UP-C Structure Services has been saved

Services

UP-C Structure Services

A tax-efficient way for partnerships to access public capital markets

Over the past 20 years, the umbrella partnership corporation (UP-C) structure has become a popular method for partnerships or limited liability companies (LLCs) to raise capital via an initial public offering (IPO) or through a special purpose acquisition corporation (SPAC).

The potential benefits of an UP-C structure

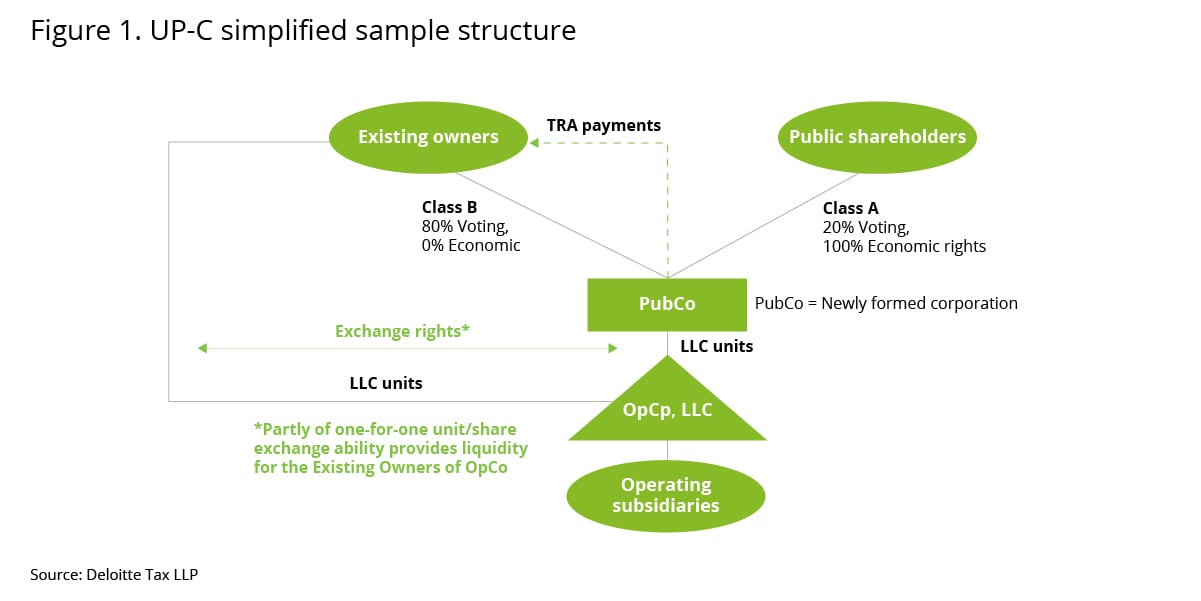

An UP-C structure is a newly formed parent company, organized as a corporation (PubCo), and its subsidiary, the pre-public offering operating entity, usually structured as an LLC or a limited partnership. Shares of PubCo are sold to the public in an IPO. PubCo then uses the IPO proceeds or newly issued stock to acquire an interest in the existing partnership whereby public shareholders have an indirect interest in the partnership. Figure 1 illustrates a simplified UP-C structure.

An UP-C structure may provide favorable benefits to historic owners. It allows them to access the public capital markets while maintaining ownership through a partnership for US federal income tax purposes, which continues to receive the benefits of a single level of taxation until the historic owners sell their interests. The UP-C structure also provides historic owners with the right to exchange their partnership interests for cash or shares of the PubCo on a one-for-one basis. To the extent the exchange is taxable for US federal income tax purposes, PubCo generally receives a step-up in its share of the partnership’s assets attributable to the acquired assets. In turn, the step-up provides PubCo additional amortization or depreciation in future periods. A significant benefit of the UP-C is in its ability for historic owners of the partnership to receive contingent installment payments upon the exchange of their partnership units through a tax receivable agreement.

