Small business banking is #trending has been saved

Perspectives

Small business banking is #trending

The future of the small business banking market

We’re in the age of startups. Driven by new tech, limited barriers to entry, and changing workforce models, small businesses make up 99.9% of US companies. How can banks revamp their services—from small business loans to financing—to match startup agendas? Those who keep up with current banking trends are well-positioned to win small business.

It’s time to rethink how you address the small business banking market

The small business banking experience is currently fragmented and typically requires in-person interactions, even for simple banking needs. This presents an opportunity for banks to overhaul their processes and capitalize on a pivotal moment to acquire new customers, all while staying compliant with regulations. As things stand, there are barriers to small businesses in acquiring financial services online.

- Most traditional banks have limited online capabilities, with digital applications serving primarily as customer inquiry and initial app intakes, requiring banker follow-ups.

- A high number of traditional banks require an in-person consultation to open small and medium banking (SMB) deposit accounts and credit cards.

- Many banks that have enabled online account opening for small business customers have not invested beyond the account opening experience.

- The number of physical bank branches is on a steep decline. By 2034, there are projected to be less than 16,000 branches in the United States.

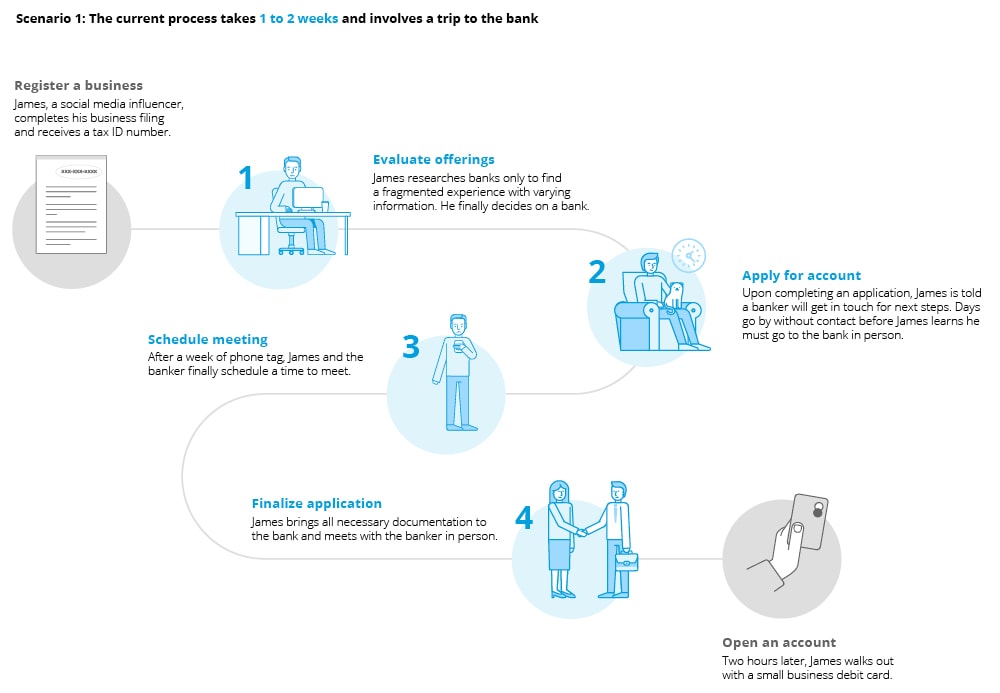

In today’s marketplace, a realistic experience for a small business might play out like Scenario 1 below.

Trends driving the future of small business banking

Addressing the realities painted above in Scenario 1 requires a massive overhaul of the current small business banking market. Banks need to be in line with the digital speed of other experiences small business entrepreneurs are encountering, and they need to build a digital experience that removes the need to meet in branch. An effective customer experience for small and medium-sized enterprises (SMEs) requires instant time to decision, experiences driven by the SME growth journey, niche offerings, and more.

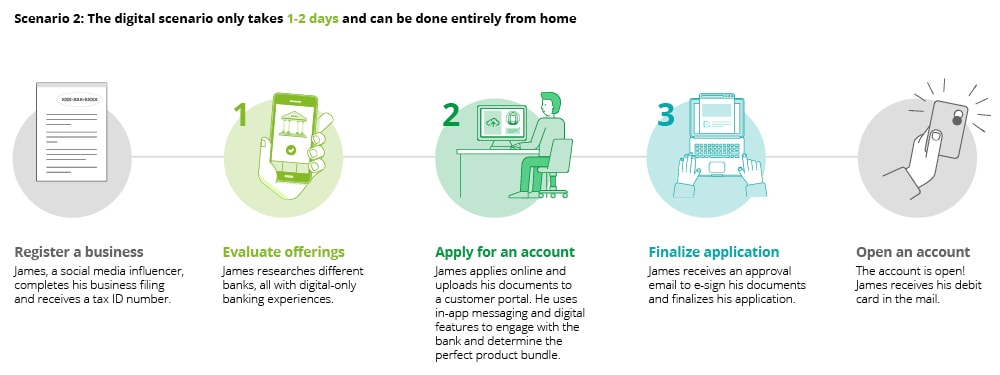

In Scenario 2, we see the future of small business banking: A seamless digital experience that takes days instead of weeks, done entirely from home.

Download our full report for a detailed look at how banks can transform their digital experiences to match current trends and meet rising small business customer expectations.

Get in touch

Do you have specific questions about digital banking and small business? Our team of experts is on standby. Contact us to stay on trend.

Contacts

Joseph Cody

Principal

Digital Banking Solutions Leader

Deloitte Consulting LLP

jcody@deloitte.com

Jon Guerena

Managing Director

nCino Practice Lead

Deloitte Consulting LLP

jguerena@deloitte.com

Stephen Popiela

Senior Manager

Offering Lead

Deloitte Consulting LLP

spopiela@deloitte.com

Evan Weinreb

Manager

Digital Banking Solutions

Deloitte Consulting LLP

eweinreb@deloitte.com

Recommendations

Buy vs. build for banking technology

Which is the best path for bank digital transformation?

Artificial intelligence in capital markets

Leveraging AI to optimize post-trade processes