Pioneering early SAF transactions has been saved

Perspectives

Pioneering early SAF transactions

Takeaways and lessons learned on sustainable aviation fuel

Deloitte is committed to achieving operational net-zero greenhouse gas emissions by 2030. To help us get there, we’ve entered into several sustainable aviation fuel (SAF) agreements, many the first of their kind. In this report, we detail our experiences, along with considerations for other companies entering the SAF market.

As part of WorldClimate, Deloitte is focused on driving responsible climate choices, including a commitment to operational net-zero greenhouse gas emissions by 2030. To help achieve our goal, we’ve entered into sustainable aviation fuel (SAF) agreements with several airlines—among the first of their kind—to cover a portion of our business travel. As the nascent SAF market grows, we’d like to share some early experiences and insights.

Key findings:

- To grow the demand-side market, there is a need for consistency and assurance in corporate reporting.

- Companies need confidence that SAF’s “sustainable” label has integrity.

- In our pilot transactions, different methodologies were used to calculate emission benefits. Standardized emissions calculations would be beneficial in providing a uniform and trustworthy approach.

- To mitigate the risks of negative environmental implications of SAF, there is a need to improve the transparency of SAF supply chains, and particularly feedstock inputs.

- It’s critical that SAF transactions and their outcomes are structured in a standardized way to enable this market to scale efficiently and credibly. Standardization will enable buyers to compare fuel attributes on an equivalent basis and send a clear signal for fuel of the highest integrity through SAF certificate purchases.

- The broad range in costs we paid indicates that the nascent SAF market has ample room to mature and equilibrate across similar types of SAF production.

Our motivation for embracing sustainable aviation

For us, mitigating climate change means demonstrating leadership through tangible climate action. As part of our efforts to meet our emission reduction goals, we’re prioritizing real, tangible, in-sector emissions reductions, not offsets.1 So, in addition to increasing our virtual work and business meetings, we’re working to ensure that when we are onsite with our clients and teams for the moments that matter, we do it with a much smaller emissions footprint. While several innovations show promise in helping to decarbonize the aviation sector,2 sustainable aviation fuel is a key solution available today, which is why we’re focusing our efforts there.

In our first major step toward advancing the SAF market, we purchased the environmental attributes of more than half a million gallons of SAF. These purchases allow Deloitte the right to claim the associated emissions reductions that result from its use. In the future, these claims will be verified by issuing SAF certificates (SAFc). Originally proposed by the World Economic Forum (WEF) Clean Skies for Tomorrow (CST) coalition,3 the SAFc is intended to create a publicly approved way for companies to invest in and claim the emissions reductions from their use of SAF through a digital certificate system without ever owning or handling the physical fuel. However, because the SAFc system does not yet exist, our pilot transactions this year did not generate SAF certificates.4

Our experiences with the SAF market

In spring of 2021, we collaborated on SAF pilot transactions with three airlines: American Airlines, Delta Air Lines, and United Airlines. In these pilots, we purchased the right to claim Scope 3 emissions reductions (see “Sustainability considerations” for more on emissions scopes) associated with more than 630,000 gallons of SAF, resulting in more than 5,500 metric tons of CO2e of emissions reductions relative to conventional jet fuel. These savings equate to the emissions from more than 19,000 economy-class passengers flying one way from New York City to Los Angeles.5

Through these experiences, the valuable insights we gained fell into two broad categories: sustainability considerations and transaction considerations for future SAFc transactions.

Organizations increasingly account for and report on Scope 1, 2, and 3 emissions, in addition to actively working to reduce the emissions themselves. When airlines burn jet fuel, the emissions that result are their direct operational, or Scope 1, emissions. For airline passengers and air freight customers, these same emissions are considered Scope 3 (or indirect supply chain) emissions. When airlines replace conventional jet fuel with SAF in their aircraft, airlines can claim the emissions reductions associated with that switch within their Scope 1 disclosure, and customers can claim them as part of their Scope 3 disclosure. Emissions reductions from SAF are evaluated through a life cycle assessment (LCA), in which the emissions at every stage of the SAF supply chain, from feedstock production to fuel burn in an aircraft, are calculated and compared to an equivalent life cycle of conventional jet fuel.