Tax Receivable Agreement (TRA)

In a typical UP-C, the historic owners negotiate for the right, through a tax receivable agreement (TRA), to receive payments for a portion of the tax savings the PubCo realizes from the exchanges (in our experience typically 85% of the tax savings, see figure 1). The TRA captures the value of future tax benefits for existing owners, value that would otherwise be foregone under a traditional IPO.

TRAs can provide for significant additional contingent consideration payments by monetizing basis step-ups and other tax attributes. This value, combined with the other potential benefits of the UP-C structure, may be compelling considerations for partnerships that want to go public:

- Liquidity: An UP-C structure offers liquidity to historic owners through their ability to exchange partnership interests for PubCo shares while retaining their interest in the pass-through structure.

- Voting control: Historic owners can maintain voting control over the PubCo by issuing high voting shares.

- Compensation options: PubCo has flexibility in compensating employees by issuing restricted PubCo stock, stock options, and other types of compensatory instruments.

- Anti-takeover mechanism: A TRA typically contains termination and change-of-control provisions that serve as effective antitakeover mechanisms.

Maintaining an UP-C structure

The potential benefits of the UP-C structure should be weighed against the administrative complexity of maintaining the structure. Being a public company means being subject to regulation by the Security Exchange Commission (SEC) and other regulatory bodies, introducing new reporting and compliance requirements to the organization. UP-C structures and TRAs are complex and typically place greater demands on the organization’s accounting and tax resources, capabilities, and systems. Potential challenges include:

- Maintaining partnership books and records and tracking partnership unit exchanges;

- Administering partnership tax computation on a quarterly and annual basis that determine tax basis and other tax attributes associated with exchange transactions of historic owners of the partnership post-public transaction; and

- Addressing financial reporting and accounting issues associated with the UP-C transaction and subsequent reporting.

