to account information, and write access, which enables payments. Open banking can be mandated through government regulations, as it is in the United Kingdom and European Union Second Payment Services Directive (PSD2), or its adoption can be industry-driven, as is the case now in the United States. Open banking is built on the premise that customers own the data they generate and have the right to direct banks to share their data with others they trust. While it was designed to give customers more choice, open banking may end up making customers better understand and appreciate the value of one of their key assets: their data.

Platform banking, in contrast, is a digital marketplace, owned and operated by a bank or other third party, that provides banking and nonbanking services. As with open banking, sharing of customer data happens only with customer consent. Moreover, platform banking also requires secure data transmission via APIs. The premise behind platform banking is that banks can serve customers better, engender more trust, and retain the customer relationship. Open banking enables and amplifies platform banking.

Traditional versus platform banking

A host of factors and trends are driving banking towards platform banking. In order to prepare and exploit opportunities presented by platform banking, banks will have to review near-term and long-term business goals and determine the optimal platform banking strategy. Based on business, organizational, and technology maturity and goals, banks will gravitate to one of three platform strategies:

- Marketplace owner

- Marketplace partner

- Utility provider

Each strategy requires varying degrees of investment and will have varying degrees of transformative impact.

Banks may be best served to pursue either a marketplace owner or marketplace partner role in the new ecosystem; becoming a utility provider is not likely a viable business model, as it relegates banks to a mere service provider with low margins and no control over the customer relationship.

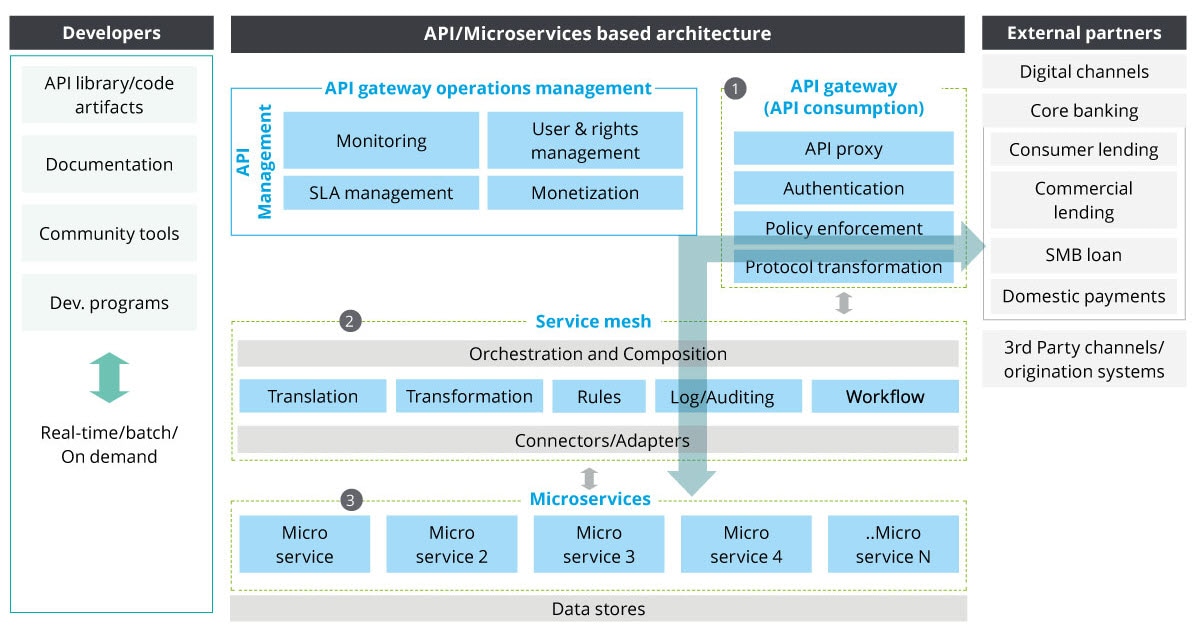

Microservices-based architecture: Foundation for platform banking

For most banks, successful adoption of platform banking standards will require substantial reengineering of current core banking application architecture and infrastructure. It will also call for an enterprise-wide transition toward microservices-based architecture. A microservices-based architecture allows efficient and accelerated integration with third parties, which can become the chief competitive differentiator in the platform banking ecosystem.

The current core banking architecture of a bank will have a significant bearing on the approach and level of technology transformation required to support either of the platform banking business models.

- Banks with legacy core banking architectures, monolithic applications with multiple point-to-point integrations and batch processing, can transform in a phased manner, while minimizing risk, through a deliberate approach with near-term and long-term objectives.

- Banks with modern cores, typically with service-oriented and mature API-based architectures, can transform through a big-bank approach owing to their mature IT organizations.

Regardless of the starting point for a bank from a technology perspective, building a microservices-based architecture is a critical enabler for platform banking because it allows greater integration flexibility and enables rapid delivery and consumption of new services.

Embarking on the platform banking journey

As is always the case with large-scale technology transformation initiatives, transitioning to a true microservices-based architecture requires significant investment, in both resources and time. The journey to platform banking and a microservices-based architecture involves two key steps to determine business and product strategy and technology readiness.

Based on the business model, product and services roadmap, and technology readiness, banks can initiate their platform banking journey through a phased approach with near-term and long-term goals. Banks with a forward-looking product roadmap, mature application architecture, and scalable technology infrastructure can fast-forward to a long-term goal of standing up a microservices-based architecture all at once.

Kick off the transition to platform banking now

The path to platform banking, while challenging, offers banks the ability to create and enter new markets, and establish new business models to enable growth. Assuming a lead or active role in a platform banking world will not only create new sources of revenue, but also enhance customer experience and improve operational efficiency.

With platform banking a matter of 'when' and not 'if', banks need to get started today. The phased approach recommended in this paper, one that considers a bank's current technical environment and its desired future environment, allows banks to lay the groundwork in a manageable, yet meaningful, way.

Get in touch

Kevin W. Laughridge |

Ketan Bhole |

Ram Nareddy |

Recommendations

2020 Banking Industry Outlook

Optimism for banking and capital markets