Allowance for loan and lease losses CECL has been saved

Perspectives

Allowance for loan and lease losses CECL

The road ahead with the CECL approach

The financial downturn experienced in 2008 and afterward appeared to expose the weaknesses of the incurred loss approach. In response, the Financial Accounting Standards Board’s (FASB) proposed a new Accounting Standards Update (ASU), Financial Instruments—Credit Losses (Subtopic 825-15), commonly referred to as the Current Expected Credit Loss (CECL) model. Under CECL, entities are required to account for expected losses over the estimated life of the loan. The CECL guidance represents a substantial departure from current allowance for loan and lease losses (ALLL) practices. Therefore, adoption of the CECL model will require a well-thought-out tactical plan.

We are pleased to present the third publication in a series that highlights Deloitte Risk and Financial Advisory’s point of view about the significance of the FASB’s update, ASU 2016-13–Measurement of Credit Losses on Financial Instruments, and related implementation considerations.

CECL modeling considerations

Transitioning from the current accounting guidance’s incurred loss approach to CECL will require a significant amount of thought and discussion with key stakeholders. Two key changes that may impact credit modeling include:

Life-of-loan estimates

One of the most talked about aspects of CECL is the use of a life-of-loan concept. In practice, the life-of-loan concept is widely viewed as replacing the LEP that is currently used, thus creating the potential that estimates need to cover a longer loss horizon.

It is widely expected that many loan portfolio segments will have longer average lives than LEPs. To better understand the differences between these two loss horizon estimates, institutions should consider the following methods as possible starting points in the process:

- To determine the life of the loan time horizon, an institution could take the weighted average life of the loan (by portfolio) to estimate the time horizon over which to forecast losses.

- Banks can then begin developing life-of-loan loss estimates and justify adjustments from the historic average losses estimated using LEPs.

Reasonable and supportable forecasts

The estimate produced by the CECL model would be founded on management’s assessment of current conditions and forecasts about future conditions. Some considerations in developing forecasts include:

- Significant reliance on judgment where detailed long-term forecasts are not available.

- Regulatory stressed scenarios not intended to be used directly for accounting purposes.

- Development and documentation of processes to demonstrate appropriate macroeconomic scenarios used in ALLL estimation under CECL (i.e., scenario generation).

- Consistent application of macroeconomic forecasts and other relevant information where credit risk drivers of the portfolios are affected by forecasts/assumptions in a similar manner.

Points of convergence

While CECL represents a significant change in accounting for the allowance, current credit risk measurement approaches used for Basel regulatory capital calculations, economic capital, and stress testing (CCAR/DFAST) provide some elements that can be potentially leveraged for CECL. The underlying transition matrix, loss curve, and expected loss (EL) framework loss estimation methodologies, among others, have several points of convergence that can be leveraged through an integrated approach. Some key examples include:

