Understand the accounting requirements in ASC 410 has been saved

Perspectives

Understand the accounting requirements in ASC 410

On the Radar: Environmental and ARO accounting

Environmental obligations can arise from the improper operation, retirement, or closing of a facility and the current or former ownership of a facility at or near a contaminated site. An asset retirement obligation (ARO) is a legal obligation associated with the retirement of a tangible long-lived asset. This On the Radar edition gives guidance on the accounting requirements established for both in ASC 410-30 and ASC 410-20, respectively.

On the Radar series

High-level summaries of emerging issues and trends related to the accounting and financial reporting topics addressed in our Roadmap series, bringing the latest developments into focus.

Understanding environmental obligations and asset retirement obligations

Environmental obligations can arise from (1) the improper operation, retirement, or closing of a facility and (2) the current or former ownership of a facility at or near a contaminated site. Entities that have incurred a legal obligation to remove or remediate pollution or contaminants from environmental media such as soil, sediment, groundwater, and surface water are generally required to recognize an environmental remediation liability in their financial statements when certain conditions are met.

An asset retirement obligation (ARO) is a legal or contractual obligation associated with the retirement of a tangible long-lived asset that results from the acquisition, construction, development, and normal operation of that long-lived asset.

The FASB has established specific guidance on accounting for environmental obligations and AROs in ASC 410.

On the Radar: Environmental obligations and asset retirement obligations

Liabilities and obligations

The FASB’s guidance on accounting for environmental remediation liabilities is codified in ASC 410-30, and the recognition and disclosure guidance is principally based on a framework outlined by the guidance on loss contingencies in ASC 450-20. Environmental remediation liabilities are a specific type of contingent liability that arises from federal, state, and local environmental regulations—or, in some instances, international treaties—related to contamination in soil, sediment, groundwater, and surface water.

In the United States, the US Environmental Protection Agency (EPA) is the primary, though not the only, environmental regulator. Other federal, tribal, state, or local agencies may also have authority to regulate environmental programs. The guidance on accounting for environmental liabilities classifies laws into two categories: (1) environmental remediation liability laws and (2) laws intended to control or prevent pollution. The following are some of the main federal regulations that serve as drivers of environmental liabilities:

- Clean Air Act of 1970 (CAA)

- Clean Water Act of 1972 (CWA)

- Toxic Substances Control Act of 1976 (TSCA)

- Resource Conservation and Recovery Act of 1976 (RCRA)

- Comprehensive Environmental Response, Compensation, and Liability Act of 1980 (CERCLA, also known as “Superfund”)

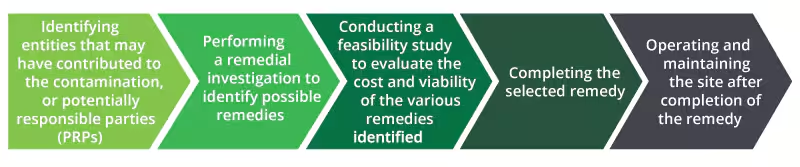

As with other contingent liabilities, an environmental remediation liability is recognized when it is probable that such a liability has been incurred and the amount of the liability can be reasonably estimated. There is often uncertainty about whether and, if so, when a legal obligation for environmental remediation has been incurred. The existence and amount of an environmental remediation liability often become determinable over a continuum of events and activities. A typical environmental remediation process consists of the following steps:

ASC 410-30 provides specific benchmarks for an entity to consider when evaluating the probability of a loss and the extent to which any loss is reasonably estimable. One such benchmark requires recognition of an environmental liability once a feasibility study is substantially complete, which is no later than when the PRPs recommend a proposed course of action to the EPA. Sometimes the EPA performs and completes its own feasibility study in lieu of, or in addition to, a PRP-conducted feasibility study. Thus, a PRP-recommended course of action may not always take place, or it may occur after the EPA’s completion of a feasibility study and related recommended course of action.

We believe that if the EPA completes a feasibility study for a particular site before PRPs have recommended their proposed course of action, the ASC 410-30 recognition benchmark is met and a liability must therefore be recognized at the time the EPA completes the feasibility study.

