New lease accounting standard and effective date has been saved

Perspectives

New lease accounting standard and effective date

Facing challenges and managing the process

After the recent Financial Accounting Standards Board (FASB) meeting in November 2017, which resulted in new options and relief provisions for companies to consider, companies still face challenges as they prepare to implement the new lease accounting standard.

June 26, 2018

A blog post by Beth Kaplan, managing director, Deloitte & Touche LLP

In our January Dbriefs webcast, Lease accounting: Implementation enters the final stretch, panelists discussed the new guidance and provisions to the new accounting rules, implementation challenges companies may face, and other operational considerations as the new lease accounting rule's effective date of January 1, 2019 approaches.

Featuring special guests Todd Sears, vice president and assistant corporate controller, Walmart; James Barker, partner, Deloitte & Touche LLP; and Sean Torr, managing director, Deloitte & Touche LLP, participants heard insights into how companies can manage the implementation process, how the new guidance can simplify implementation, and tips to address challenges that many are facing or will face in the year ahead.

New lease accounting standard effective date

ASC 842, Leases, was added by ASU 2016-02 on February 25, 2016. The new guidance is effective as follows:

- For public business entities, the standard is effective for annual periods beginning after December 15, 2018 (i.e., calendar periods beginning after January 1, 2019), and interim therein.

- For all other entities, the standard is effective for annual periods beginning after December 15, 2019 (i.e., calendar periods beginning after January 1, 2020), and interim periods after December 15, 2020.

- Early adoption would be permitted for all entities.

For more information, read our Heads Up publication which addresses frequently asked questions about the lease accounting standard.

New FASB guidance and what it means for the implementation process

In November 2017, the FASB issued new proposed guidance to simplify the lease accounting implementation process. This included the elimination of the requirement to evaluate pre-existing land easements to determine if they meet the definition of a lease under the new standard, the new option to not restate comparative reporting periods in transition, and the option of combining lease and non-lease components under certain conditions.

However, even with the new guidance, only 10.2 percent of poll respondents during the live webcast anticipated the FASB's new measures would reduce the amount of time and effort needed to implement the new standard.

The FASB relief provisions are a big deal for companies transitioning to the new lease accounting rules. But no one should slow their implementation efforts as a result of it.

— James Barker, senior consultation partner for lease accounting, Deloitte & Touche LLP

Addressing challenges as implementation enters the final stretch

As the lease accounting standard effective date looms ahead, it is important for companies to prioritize their implementation efforts to address key challenges in the process.

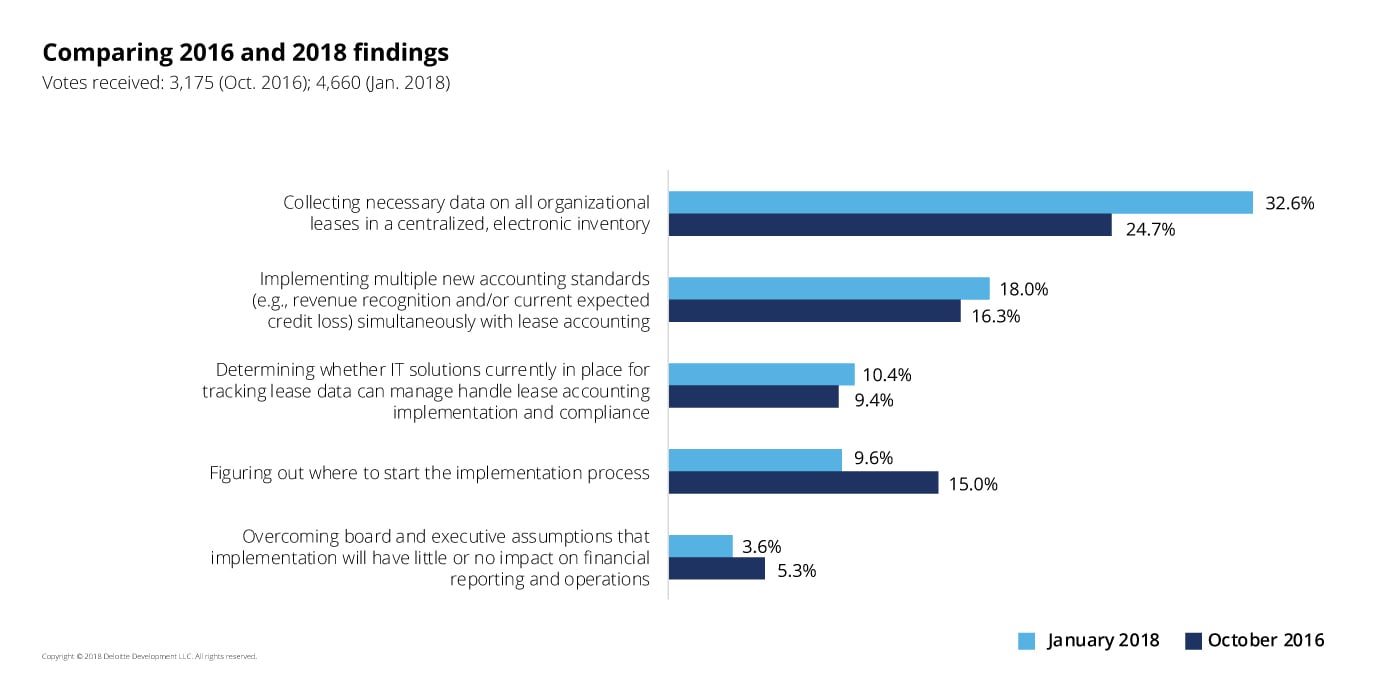

The biggest challenge? Data abstraction.

In a poll of more than 3,890 participants of the January 31 Dbriefs webcast, data abstraction remained the biggest challenge in the implementation process. Nearly one-fifth (18 percent) of respondents acknowledged that implementing multiple new accounting standards, such as revenue recognition and current expected credit loss, simultaneously with lease accounting is proving difficult. But, lease data collection to create the centralized electronic inventory remains the predominant implementation challenge (32.6 percent; up from 24.7 percent in 2016).

Which will pose the largest implementation challenge for your company's lease accounting standard compliance efforts in the next 12 months?

Dbriefs poll results: Lease accounting implementation enters the final stretch

How companies are addressing challenges

There certainly are opportunities to leverage technology to help accelerate the overall abstraction process. I think it's important to set realistic expectations, the machines could only do a certain amount, and there still is the need for human intervention.

— Sean Torr, managing director, Deloitte & Touche LLP

Many companies may be underestimating the effort it may take to collect lease data and aggregate it into a centralized system before the lease accounting standard effective date. In the follow-up podcast, our speakers continue the conversation with additional questions and further guidance on how companies can manage the implementation process, the opportunities to leverage technology, and further insights into the challenges of technology and data abstraction for the new lease accounting standards.

Listen to the archive of the Dbriefs webcast, Lease accounting: Implementation enters the final stretch, or listen to the Green Room Podcast in the audio player at the top of this post.

Visit the Controllership Insights blog for additional blog posts.

This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

Get in touch

Recommendations

Operationalizing the new lease standard

Lease accounting