Banking supervision and regulation report has been saved

Perspectives

Banking supervision and regulation report

Federal Reserve releases its inaugural report on banking system conditions

A summary of the Fed's banking supervision and regulation report, summarizing current banking system conditions and recent supervisory and regulatory actions.

January 3, 2019 | Financial services

On November 9, 2018, the Federal Reserve Board (FRB) released an inaugural version of a Supervision and Regulation Report,1 which summarizes current banking system conditions and the board’s recent supervisory and regulatory actions. The report highlights identified trends going back to the financial crisis, including semi-annual distribution and issues and forward-looking supervisory concerns across institutions—including the large banking organization portfolio and the Large Institution Supervision Coordinating Committee (LISCC) portfolio across US bank holding companies (BHCs), US banks, and foreign banking organizations (FBOs).

During the testimony before the US House of Representatives Committee on Financial Services, Federal Reserve Board (FRB) Vice Chairman for Supervision Randal K. Quarles presented the report,2 which focuses on FRB’s prudential supervisory activities, as a tool to keep Congress and the public informed about the FRB’s works.

With the FRB recently finalizing a new rating system for large financial institutions and with banking agencies clarifying the role of supervisory guidance,3 the report reflected another step for the FRB to strengthen transparency in regulation and supervision. The report discusses highlighted areas in banking system conditions, regulatory developments, and supervisory developments.

Summary of FRB’s perspectives

According to the report, overall the banking sector in the United States appears to remain in strong condition, with robust economic performance, fewer nonperforming loans, lending growth, and stable overall profitability. The report highlights that US banking firms are currently well-capitalized and have stronger liquidity positions, while the largest firms have developed resolution plans that reduce the negative systemic impact.

Further, half of the supervisory findings for large banks issued in the past five years were related to areas of governance and risk-management control issues, including weaknesses in Bank Secrecy Act/Anti-Money Laundering (BSA/AML) programs, internal audit functions, IT risk management (including

- Capital;

- Liquidity;

- Governance and controls; and

- Recovery and resolution planning.

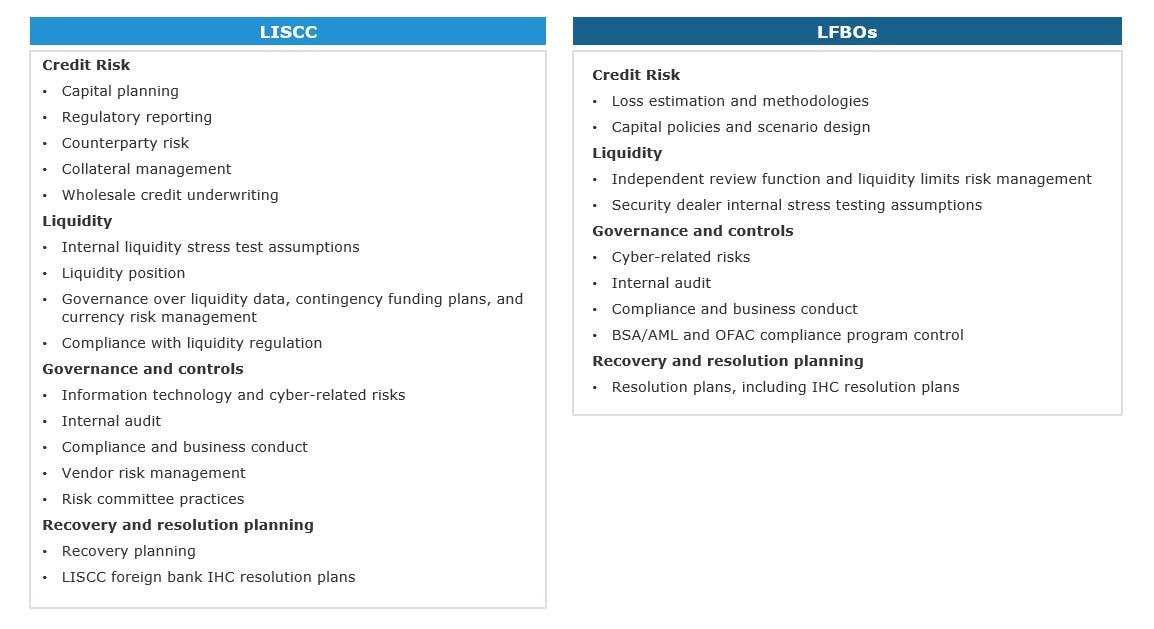

Overall, large financial institutions, which include LISCC portfolio companies and FBOs, have addressed and closed out a significant number of supervisory findings (matters requiring attention (MRAs)). However, MRAs have increased for large FBOs, reflecting changes in regulation that required substantive changes to their US structures. See below for a list of supervisory findings for various types of banking entities:

