Technology and data governance has been saved

Perspectives

Technology and data governance

Investing in a way that pays back

Financial institutions are increasingly seeing the need for an increased focus on investments in technology and data governance that can provide standard-yet-granular and high-quality data to support financial stability, and help with monitoring their safety and soundness.

October 14, 2020

The FRB announced the launch of a pilot program to support the development, testing, and adoption of FedNow and has invited a number of financial institutions, as well as service providers and payment processors that partner with financial institutions to participate. The FRB expects to bring its FedNow products to market on an iterative basis to meet industry demand, and it anticipates having the first version of its release available by 2023 or 2024.

Real-time payments

August 6, 2020

The Federal Reserve Board (FRB) released additional information on its planned FedNowSM Service (FedNow), a solution in support of real-time payments (RTP). The updated details provided in the FRB’s release included a response to public comments received on its original announcement and from the August 2019 request for comment. FedNow is expected to be a real-time gross settlement (RTGS) service that enables faster payments and supports 24x7x365 settlement for all banks and payment processors (financial institutions) to settle directly through the Federal Reserve System (the Fed).

Even though The Clearing House (TCH) introduced its private-sector RTP® service in 2017, the US is still behind some countries in the widespread adoption of faster payments.

May 10, 2018 | Financial Services

The right kind of data must also be easily accessible and malleable enough to be re-purposed as needed, and provide actionable insights and analysis. Beyond regulatory compliance, executives understand that their firms stand to reap other business benefits that can provide competitive advantages. This was echoed in a recent survey where CFOs were asked:

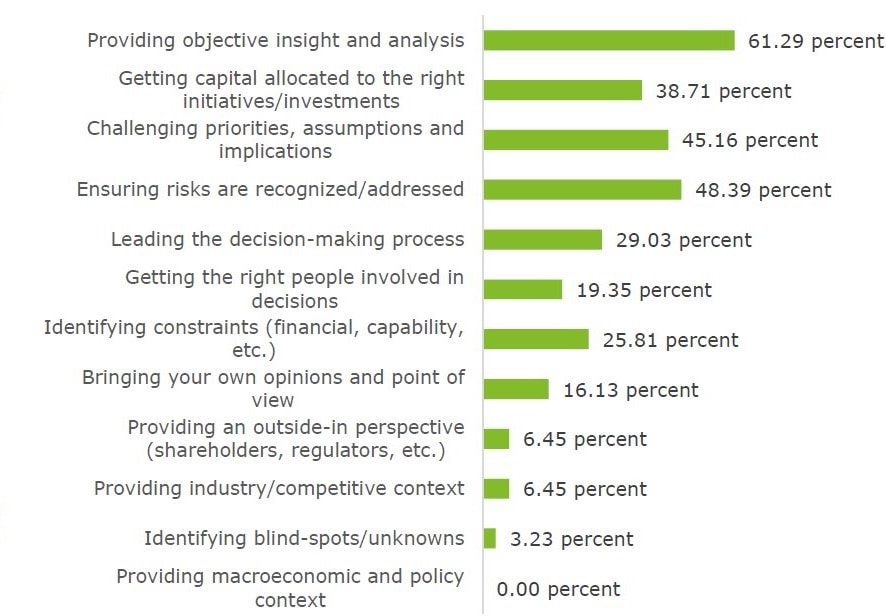

What are your most important personal contributions to your company's planning processes?

Although responses varied by industry, many CFOs cited the following: Providing insight and analysis, ensuring risks are recognized, allocating capital to the right initiatives, and challenging priorities and assumptions.

Figure 1: Deloitte LLP CFO Signals 4Q ’17, CFO Role in Business Planning p27. Published 10-Jan 18

How did the industry get here?

One of the outcomes of the financial crisis was the enactment of the Dodd-Frank Act and other requirements (such as Basel III, Comprehensive Capital Analysis and Review (CCAR), and Capital Liquidity Analysis and Review (CLAR)), which centered on granular, high-quality data throughout financial institutions, including heightened internal controls through an enterprise-wide governance structure. Today, most key executives such as chief financial officer (CFO) not only have to know and analyze their data as part of risk monitoring, but are mandated to attest to the quality of their data (e.g., CFO attestation).

In short, the impact of the crisis and increased regulatory requirements has changed the business landscape. Financial institutions must not only make operational changes to meet regulatory requirements, but they must also strategically position themselves to increase the business value for making investments. A key question is, “How do firms make the requisite investments to not only help comply with their regulatory requirements but also help enhance business value across the enterprise?”

Investments that pay back

While many executives are examining ways to a foster growth in their plans, capital efficiency and returns remain a focus. Financial institutions can consider the following examples of investment areas and potential payoffs when formulating their technology and data governance strategy:

| Opportunity | Need/challenge | Investment | Potential pay back |

|---|---|---|---|

| Capital efficiency | Lack of transparency and organization in transaction data can cause financial institutions to default to higher capital charges, resulting in inefficient use of capital |

Cognitive Intelligence/Robotic Process Automation offers ways to look through documents that support transactions (e.g., prospectuses, loan agreements) to support applying appropriate capital to exposures |

|

| Free up and re-allocate human capital resources | Large transaction volume that requires a substantial level of manual testing effort may create quality control issues and inefficient use of human capital |

Automation capabilities (e.g., Robotic Process Automation, Natural Language Processing/Generation) can be applied to controls that are suited to automation to increase efficiency and improve testing coverage |

|

Financial institutions have the need to manually process high volumes of forms in the first lines, thereby reducing resources available for knowledge intensive tasks and processes |

Machine Learning and Natural Language Processing provide opportunities for data extraction, processing, and integration of information from the forms into IT systems |

|

|

| Data aggregation and reporting | Regulators have increasingly moved toward standardized reporting via forms such as FR Y-14A; FR Y-14Q; and FR Y-14M, etc., creating the need for supporting capabilities |

Sustainable data and technology infrastructure that can provide standardized data aggregation and reporting to support compliance with regulatory requirements |

|

| Data governance | Increased regulatory scrutiny on data completeness and accuracy necessitates ongoing assessment of adequacy of governance framework |

Compliance assessment framework designed to identify gaps and enhance risk data controls and aggregated reporting |

|

From the design and build stage, financial institutions must think of the needed components to design/adopt a strong data architecture and technology that supports compliance with current regulatory requirements and can nimbly accommodate future changes, in light of ever evolving regulatory requirements. A strong governance framework is needed to implement robust quality controls, risk assessments, and on-going monitoring and testing. Results of monitoring and testing activities should inform proactive data compliance management.

How Deloitte can help

With an understanding of the maturity level of a data infrastructure and governance, our services can be provided through both a tactical and strategic model presented below, fostering a sustainable approach to help reduce cost and increase efficiencies:

| Categories | Tactical | Strategic |

|---|---|---|

| Data & infrastructure |

|

|

| Reporting, training & testing |

|

|

| Operating model |

|

|

| Risk & controls |

|

|

This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor.

Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

Contact us

Marjorie Forestal |

Ken Lamar |

Claudio Rodriguez |

Precious Ugwumba |

Stanley Philip |

Chris Spoth |

Irena Gecas-McCarthy |