The Up-C deal structure for pass-through entities has been saved

Perspectives

The Up-C deal structure for pass-through entities

An advantageous umbrella structure for IPOs and SPAC mergers

If you’re considering an entrance into the public markets, you’re likely facing challenging questions. Do you go with a traditional IPO or merge with a SPAC? When will pricing be right? But for pass-through entities such as partnerships or limited liability companies (LLCs), there is one additional question that is critical to answer – whether to choose an Umbrella Partnership Corporation (Up-C) for your deal structure.

What is an Up-C deal structure?

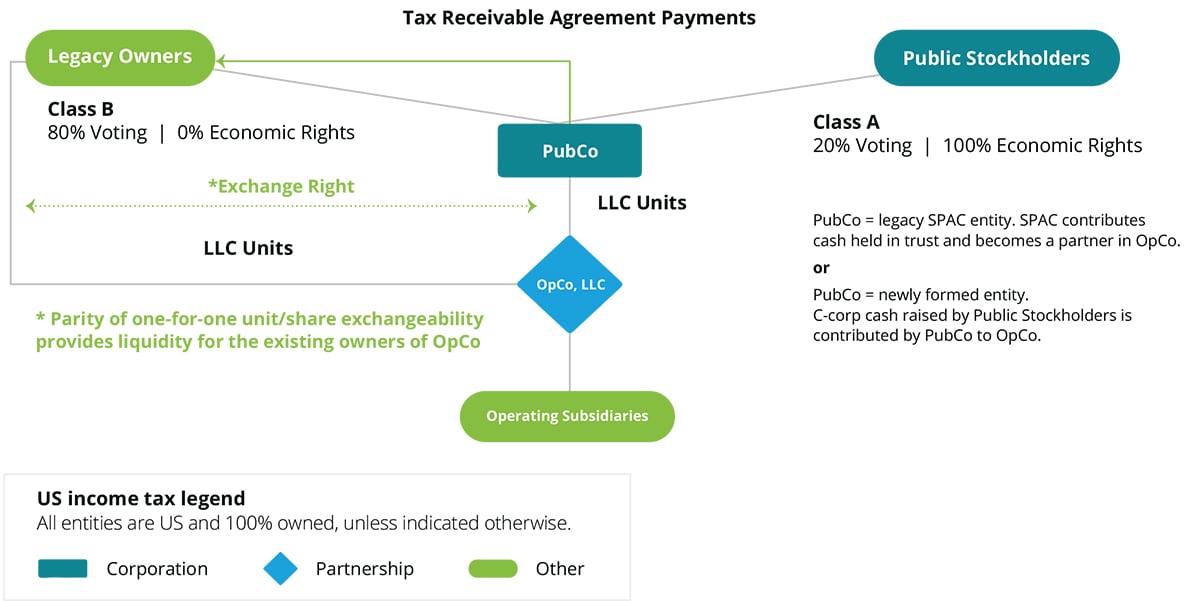

In a typical IPO Up-C structure, the existing partnership owners in an operating company (OpCo) form a C corporation (PubCo) that is organized as a holding company with no material assets other than its equity interest in the existing partnership. In a typical Up-C structure as part of a SPAC merger, the SPAC represents PubCo in the arrangement. PubCo is capitalized with two classes of common stock: (1) Class A common stock, which is issued to public investors and provides both voting and economic rights in PubCo, and (2) Class B common stock, which is issued to the existing owners of the partnership and only provides voting rights in PubCo.

Deal structuring for pass-through entities: The Umbrella Partnership Corporation

In order to complete the Up-C structure, the existing owners execute a reorganization that results in the unitization of the owners’ existing interests in the partnership. The common units are intended to maintain the owners’ existing economic rights related to their interests in the partnership. The common units held by the existing owners do not provide the existing owners with any voting rights related to the partnership. Rather, all the voting power in the partnership is held by PubCo through its role as managing member.

In addition to the common units held in the partnership, the existing owners will also hold an equivalent number of shares of Class B common stock in PubCo, which provides the existing owners with voting rights in PubCo. The owners may exercise their right to exchange their common units and shares of Class B common stock on a one-for-one basis for shares of Class A common stock in PubCo.

Figure 1 depicts a typical Up-C structure:

This deal structure can provide significant tax benefits to its historical owners for years after the deal closes. In order to capture these benefits, there are considerations that need to be tackled on the front end of deal execution, from tax implications associated with the timing of the deal to certain accounting and reporting complexities.

Tax considerations

An Up-C structure may provide favorable tax benefits to pre-IPO owners. It allows them to access the public capital markets while maintaining ownership through a partnership, which continues to receive the benefits of a single level of taxation until the pre-IPO owners sell their interests. The Up-C structure also provides pre-IPO owners with the right, through an exchange agreement, to exchange their partnership interests for shares of the PubCo on a one-for-one basis. These exchanges generally result in a step-up in the tax basis of the partnership’s assets, which, in turn, increases amortization and/or other deductions available to PubCo. A significant potential benefit of the Up-C is its ability for historical owners of the partnership to receive a premium on the value of their partnership units.