Supervision of LISCC firms

- The overall safety and soundness of LISCC firms

has improved recently, with firms meeting regulatory capital requirements and incorporating enhanced capital planning practices. - LISCC firms have also improved governance practices and have strengthened aspects of how they manage compliance with internal and regulatory requirements and other operational risks.

- US LICC firms improved their ability to mitigate the adverse effects of potential failure and unwinding of their operations.

- Over half of the supervisory findings issued in the past five years were related to governance and risk-management issues, including weaknesses in BSA/AML programs, internal audit, IT risk management, and model risk management.

Supervision of Large and Foreign Banking Organizations (LFBOs

LFBOs - Some firms have shown weaknesses in the liquidity risk identification processes and a lack of robust internal risk functions.

- Almost 70 percent of supervisory findings for LFBO firms are nonfinancial risks, including governance and controls, BSA/AML issues, and IT risk management deficiencies.

- FBOs continue to strengthen risk management and reporting systems of their respective intermediate holding company (IHCs) to meet supervisory expectations. Supervisory findings for FBO branches and agencies are concentrated in compliance risk management and controls.

Upcoming supervisory priorities

Main takeaways

- Increase in transparency: The release of the Supervision and Regulation report aligns with the FRB’s efforts to improve transparency and provide more public information about the board’s supervisory activities to regulated institutions. This transparency can provide a forward look into supervision and examination areas of focus.

- Considerations for regulatory relations efforts: The efforts by the Federal Reserve to recalibrate their supervisory programs to confirm they are effectively and efficiently achieving their goals, has resulted in an increased emphasis on risk-focusing examination activities, dependent on the financial institution risk assessment. The summaries of examination findings provide a comparative view across portfolios, trends over time, and provide a high-level ability to compare one’s own institution vis a

vis the entire portfolio. - Calibration against internal issues management processes: The report emphasizes the current safety and soundness of the US banking system, and how the FRB is now at a stage of testing the effectiveness and efficiency of its post-crisis regulatory framework and simplifying the framework without sacrificing financial stability. It will be important for regulated institutions to recognize that although capital and liquidity positions may generally be stable, continued deficiencies in managing nonfinancial risks, such as governance, internal controls, BSA/AML, or IT risk, may place the ratings at risk.

- Communication tool: Banking institutions should consider utilizing this report for board and senior management discussions to help calibrate the broader industry landscape and their own issues, examination priorities, and feedback. The analysis

on priorities provides early warning on areas with self-identified or internal audit-identified issues. These also may represent areas that coincide with compliance plans and areas for training. In essence, this can be a “roadmap” for their regulatory interactions.

As further developments occur, Deloitte will issue additional updates as appropriate.

Contact us

Irena Gecas-McCarthy |

David Wright |

Simren Flora

|

||

Kyle Cooke |

Marco Kim |

Endnotes

1 Board of Governors of the Federal Reserve System, “Supervision and Regulation Report,” (November 2018), available at https://www.federalreserve.gov/publications/files/201811-supervision-and-regulation-report.pdf

2 FRB Vice Chairman for Supervision Randal K. Quarles, Remarks on the “Supervision and Regulation Report” https://www.federalreserve.gov/newsevents/testimony/quarles20181114a.htm

3 Board of Governors of the Federal Reserve System, “Agencies issue statement reaffirming the role of supervisory guidance” (September 11, 2018) available at https://www.federalreserve.gov/newsevents/pressreleases/bcreg20180911a.html

This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

Recommendations

Regulatory developments for foreign banking organizations

Year three of Enhanced Prudential Standards