Accounting automation and the future of controllership has been saved

Perspectives

Accounting automation and the future of controllership

Diving deeper into the benefits of new technologies

Our December Dbriefs webcast focused on accounting automation technologies and featured insights into the spectrum of robotics and process automation capabilities that drive initiatives to push the controllership function into the future.

May 10, 2018

A blog post by Beth Kaplan, managing director, Deloitte & Touche LLP

During the live webcast, we polled more than 1,700 finance, accounting, and other professionals about the digitization of their controllership functions. More than 50 percent of respondents said their organizations were planning digital controllership improvements—including leveraging process automation, analytics, and other technologies for financial and accounting processes—in the year ahead. Of these improvements, using robotic process automation (RPA) in finance and accounting to increase efficiency and internal control was a top priority for such efforts.

With so many finance professionals planning digital controllership initiatives, the Dbriefs and Green Room podcast offered valuable insights around the implementation of accounting automation software and robotics technology programs. These included benefits; keys to mitigating risk; the spectrum of RPA programs; and examples of how other companies are incorporating RPA in finance and accounting, managing new platforms, and developing effective business cases for RPA programs.

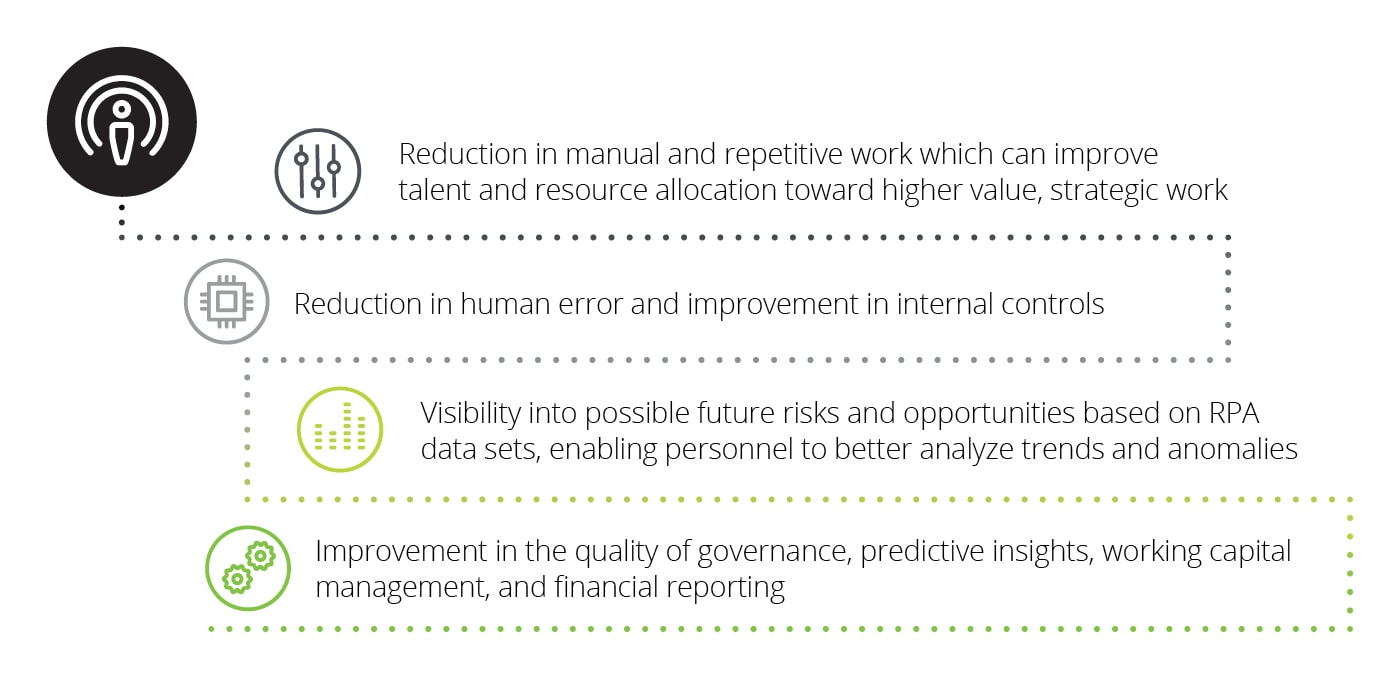

Some specific benefits of RPA for controllers:

Identifying and managing risks

We discussed areas that controllership teams can focus on to manage common risks involved in the implementation of RPA in finance and accounting.

- Technology—Improper bot design may impact existing IT infrastructure. Conversely, routine IT platform changes may impact automation technologies.

- Regulatory compliance—Accounting automation errors can reduce the accuracy of regulatory reports, risking fines and sanctions as well as legal violations.

- Operations—Poorly designed automation can cause processing errors. Also, a lack of effective oversight procedures can lead to increased operational inefficiencies.

- Talent—In times of organizational transformation, morale may suffer if employees don't understand RPA programs are not replacements and instead enable more focus on higher level work. In addition, further access to and oversight of automated processes should consider be carefully managed to prevent and detect abuse.

- Financial reporting—Poorly implemented RPA in finance and accounting can result in inaccurate or incomplete financial reports, financial restatements, and reputational damage.

In the resulting follow-up podcast, special guest Justin Wallen, who leads Global Decision Support for Pfizer, continued the conversation with answers to additional questions and more insights into accounting automation—including proofs of concept highlighting the benefits and ROI of automation to make a strong business case for implementation. Wallen also detailed a business case for automation that utilized bots to improve efficiency, internal control, quality, and cost, which added up to a positive return on investment for process automation programs at his organization.

RPA is not emerging—it is here now and mature and if people aren’t looking at it, they should be.

— Justin Wallen, Pfizer

The wealth of knowledge and real-world examples offered should help finance professionals better shape their digital strategy to build a controllership team for the future.

View the archived Dbriefs webcast, "Process automation: What it means for the future of controllership" or listen to the Green Room Podcast in the audio player at the top of this post.

Visit the Controllership Insights blog for additional blog posts.

This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

Get in touch

Recommendations

Controllership Perspectives

Navigating what’s next