Artificial intelligence: An emerging oversight responsibility for audit committees? has been saved

Perspectives

Artificial intelligence: An emerging oversight responsibility for audit committees?

As published in NACD’s ‘2024 Governance Outlook’

Recent developments in artificial intelligence (AI), including the emergence of Generative AI, are leading businesses to evaluate AI’s potential impact to their business technology strategy. As businesses expand their use of AI, especially into core business processes, the audit committee will need to understand the challenges and opportunities presented by AI to address risks related to governance and stakeholder trust.

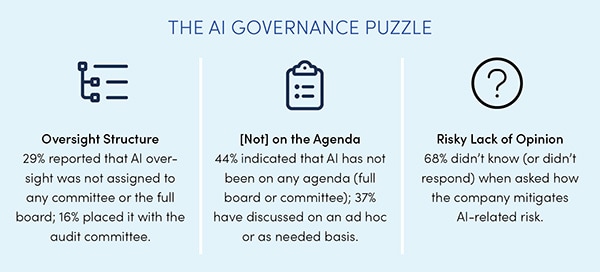

Who’s minding the AI store now?

According to a 2023 survey conducted by Deloitte and the Society for Corporate Governance, corporate secretaries see AI strategy and oversight as still evolving. The findings show that few respondents (13%) had a formalized AI oversight framework, although many (36%) were considering the development and implementation of AI oversight policies and procedures.

These results are particularly interesting when compared to a 2022 Deloitte survey, in which 94 percent of respondents said AI was critical to their company’s short-term success.1 This may suggest some level of information asymmetry between management and the board, congruent with the notion that AI is in a state of flux. Thus, at least for now, the AI landscape might best be characterized as an abstract governance puzzle.2

Familiar and different set of risks

With new technology comes the possibility of new risks. Some AI risks present well-trodden challenges that arise in other technology areas and can be overseen and understood in the context of an ongoing enterprise risk management (ERM) process,3 such as the COSO ERM framework. However, other risks may be unfamiliar and/or amplified. Some examples include shadow IT environments, IP ownership and infringement, and cybersecurity bad actors.

With risks come benefits, too

If AI presented nothing but risk, it seems unlikely that it would have emerged as “the” technology of the future. Clearly, AI has benefits, some of which may not be known for some time. One particular set of benefits is squarely in the audit committee’s wheelhouse—namely, the potential to streamline and enhance a company’s internal audit, financial reporting, and internal control functions. There are also aspects of generative AI technology that, while still evolving, may one day fundamentally change an organization’s financial systems. While there is much uncertainty, the future transformative potential of generative AI may add much to the current array of use cases. In the shorter term, various subcategories of AI are already capable of improving the quality of financial reporting via reviewing transactions, identifying errors, addressing internal control gaps, and detecting fraud. If AI isn’t being used within these areas, the audit committee might ask if the company is exploring potential use cases—and if the company is not, the committee might ask to hear the reasons behind that decision.

AI and the audit committee

An important part of the AI governance puzzle for the audit committee is assessing risk. But, at least for now, this task is currently made more difficult by a shifting regulatory landscape.

Governments and regulators around the world are considering whether regulation and policy can address AI risks. Their progress toward developing and enacting policies and regulations over AI is uneven across the globe and in different stages of development and enactment. And to make things more complex, stakeholder groups—shareholders, customers/clients, employees, suppliers, and community—all have varying and sometimes conflicting expectations around use and governance of AI. For these reasons, there may be a benefit to continuously assessing AI risks and benefits over waiting for emerging and future legislative proposals or regulatory guidance. But to accurately make such continual assessments, it’s important that the audit committee and the board have sufficient knowledge to ask questions around the organization’s adoption and use of AI.

The following questions may be a good place to start the audit committee’s dialogue about AI strategy and governance.

- What are the company’s current and potential future use cases for AI, and do any of them have an impact on financial reporting or other audit committee oversight areas?

- Has management considered opportunities to use AI that may enhance or improve financial reporting processes?

- What processes are, or will be, used to evaluate dependencies that may arise in other areas where the audit committee may have primary oversight, like cybersecurity or data management?

- Are processes for use of AI congruent with the company’s risk appetite in terms of level of proactiveness and mitigation strategy?

- Given the speed of AI technology development, are existing processes being assessed and updated with appropriate frequency?

Artificial Intelligence: An Emerging Oversight Responsibility for Audit Committees?

1 Business leaders were defined as company representatives who met one or more of the following qualifiers: (1) responsible for AI technology spending or approval of AI investments, (2) responsible for the development of AI strategy, (3) responsible for implementation of AI technology, (4) acting as AI technology subject-matter specialist, or (5) otherwise stated they were influencing decisions around AI technology. See Nitin Mittal, Irfan Saif, and Beena Ammanath, Fueling the AI transformation: Four key actions powering widespread value from AI, right now, State of AI in the Enterprise, 5th Edition report, Deloitte, October 2022.

2 Natalie Cooper, Bob Lamm, and Randi Val Morrison, "Future of tech: Artificial intelligence (AI)," Board Practices Quar¬terly, Deloitte, August 2023.

3 Alexander J. Wulf and Ognyan Seizov, "'Please understand we cannot provide further information': Evaluating content and transparency of GDPR-mandated AI disclosures," AI & Society (2022).

5 Vic Katyal, Cory Liepold, and Satish Iyengar, “Artificial intelligence and ethics: An emerging area of board oversight responsibility," On the Board’s Agenda, Deloitte, 2020.

Get in touch

Carey Oven

Enterprise Leader Development & Succession | Deloitte & Touche LLP

Krista Parsons

Managing Director and Audit & Assurance Governance Services and Audit Committee Program Leader | Center for Board Effectiveness | Deloitte & Touche LLP

Recommendations

On the Audit Committee's Agenda

Top of mind topics for audit committee members

Audit Committee Guide

This guide helps audit committee members and management better understand the requirements, roles, and responsibilities of the audit committee.