The two most common calculation methods are known as “well-to-wake” and “tank-to-wake” (see figure 1). The well-to-wake method includes emissions from the production of feedstock to the exhaust of the aircraft. This method includes both upstream supply chain and direct emissions within the SAF life cycle. The tank-to-wake method only includes emissions from the combustion of fuel and does not include upstream emissions from feedstock and SAF production and distribution. For voluntary SAF purchases, the well-to-wake method is preferred in disclosure for both airlines and corporate buyers, as it captures the full emissions impact of SAF as compared with conventional jet fuel. This is the method we used.

In our pilots, each airline used a different methodology to calculate emissions benefits. Deloitte recommends that future SAFc guidance provide a standard method for airlines and their customers to calculate emissions reductions associated with a batch of SAF. Beyond life cycle emissions reductions, SAF feedstocks should also be responsibly produced and obtained upstream of the fuel production itself to be able to claim that the fuel is truly sustainable. To ensure that feedstocks are sustainable, it’s critical to understand how and where they are produced.

It’s also critical that SAF transactions and their outcomes are structured in a standardized way that enable the market to scale efficiently and credibly. Standardization and transparency of claims (and the data that underlie them) is important as it allows buyers to compare fuel attributes on an equivalent basis and sends a clear signal for the highest integrity SAF through SAFc purchases.

