Tokenization in financial services: Embracing a new ecosystem has been saved

Perspectives

Tokenization in financial services: Embracing a new ecosystem

The benefits and challenges of tokenization

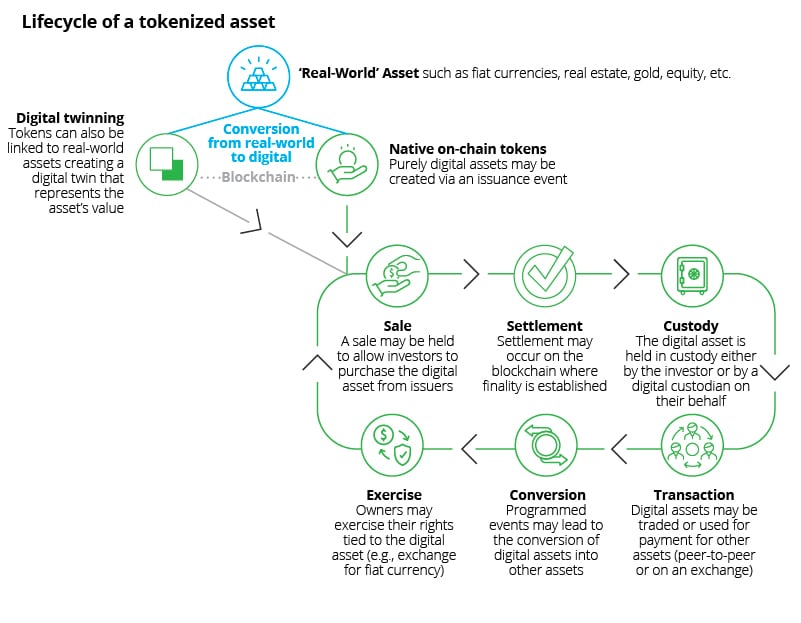

A growing number of leaders are extolling the opportunities of tokenization in financial services. Its basics are relatively simple: the linking of financial assets to digital tokens traded on distributed ledgers, including blockchains, whereby the tokens reflect the fair value of the underlying assets. While the challenges of tokenization are complex, the benefits of tokenization promise to be transformative.

Looking into a tokenized future

Various financial services providers are projecting that tokenization in financial services could generate trillions of dollars in new value this decade. And while these estimates may elicit skepticism among some, they would likely represent just a tiny fraction of the global market of assets that has the potential of being tokenized. Think of the many sectors with assets that have that possibility: real estate, private equity and venture capital funds, exchange-traded products, and many others.

Tokenization: Realizing the vision of a future financial ecosystem

The foundations of a tokenized future are already in the works. Several financial institutions have launched proofs of concept (PoCs) and have joined industry consortia that are dedicated to developing rigorous cross-industry standards, practices, and solutions to explore the benefits of tokenizatio

Source: Deloitte

So, what are the benefits of tokenization in financial services?

- The introduction of new financial products and services would be possible thanks to the digital representation of conventional assets that traditionally have been illiquid; or through the creation of new digital assets represented as tokens, such as nonfungible tokens (NFTs).

- Tokenization is likely to help reach new customers thanks to its ability to allow for fractional trading in illiquid assets. These assets might include real estate, artwork, or other valued collectibles. Moreover, tokenization could allow investors themselves to gain access to markets previously closed to them.

- Tokenization offers the possibility of new operational efficiencies. That’s because the process would in all likelihood be anchored to a ledger that facilitates smart contracts. These in turn serve to automate and streamline the trading of the underlying assets and facilitate the flows of programmable funds. Furthermore, tokenization could support improvements to the legacy infrastructure of financial services companies.

What early adopters are up against

The path to commercialization and the realization of near-term value may not be easy for early adopters. For some of their challenges, there are already indications that solutions may be at hand. For other challenges, these early adopters should collaborate with more traditional financial institutions, technology vendors, and regulators to unlock the value that they anticipate. Let’s explore five of the main challenges of tokenization early adopters are likely to face.

So far, major financial services institutions experimenting with tokenization have been testing on their own permissioned platforms that provide them with a safe space to play out use cases knowing they have complete control from administrative, security, and compliance perspectives. As a consequence, they have been able to avoid many of the challenges they might well face outside of their own carefully controlled platforms.

Yet, to unlock and maximize the potential of these tokenization in financial services use cases, these institutions should go outside their walls and cultivate vibrant secondary markets that trade in tokens. To create those secondary markets, interested institutions should connect their separate environments by relying on shared technical standards for interoperability. While interoperability standards do not yet exist, efforts to achieve it are in progress, and institutions should continue to participate in order to create the needed infrastructure and standards.

Explore the challenges and obstacles that lie ahead on the road to interoperability

While interoperability and secondary markets are important, as we noted earlier, institutions have limited their tokenization efforts to their own permissioned environments so far—and that is for a good reason. Across technology, operations, strategy, tax and accounting, and regulatory compliance, tokenization in financial services introduces a broad range of new risks.

