Modernizing the three lines of defense model has been saved

Analysis

Modernizing the three lines of defense model

An internal audit perspective

As the risk landscape becomes more complex and fast-moving, it exposes weaknesses in the traditional three lines of defense model. How can internal audit (IA) play a key role in evolving and strengthening this critical risk management framework?

Pressures on the traditional three lines of defense model

Businesses are continuing to evolve out of necessity, responding to an onslaught of disruption, new business models, and technology. This continuous change affects business operations at all levels, with customers demanding real-time interactions, regulators applying increasing levels of scrutiny, and governance stakeholders requiring assurance in this complex and dynamic risk environment. The result has exposed weaknesses in the traditional three lines of defense (3LOD) risk management model.

In its current form, is the 3LOD framework still relevant and efficient? As the risk landscape becomes more complex and fast-moving, it is critical for organizations to identify and respond to emerging risk events quickly and effectively. We believe that internal audit (IA) should play a key role in this evolution.

Current-state challenges with 3LOD

Different groups within organizations play a distinct role within the three lines of defense model, from business units to compliance, audit, and other risk management personnel.

- First line: Management (process owners) has the primary responsibility to own and manage risks associated with day-to-day operational activities. Other accountabilities assumed by the first line include design, operation, and implementation of controls.

- Second line: The second-line function enables the identification of emerging risks in daily operation of the business. It does this by providing compliance and oversight in the form of frameworks, policies, tools, and techniques to support risk and compliance management.

- Third line: The third-line function provides objective and independent assurance. While the third line’s key responsibility is to assess whether the first- and second-line functions are operating effectively, it is charged with the duty of reporting to the board and audit committee, in addition to providing assurance to regulators and external auditors that the control culture across the organization is effective in its design and operation.

While the 3LOD framework is widely acknowledged and understood by a range of industries as the governance model for risk, its implementation varies in form and maturity across the spectrum. Traditionally, the role of IA functions is to provide assurance while maintaining objectivity and independence; however, its mandate should continue to evolve as the need to adapt to a business-focused, technology-driven, advisory mindset is amplified.

Explore the three lines of defense model

Regardless of how mature and integrated the three lines of defense model is within organizations, there are a number of challenges that limit its effectiveness:

• Early-stage adoption – In early stages of the 3LOD framework, management does not have a strong awareness or ownership of risk and controls. There may be a risk function in place, but often its role is to facilitate the maintenance of the risk register, without insight or challenge by IA. Depending on the industry and sector, regulatory compliance risks are absorbed into both risk and IA functions, with specialist teams existing in pockets or one-off "silos" not seen as assurance functions (for example, health and safety in construction firms or clinical governance in the health care industry) nor well integrated within a broader risk management program. In smaller firms, given the similar risk and control skill sets, the IA and risk functions are seen crossing the boundaries between the second and third lines, causing inefficiencies and duplication.

• Established lines of defense – As the 3LOD framework becomes established, the focus on stakeholder management, developing internal capabilities, and delivering the assurance activities in the second-line functions often creates a silo mentality, leading to a lack of coordination, duplication of risk areas, gaps, and misaligned or conflicting assurance opinions. Where these positions become entrenched, the third line is typically perceived as combative, reactionary, and retrospective in its approach. This combination has led to an ineffective 3LOD model, where the board are receiving conflicting and disjointed points of view of its key risks. This challenge was highlighted in Deloitte’s 2018 CAE Global survey, where respondents cited improvements in coordination within the 3LOD as an important business imperative.

• Maturing lines of defense – In the face of increasing regulatory pressure, as well as the opportunity to become more efficient and effective, we are seeing the strengthening of all three lines of defense, being driven from the board focus on emerging risks and core control disciplines. An example of this is in the United Kingdom, where financial services regulators are increasing the personal accountability of senior managers (including executive and nonexecutive directors) over the control environment. The result has been felt across all three lines of defense:

– The first line taking an active role in the management of risk for its area; some are starting to embed first-line monitoring of controls (in larger institutions, this has led to first-line assurance teams–"Line 1b").

– Risk functions are increasingly forward-looking in their assessments of emerging risks, using key risk indicators to highlight potential control failures and working with management to improve the design of controls.

– In addition to advising management on new regulatory risks and designing corresponding policies, compliance functions are undertaking increased regulatory monitoring reviews, which include regulatory controls testing. This is aligned with Deloitte's point of view, where the first and second lines take on greater ownership of their responsibilities as part of "assurance by design" and "automated core assurance."

– This has left IA functions undertaking risk-based assurance reviews over the same risk areas as the second line, increasingly with a very similar assurance skill set, leading to a duplication of assurance activities between the three lines of defense.

While these actionable and strategic steps are oriented towards an evolution in the three lines of defense model, there have been several negative side effects for more mature 3LOD models. The first line can have audit fatigue due to duplicative testing from both second and third lines, resulting in less time to focus on the business at hand. There are also cases where the over fitting or over strengthening of the second line has resulted in issues because the first line stops performing activities, believing they have responsibility of the second line. In times of crisis, many organizations fall into the trap of overreaction, whereby additional activities are added to the portfolio for the second and third lines. In such situations, the third line is best positioned to help their organizations avoid knee-jerk reactions and help draft a measured response that is risk-focused, pragmatic, and practical.