The Up-C structures present a tax planning opportunity. The sale of a partnership interest from one partner to another creates a step-up for the buying partner in the underlying basis of the organization’s assets. This step-up is a benefit to the buyer, as the higher basis can serve as a tax deduction against future income. Due to this benefit being provided to the buyer, the seller in this scenario would normally pursue a higher price for the sale because it’s akin to an asset sale. An Up-C structure provides a way to compensate the seller for the tax benefits being provided to the buyer. Through the use of a Tax Receivable Agreement (TRA), this deal structure may enable the original members/partners to receive a future stream of income from the step-up as the corporate buyer uses the step-up benefits as a reduction to future taxes.

The public company itself functions as a partner within the partnership, enabling the continuing members/partners to access the public markets via future exchanges of partnership interests for PubCo stock.

There are benefits and complexities to an Up-C structure:

- Up-C structures offer companies the opportunity to extract value for pre-IPO owners that is not available through traditional IPOs or SPAC mergers. In addition, it allows the pre-IPO owners to retain a single level of taxation while obtaining the benefits of accessing the public capital markets once they choose to exchange.

- The corporate tax rate remains comparatively low; however, the potential benefits associated with the structure still warrant consideration in the current environment.

- Businesses considering an Up-C deal structure should consider timing of the Up-C conversion, going public, and any major transactions that occur along the way, because each may cause different tax outcomes.

Accounting and reporting considerations

In an Up-C structure, PubCo must evaluate whether it should consolidate the partnership. A key factor in this evaluation is whether the partnership represents a variable interest entity (VIE). The partnership is likely considered a VIE unless either (1) a simple majority have the ability to remove PubCo as the managing member, or (2) the limited partners that hold equity in the partnership can participate in the significant financial and operating decisions of the partnership.

Below, we discuss some of the typical arrangements and outcomes related to consolidation and other accounting and reporting considerations based on our experience in the field. However, these analyses are complex and variable, and specific fact patterns may create unique considerations that could impact the conclusion for a specific company.

If the partnership qualifies as a VIE, PubCo will typically consolidate the partnership because PubCo, through its role as the managing member, has the power to direct the activities of the partnership that most significantly affect the partnership’s economic performance. In a SPAC merger, this may result in the SPAC accounting for the merger as a forward transaction requiring purchase accounting, as opposed to a reverse merger.

If the partnership does not qualify as a VIE, then PubCo generally will not consolidate the partnership under the voting interest model.

In an Up-C structure, existing owners enter into an exchange agreement that specifies the terms and conditions pursuant to which the investor can monetize its investment in the partnership upon consummation of the IPO or SPAC merger. Generally, to monetize its investment, an existing owner is first required to exchange its common units in the partnership and shares of Class B common stock in PubCo into shares of Class A common stock in PubCo on a one-to-one basis, subsequent to which the owner can sell its shares of Class A common stock in the open market.

Notwithstanding, in some Up-C structures, PubCo has the right to redeem the owner’s common units in the partnership and shares of Class B common stock in PubCo for cash if the owner notifies PubCo of its intent to exercise its exchange right. When redemption provisions exist, companies should evaluate those provisions, along with which party controls the redemption options, to determine whether the existing owner’s noncontrolling interests should be classified as a liability, permanent equity, or temporary equity. In addition to the initial classification determination, noncontrolling interests represent an ongoing administrative requirement for both accounting and tax purposes, often requiring the coordination of the two departments to appropriately reflect the activity of the PubCo.

TRAs are commonly used in Up-C deal structures to provide existing owners the ability to retain tax benefits associated with ownership in a pass-through entity. Although TRAs are primarily used for tax reasons, companies should consider the appropriate accounting for the TRA. Typically, companies record a deferred tax asset, which represents the amount of the total estimated realizable tax benefit, and a liability representing the total estimated amounts payable under the TRA unless recognition is not expected based on an assessment of earnings projections.

Significant tax benefits with an Up-C structure

Becoming a public company, whether through a regular way, IPO, or SPAC merger, presents opportunities for both mature and emerging companies. The volume and value of this activity has been on the rise in recent years. For the existing owners of a pass-through entity, an Up-C structure can provide significant tax benefits for years to come. While there often are significant accounting and reporting complexities that arise as a result of the consolidation implications associated with this structure, with a bit of foresight and the right experience, this deal structure can deliver these tax benefits and opportunities along with access to the capital markets. Deloitte can help you learn more about using an Up-C structure.

Get in touch

Will Braeutigam

US Capital Markets Transactions Leader | Deloitte & Touche LLP

Recommendations

IPO Readiness and Execution Services

IPO planning, assessment, readiness, execution, and post-IPO services

UP-C Structure Services

A tax-efficient way for partnerships to access public capital markets