When the recognition criteria are met, entities initially measure environmental remediation liabilities at the estimated cost of remediating the site; generally, environmental remediation liabilities are not discounted unless certain conditions are met. Estimated remediation costs are continually updated, and the recorded liability is adjusted prospectively until the obligation is settled.

In a manner consistent with the guidance in ASC 450-20 and ASC 275 on other loss contingencies and uncertainties, entities are required to disclose the existence of environmental remediation loss contingencies when it is at least reasonably possible that a loss has been incurred regardless of whether the loss is reasonably estimable. Additional disclosure requirements exist for recognized environmental remediation loss contingencies.

Unlike an environmental liability, which results from the improper use of a long-lived asset, an ARO exists when an entity has an unconditional obligation associated with the retirement of a tangible long-lived asset used under normal operations. Like environmental obligations, AROs can arise from an existing or enacted law. However, unlike many environmental obligations, AROs can also arise (1) from statute, ordinance, or written or oral contract or (2) by legal construction of a contract under the doctrine of promissory estoppel.

Entities should evaluate the existence of legal obligations on the basis of current laws, regulations, contractual obligations, and related interpretations and facts and circumstances and should not forecast changes in laws or interpretations of such laws and regulations. The impacts of changes in laws or regulations should be considered in the period in which such laws or regulations are enacted.

An ARO is recognized at fair value when incurred or when a reasonable estimate of its fair value can be made. An asset retirement cost (ARC) is recorded by increasing the associated long-lived asset’s carrying value. The ARC is depreciated over the useful life of the long-lived asset. An ARO liability is discounted and recorded at present value, and accretion of an ARO liability due to the passage of time is recognized as a component of operating expense. Revisions to the estimated timing or amount of cash flows associated with the retirement activities are recognized as an increase or decrease in the carrying amount of the ARO and the related ARC.

Entities often incorporate the use of internal resources into their remediation plans. The guidance in ASC 410-20 requires the amounts included in the ARO cash flow estimate to reflect costs that a third party would incur to conduct retirement activities. Therefore, in addition to internal resources, entities need to consider incremental costs (e.g., overhead, equipment charges, profit margin) to ensure that the amounts included in the ARO cash flow estimate reflect costs that a third party would incur. Accordingly, if an entity settles the ARO by using its own internal resources, the incorporation of third-party and marketplace assumptions into the estimate of ARO cash flows and the initial measurement of the ARO will most likely result in the recognition of gains upon the settlement of the ARO.

Application of the guidance in ASC 410-20 can be complex and requires significant management estimates and judgment. For example, determining whether a legal obligation to retire a long-lived asset has been incurred may not always be clear and unambiguous. If an entity makes a promise to a third party, including the public at large, about its intentions to undertake asset retirement activities, significant judgment may be required in the determination of whether the entity has created a legal obligation under the legal doctrine of promissory estoppel, which is defined in ASC 410-20-20 (citing Black’s Law Dictionary, seventh edition) as the “principle that a promise made without consideration may nonetheless be enforced to prevent injustice if the promisor should have reasonably expected the promisee to rely on the promise and if the promisee did actually rely on the promise to his or her detriment.”

Driven by investor demand, stakeholder pressures, and, more recently, regulatory attention, companies are increasingly focused on climate-related and environmental matters. In addition, climate change has been a central topic of U.S. policy discussions in many government departments and agencies. In the current and forthcoming regulatory environment, it will be essential for companies to closely monitor their environmental obligations under new or changing laws and regulations.

EPA’s final rule on legacy CCR surface impoundments and CCR management units

On May 8, 2024, the EPA’s final rule on legacy coal combustion residuals (CCR) surface impoundments and CCR management units (CCRMUs) was published in the Federal Register. The three main elements of the final rule are as follows:

- Legacy CCR surface impoundments — The final rule introduces a definition for legacy CCR surface impoundments, which are inactive surface impoundments at inactive power plants. These impoundments must adhere to the same regulations as inactive CCR impoundments at active power plants, barring location restrictions and liner design criteria, with customized compliance deadlines.