3LOD future state and opportunities

IA functions with the strongest impact in their organizations are those which are adapting to change; collaborating; and making investments in digital assets, analytics, and automation. New technologies have created an opportunity to enable a variety of techniques to improve efficiency and insight from assurance activities, including 100 percent assurance coverage (rather than sampling), automation of assurance tasks, and real-time insight into emerging risks via data-led, continuous monitoring. This creates an opportunity for IA and its future role.

To take advantage of these changes and disruptions, auditors need to rethink their role by adapting to and embracing change, enabling the IA function to become more agile, nimble, and forward-looking, thus driving change through the three lines of defense model.

For IA to be perceived as protecting, building, and preserving value, it needs to truly assure, advise, and anticipate. The IA of the future will play an active role in educating stakeholders and sharing tools, insights, and knowledge. Effective IA functions with a dynamic and forward-looking mindset are likely to be viewed positively by key stakeholders. While the maturity of IA groups within individual organizations will vary, the key is to start identifying current inefficiencies in an organization’s 3LOD model and to encourage innovation with meaningful, strategic steps. Innovation should extend beyond technology, including coordination, communication, audit and risk assessment methodology, and elevating engagement connection with first- and second-line stakeholders. With a renewed vision, IA would be in a better position to strengthen its impact and mobilize itself for future challenges and opportunities.

The road ahead for CAEs and their organizations

IA should focus its efforts on shifting ownership of certain elements of risk management to the first and second lines through education and awareness-building, highlighting the value and efficiencies that can be achieved. This can only help, and assurance, coverage, and clarity will increase. By leveraging digital assets and innovative methods, IA and risk management could automate processes previously covered manually, or not covered at all by the IA plan. IA should increase its participation in coordinating and designing processes that could help management and the second line take ownership of these activities while addressing business risks and minimizing the audit fatigue due to the efforts of second and third line.

In this optimized model, we see the opportunity for real-time assurance, a lower cost structure, and a better span of control across the organization. IA can take a leading role in this effort. IA could create opportunities to help implement assurance activities into controls as they are designed. This approach is called "assurance by design." There is a distinct possibility to automate and create workflows that many of the typical second-line activities and some first-line compliance activities can leverage ("core automated assurance"). This would allow IA (third line) to focus on the greatest risks while creating much-needed capacity.

Looking specifically at IA, this framework represents a traditional view of not only fulfilling IA’s core assurance responsibilities, but also the need to advise on key risks and help the business anticipate and measure risk. There are a number of enablers and accelerators that can be used to achieve these objectives, including:

- Talent; building the workforce of the future; and considering what type of work needs to get done, who is going to do the work, and where the work is going to be performed

- Developing new and innovative approaches for assessing risk, how audits are performed and delivered, and reporting results

- Utilizing and integrating digital assets into business as usual

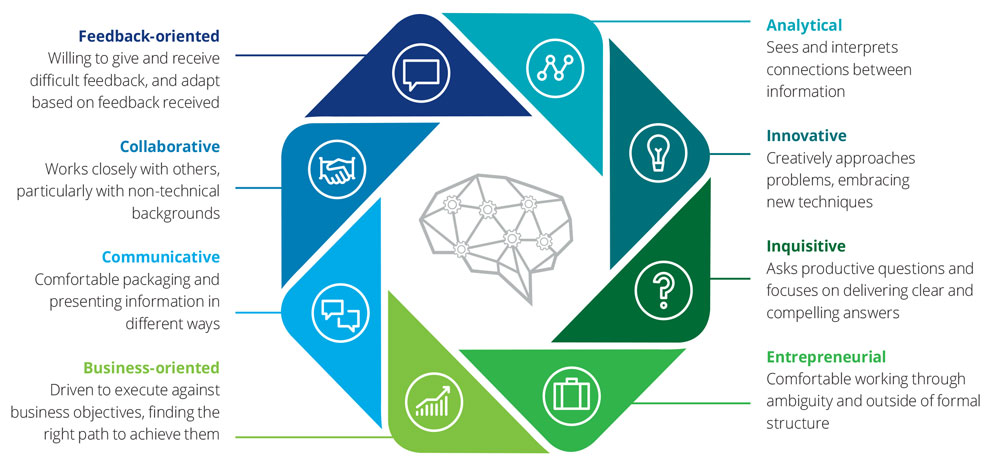

In addition, the CAE should focus on the IA function in considering the importance of developing an innovative mindset. This is critical for organizations as they look to the future and develop forward-looking approaches for managing risk. The CAE should think about the skills and attributes that drive innovative behavior. It is interesting that the skills and characteristics in many ways are the same for what an innovative risk and control professional will need to be impactful in the future.

Internal audit of the future: Inside an innovative mindset

New possibilities for IA

IA is at the cusp of innumerable possibilities to collaborate with the other lines in the three lines of defense model, develop roadmaps, and help improve governance across the organization. Here is a great opportunity for the profession to redefine itself and cement its position as not only a provider of assurance, but also a function that assures, advises, and anticipates. Our point of view represents fulfilling assurance responsibilities with combined core assurance spread throughout the lines of defense, rather than just through IA, but also includes the imminent need for IA to advise the business with anticipation and measurement of risk. These are the critical elements of the IA of the future (see Deloitte POV: Internal Audit 3.0), which will create capacity for IA to focus on the truly most relevant and impactful risks to the organization.

Get in touch

Recommendations

What does an optimal risk management operating model look like?

Managing operational risk and compliance: New paradigms for synergy

Connect. Modernize. Digitize. Take command of risk

A strategic way to build resilient organizations