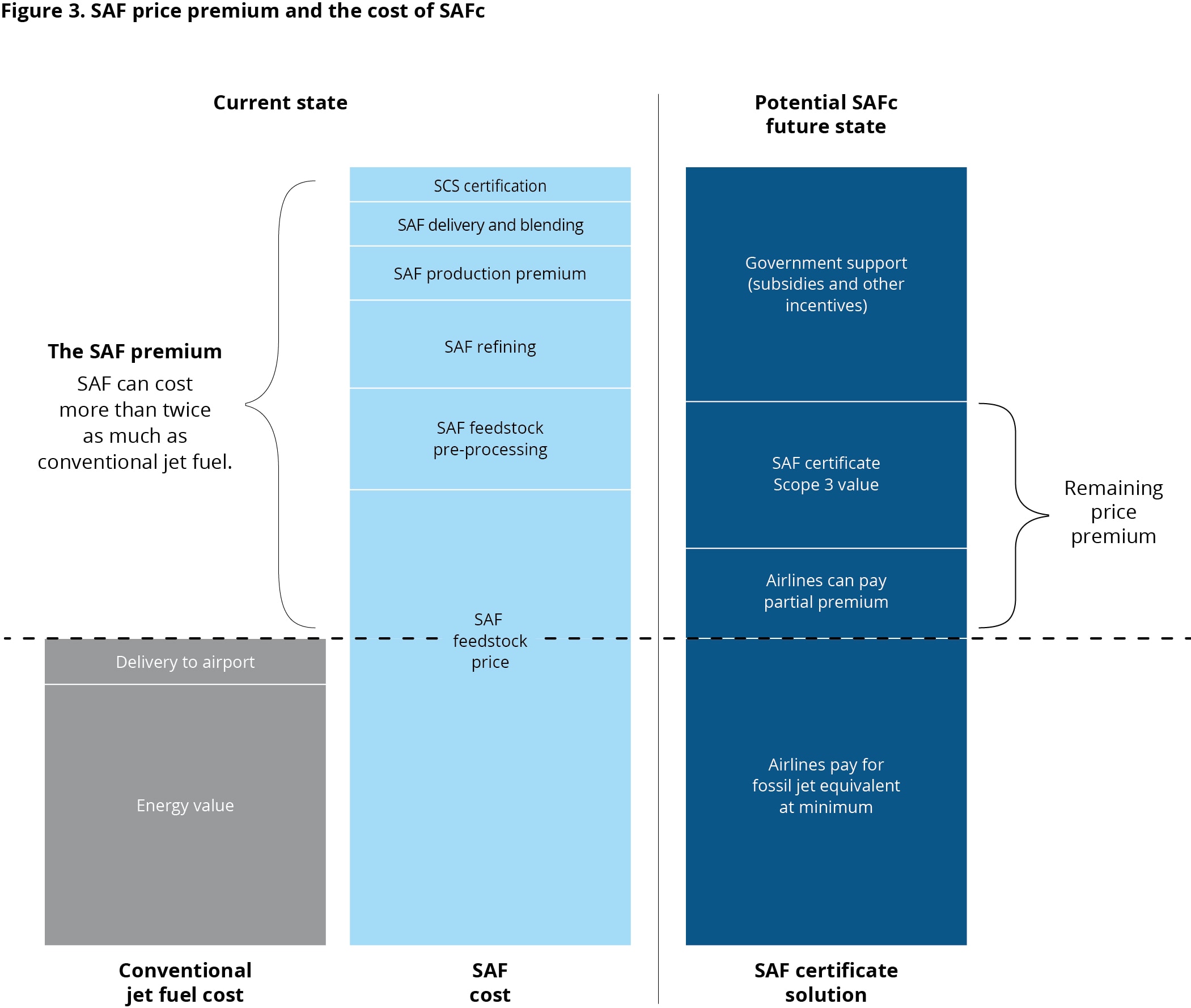

As expected in a nascent market, SAF prices range widely. In our pilot transactions, we paid a price premium of at least twice the price of conventional jet fuel. Over time, however, the cost is expected to decrease as producers learn by doing and the industry scales up production. We paid an average of $130 per metric ton of CO2e avoided (with a well-to-wake methodology), and this cost ranged by more than $90 per metric ton avoided. This significant range indicates that the nascent SAF market has ample room to mature and equilibrate across similar types of SAF production.

In all three pilot transactions, we received a predetermined SAF cost from the airlines, without a clear price breakdown relative to conventional jet fuel. In order for Deloitte and other corporations to substantiate emission reduction progress associated with the use of SAF, we need future SAFc purchases to enable credible Scope 3 emissions reduction claims and disclosures that specifically count toward business travel emissions accounting.

Even when the physical fuel associated with an SAFc purchase is not burned by an aircraft that a corporate employee is traveling on, the company would need to be able to report lower-emissions-intensity business travel as a result of its SAFc purchases. This is why a book-and-claim system that enables the physical fuel volume to be delivered to any airport (and for anyone to pay for and own the environmental attributes) is a critical element to SAF as a solution for reducing emissions from business travel. Additionally, a standardized set of contract terms that clearly articulate which emissions reductions airlines and corporate buyers can each hold and use, and in which circumstances, will make this process much more efficient, lower-risk, and less legally intensive for future SAFc transactions.

Another key consideration is whether our SAF pilots directly enabled new SAF production, as opposed to contributing toSAF that would have been purchased without our organization’s actions. Deloitte did not include a specific additionality requirement for the pilot transactions, but our purchases did facilitate new SAF delivery, and we see the value in enabling new SAF supply through SAFc transactions.

Finally, it is critical that, once the SAFc system is developed, these certificates and their associated claims are visible to the public in a transparent database or registry. The SAFc is claimed or “retired” on a registry that recognizes the final user of the emissions reduction claim. This public repository can serve as an auditable record to underlie corporate sustainability reporting, as well as voluntary and regulated disclosures. This infrastructure also can safeguard the market against the risk of double-counting emissions benefits.

What’s next for SAF use and certification?

Piloting how a future SAFc could function and add value is a critical step in Deloitte’s effort to reduce our air travel emissions, and we welcome others to join us. We’d like to thank and acknowledge the airlines for embarking on this journey with us. We hope that our experience can inform and support other organizations in their decision-making processes and that it helps them to articulate why implementing and scaling the SAFc is so critical today.

Get in touch

Lisa Newman-Wise |

Allison Connell |

Duncan Masland |

References

1. Unless otherwise indicated, “we”, “our”, and “Deloitte” refer to Deloitte LLP in the US, not the entire global organization.

2. Electric and hydrogen-fueled planes, although promising, are unlikely to be viable options for larger commercial flights within the next decade.

3. “Clean Skies for Tomorrow: Sustainable Aviation Fuels as a Pathway to Net-Zero Aviation,” World Economic Forum, April 21, 2021, https://www.weforum.org/reports/a356c865-311e-45ca-845d-efe5f762a820

4. Unless otherwise indicated, in this report, we use the term “pilot” to describe Deloitte’s process in purchasing SAF environmental attributes, and SAFc when referring to the future state of the SAF certificate system that we hope our experience detailed here will inform.

5. https://www2.deloitte.com/us/en/pages/about-deloitte/articles/sustainable-aviation-fuel-agreements.html

6. https://www.weforum.org/reports/a356c865-311e-45ca-845d-efe5f762a820

Recommendations

Sustainable aviation fuel agreements

Deloitte enters sustainable aviation fuel agreements

Let's come together

And make a difference for the greater good