- CCRMUs — The final rule stipulates groundwater monitoring, corrective action, closure, and post-closure care requirements for CCRMUs, which are at active and inactive power plants with a legacy CCR surface impoundment. CCRMUs include CCR surface impoundments and landfills closed before October 19, 2015, and inactive CCR landfills.

- Facility evaluation reports (FERs) — The final rule mandates new reporting requirements. The owners and operators of legacy CCR surface impoundments must prepare FERs that identify and describe the CCRMUs. In a manner consistent with existing CCR rules, facilities must publish FERs on their CCR websites in two parts, within 15 months (part 1) and 27 months (part 2) of the final rule’s effective date.

Climate and sustainability matters

On March 6, 2024, the SEC issued a final rule that requires registrants to provide climate-related disclosures in their annual reports and registration statements. Specifically, registrants must disclose certain climate information in the notes to the financial statements and outside the financial statements. For example, in the footnotes to the financial statements, a registrant must disclose (1) financial statement impacts due to severe weather events and other natural conditions, including the aggregate expenditures incurred, losses recognized, and capitalized costs and charges, subject to certain thresholds; (2) a rollforward of carbon offsets or renewable energy certificates (RECs) if the registrant’s use of carbon offsets and RECs is a material component of its plan to achieve its disclosed climate-related targets or goals; and (3) whether and, if so, how severe weather events and other natural conditions and disclosed climate-related targets or transition plans materially affected estimates and assumptions reflected in the financial statements. Large accelerated filers and accelerated filers must provide disclosures outside the financial statements about their material scope 1 and scope 2 greenhouse gas (GHG) emissions, subject to assurance requirements that will be phased in. In addition, all registrants, regardless of filer status, are required to disclose outside the financial statements (1) governance and oversight related to material climate-related risks; (2) the material impact of climate-related risks on the company’s strategy, business model, and outlook, including material expenditures and impacts related to targets, goals, and related activities or mitigation; (3) the risk management processes for material climate-related risks; and (4) material climate targets and goals.

On April 4, 2024, the SEC voluntarily stayed the effective date of the final rule pending judicial review of petitions challenging it, which have been consolidated for review by the US Court of Appeals for the Eighth Circuit. For more information about the final rule, see Deloitte’s March 6, 2024 (updated April 8, 2024), and March 15, 2024 (updated April 8, 2024), Heads Up newsletters.

Concurrently with the SEC’s rulemaking activities related to climate disclosures, its Division of Corporation Finance (the “Division”) has continued to issue comment letters to registrants in various industries regarding climate-change disclosures. The Division has publicly released such comment letters and registrants’ responses to them.

Many companies are publicly committing to achieve environmental goals related to climate change and sustainability. Public commitments about intentions to undertake a certain course of action with respect to asset retirement activities can result in an entity’s incurrence of an ARO that must be recognized in the financial statements under the doctrine of promissory estoppel. Companies should carefully monitor and evaluate their public commitments and work closely with legal counsel to evaluate their own specific circumstances in determining whether legal obligations have been incurred.

Continue your environmental obligations and asset retirement obligations learning

Deloitte’s Roadmap Environmental obligations and asset retirement obligations comprehensively discusses the recognition, measurement, presentation, and disclosure guidance in ASC 410-20 and ASC 410-30.

Subscribe to the Deloitte Roadmap Series

The Roadmap series provides comprehensive, easy-to-understand guides on applying FASB and SEC accounting and financial reporting requirements.

Explore the Roadmap library in the Deloitte Accounting Research Tool (DART), and subscribe to receive new publications via email.

Let's talk!

Learn more about this topic

Ashley Carpenter

Senior Consultation Partner | Audit & Assurance

Get in touch for service offerings

Jamie Davis

Partner – Audit & Assurance | Deloitte & Touche LLP

Recommendations

Accounting for GHG emissions

On the Radar: Greenhouse gas protocol reporting considerations

Accounting & financial reporting roadmap

Find comprehensive guides to help you face your most pressing accounting and reporting challenges with clarity and confidence.