Risks associated with regulatory compliance are likely the largest obstacle to adoption of asset tokenization by regulated financial institutions. One issue is that there are often a large number of regulatory bodies that have a hand in defining regulations, which can make tokenization compliance complex. Today, many jurisdictions lack regulatory clarity where regulators have yet to establish rules for how tokenized securities can operate on asset exchanges and interbank networks. It remains unclear when such rules might be promulgated. Their absence tends to increase regulatory risk for institutions since it remains unclear which risk controls they should implement for compliance purposes.

As a consequence, operators in such jurisdictions may have had to work in a piecemeal fashion—use case by use case. This could help demonstrate to regulators that they can put in place the necessary controls to safeguard transactions, assets, and user information.

Learn why institutions should undertake a comprehensive risk assessment

Distributed ledgers tend to present a special conundrum—a conflict between transparency and privacy. Any institution interested in pursuing tokenization efforts should resolve this problem. Doing so comes down to making design choices about what information tokenization networks will share regarding transactions and how they share it.

Distributed ledgers can provide unprecedented transparency to the financial markets, and this can have a significant benefit for financial institutions and their regulators. Operating from a shared single source of “truth” can streamline the approval of transactions, compliance reporting, and responses to suspicious activity.

That said, transparency can come at a cost to privacy. For instance, the original bitcoin blockchain made visible all transactions associated with any wallet to all users. Yet, it did not reveal the identity of the wallet’s owner. Here’s the rub with tokenization. Greater privacy will be required in order to encourage investors to adopt tokenized assets. And naturally, investors will likely want to protect certain kinds of information from a host of parties, including potential competitors. And they will probably not agree to allow participants to see all of their transactions.

Discover how the designers of interoperable systems might address and meet those expectations

Tokenization in financial services can offer a more efficient method for trading assets and may significantly reduce operating costs for institutions. However, one of the more significant technical challenges facing institutions seeking to adopt tokenization involves integrating the technology of distributed ledgers with legacy back-end systems, while also building in the appropriate smart contracts to facilitate automation.

Here are some of the ways in which tokenization can improve efficiencies. By using distributed ledgers and smart contracts, tokenization offers the possibility of the “atomic settlement” of transactions. That means cash and securities are exchanged simultaneously in an automated fashion governed by smart contracts that also facilitate the irreversible transfer of assets or funds between parties. Consequently, atomic settlement operates on the principle that either the entire transaction succeeds or fails as a single, indivisible unit, eliminating the risk of partial or incomplete transactions. Such a process would tend to accelerate settlement times and eliminate the need for, and errors originating from, manual execution. A number of financial institutions are already investigating or working to implement.

Tokenization in financial services raises a variety of questions and challenges pertaining to accounting, valuation and taxation.

One challenge is that tokenizing certain transactions could result in an increase in the institution’s capital requirements under the SEC’s SAB 121 staff interpretation, which mandates that any SEC registrant safeguarding a crypto asset must record a safeguarding liability and corresponding asset on its balance sheet. When a token is introduced to a transaction, an institution may have to record a separate safeguarding liability and corresponding asset for the token and may also be required to increase its capital holdings depending on any relevant regulatory requirements. Issuing and safeguarding many tokens could require that an institution keep much higher capital reserves.

Additionally, different challenges may arise depending on the underlying asset and the legal construct of the tokenized asset. The seminal question is whether the tokenized asset conveys rights and obligations upon a holder that might differ from a direct holding of the underlying asset. For example, consider a scenario where secondary markets are available for the tokenized asset that are not available in the underlying asset. Unintended tax consequences may result from creating new liquidity, transaction types, or simply by not adhering to the commonly accepted legal form under which tax analysis typically relies. Tokenization may therefore change the character of the asset held and alter the timing, sourcing, or recognition for income earned.

Get familiar with some of the tax and accounting advantages resulting from tokenization

Setting sail amid uncertainty

Resolving the challenges of tokenization and realizing the benefits of tokenization will likely require considerable time and effort, as well as collaboration among industry stakeholders. The process will be a gradual, multi-front process, and it is very unlikely that any one party will achieve any monumental breakthrough. It will all be incremental.

Commercial success of tokenization could usher in a new era for the financial services industry. With the path yet to be defined, organizations will likely need to work through complex and diverse challenges including interoperability and secondary markets, regulation and risk management, privacy, legacy systems, and tax and accounting. Early movers that can assess the tokenization effort holistically while tackling each of these hurdles could lead their industry in the future.

Contact us

Our Blockchain & Digital Assets leaders are ready to help your business trailblaze in this space – with a multi-lens perspective that provides clarity through the complexity. Reach out to ask a question, start a conversation, and select “yes” below to subscribe for the newest insights and reports about Blockchain and Digital Assets.

Get in touch

Recommendations

The use of cryptocurrency in business

Why companies should consider using cryptocurrency

Risk management and governance of digital assets

Managing the evolving risks of DeFi, CeFi, and tokenization