- Balance sheet mapping/exposure identification

- Data sourcing

- Infrastructure

- Processes and controls

- Risk models and valuation engines

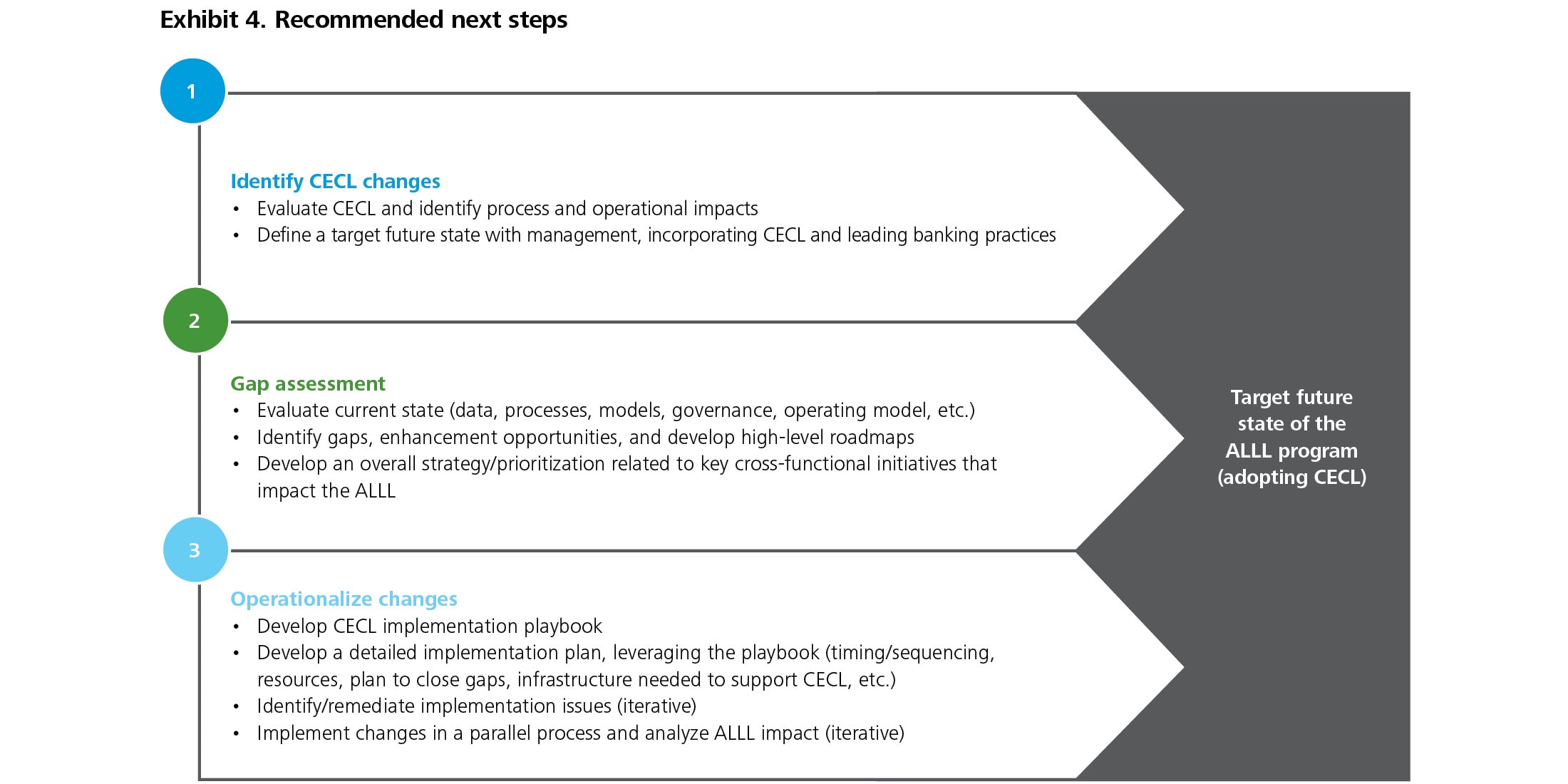

Next steps

To prepare for CECL, develop an implementation framework that aligns with the company’s strategy. Board members should push risk management to be prepared for the transition so that the change in the reserve estimate under CECL is transparent to regulators and external auditors from modeling and process standpoints.

Successful implementation of the CECL standard will also require a well-thought-out tactical plan to meet the implementation framework’s objectives. One way to operationalize the CECL implementation is to develop a CECL playbook that includes detailed roadmaps describing how initiatives will be implemented. The exhibit below provides some recommended next steps in assessing and planning for CECL adoption, above and beyond the development of a CECL playbook.

Additional information can be found in parts one and two of the series, Staying ahead: Allowance for loan losses and Putting current expected credit losses in perspective: Fundamentals of implementation success.

CECL series

- Staying ahead: Allowance for loan leases

- Putting current expected credit losses in perspective: Fundamentals of implementation success

- Practical insights on implementing IFRS 9 and CECL: ASU 2016-13 and opportunities for implementation efficiencies

- Additional CECL-related information can be found on our credit impairment resource page

Learn more about CECL

Download the publication to explore more about the proposed CECL model and anticipated implementation challenges, as well as some ways organizations can use CECL model implementation as a catalyst to align accounting impairment and regulatory capital processes.

Additional information is available around allowance for loan losses (ALL) and current expected credit loss (CECL).

Get in touch

Recommendations

2017 US Current Expected Credit Loss (CECL) survey

Explore implications of the FASB’s new credit impairment standard