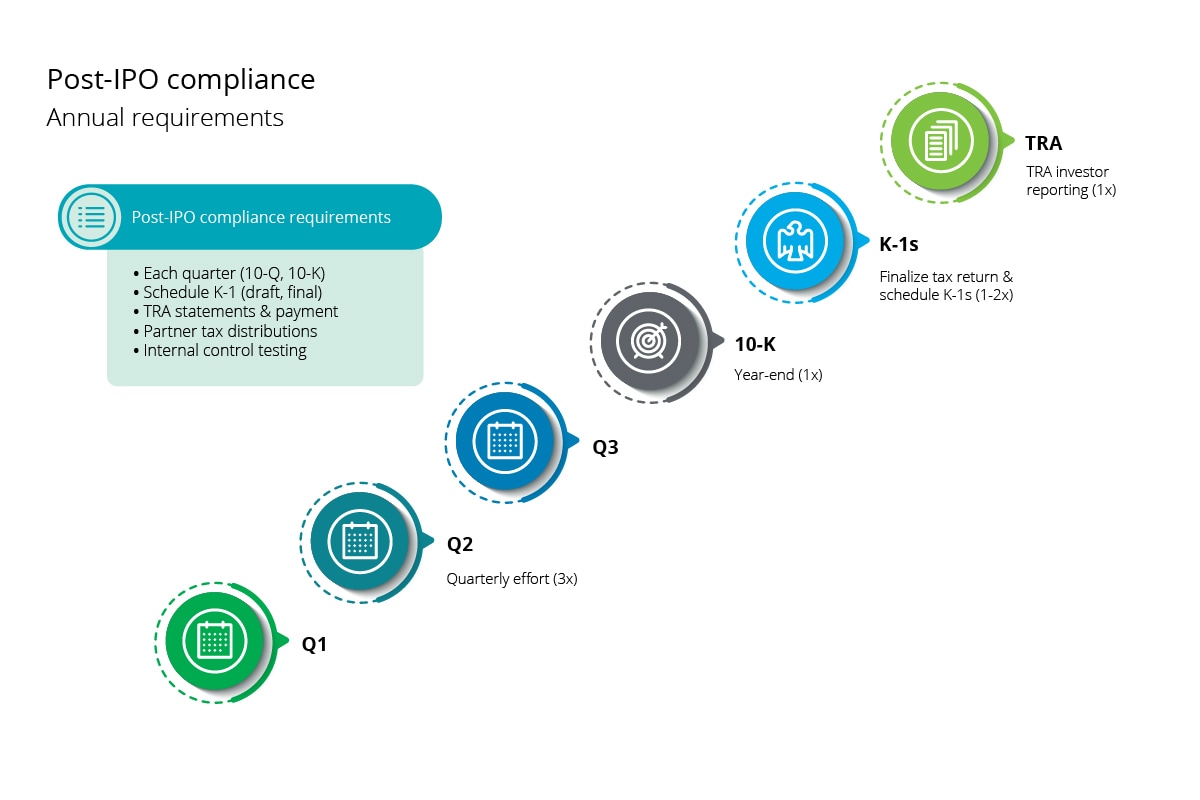

Reporting and compliance

Once the public offering is completed, the UP-C structure introduces intricate requirements and calculations for both the parent company and the partnership subsidiary, which will need ongoing maintenance. Ongoing reporting and compliance include:

Simplify compliance with Deloitte’s partnership compliance services delivered using iPACS.UP-C and iPACS.TRA

Advanced technology, combined with deep UP-C knowledge and experience, are key to addressing the volume and complexity of UP-C and TRA tax reporting.

iPACS, Deloitte’s proprietary tax technology ecosystem for partnerships, enables reporting and analytics, automated processes, increased efficiencies, and transparency—all while reducing risk and achieving scalability.

See how iPACS simplifies the UP-C compliance process, improves quality, timing, and efficacy, and helps maintain the UP-C structure

iPACS.UP-C and TRA modules

iPACS.SubK and iPACS.TRA are bespoke modules of iPACS capable of meeting the complexity of tax compliance obligations for UP-C structures.

Tailored specifically for UP-C clients, the iPACS.UP-C and iPACS.TRA modules support the full range of UP-C computation and reporting requirements and help UP-C organizations achieve efficiencies year over year.

iPACS streamlines tax compliance and provide UP-C management with clear, transparent, customized reporting and analytics to provide insights and facilitate decision-making. Reap the benefits of Deloitte’s tax services delivered via the iPACS technology ecosystem for your organization’s post-public offering administrative effort:

- Accessibility: Web-based iPACS technology lets you own your data and can be accessed at any time;

- Quality and transparency: Provides a view into tax processes for key stakeholders;

- Added efficiencies: No more using multiple spreadsheet models for quarterly and annual UP-C effort;

- Scalability: Scales and adapts over time based on the needs of your business; and

- Risk management: Fewer manual processes reduces errors and enables a focus on more proactive risk management.

Looking forward

Businesses considering an UP-C have many factors to contemplate. The advantages are compelling, as are the challenges. Deloitte provides a dedicated national team of UP-C specialists to help you with both the UP-C conversion and ongoing tax compliance. From day one, we have led the industry with regard to the UP-C structure and are the leading-edge innovator ever since. We offer deep knowledge and tailored processes powered by proven technology. Contact your Deloitte engagement team or one of the specialists below to get started.

Contact us

Sean Brennan, Partner, National Federal Tax Services, Deloitte Tax LLP

Dan Brown, Partner, National Federal Tax Services, Deloitte Tax LLP

Scott Greenman, Partner, National Federal Tax Services, Deloitte Tax LLP

Travis Nemes, Managing Director, National Federal Tax Services, Deloitte Tax LLP

Vanessa Stucky, Partner, National Federal Tax Services, Deloitte Tax LLP

Jen Chu, Partner, M&A Transaction Services, Deloitte Tax LLP

Ashley Cortez, Principal, M&A Transaction Services, Deloitte Tax LLP

Ben Applestein, Principal, Washington National Tax – Passthroughs, Deloitte Tax LLP

Recommendations

The Up-C deal structure for pass-through entities

An advantageous umbrella structure for IPOs and SPAC mergers