The agile advantage: Moving transformations from unknowns to outcomes has been saved

Perspectives

The agile advantage: Moving transformations from unknowns to outcomes

CFO Insights

In this edition of CFO Insights, we will try to demystify agile and share some practical considerations for improving your capabilities to adopt an agile approach to transformation.

Explore content

- Introduction

- Confronting unknowns with agility

- What can CFOs do to support agile?

- Endnotes

- Get in touch

Introduction

CFOs are increasingly at the center of major transformation efforts—as sponsors, leaders, or co-leaders. These enterprise or finance transformation efforts can be complex, multi-dimensional, and subject to many unknowns and uncertainties (see “What changes in a transformation—and why it matters to CFOs,” CFO Insights, January 2020).

For example, if you build it, will they (customers) come? If you are pivoting more sales to eCommerce channels, as many companies did during the pandemic, which approach to pricing, subscriptions, and user interfaces will engage customers effectively to drive sales? If you are introducing a new reporting and forecasting system that requires greater self-service by the businesses, will the business users modify their behaviors to actually use the system?

Given such uncertainties—usually in customer, employee, supplier, and ecosystem partners’ behaviors and preferences—traditional planning, user requirements specification, and development models may be too slow and fail to generate the desired outcomes from today’s transformation efforts. In response, some organizations are adopting an agile approach to executing transformation initiatives to achieve tangible and valued outcomes.

What is agile? More than a synonym for flexibility, agility is a mindset that acknowledges the future has significant unknowns and offers a set of execution practices that adapt to and resolve the unknowns, leading to tangible outcomes. While a methodology such as Waterfall stresses a pre-planned, rigid, linear approach to development, agile enables teams to implement small or short chunks of work and change direction based on results of that work.

Still, scaling agile to broader transformations poses distinct challenges for CFOs and finance organizations. Funding models, typically based on annual budgets, may need restructuring to reflect the incremental aspect of agile’s multi-stage approach to delivering early, measurable ROI to the business.1 Moreover, both finance and partner organizations may have to change—in mindsets, behaviors, and processes—to effectively enable more transformative enterprise and functional shifts.

In this edition of CFO Insights, we will try to demystify agile and share some practical considerations for improving your capabilities to adopt an agile approach to transformation.

Confronting unknowns with agility

In a traditional approach to transformation, a company may hatch plans that can easily devour at least a year’s worth of time before key stakeholders begin to see change. But during the year, the situation can change, rendering assumptions about the future of markets, technology, or customer behavior obsolete. This can lead to execution efforts that do not match ground-level realities and fail to realize substantial value.

In contrast, the prerequisite to an agile approach is to adopt an open mindset that disposes of fixed preconceptions about the future. This includes making sure previously devised plans and agendas aren’t clouding the view of either new pertinent information or unexpected opportunities. Agile leaders acknowledge that what is ahead is not just immediately unknown, but may even be unknowable. Instead, they take complex projects and break them into short phases (two-to-four-week “sprints,” in agile parlance), soliciting feedback either internally or from customers to come up with potentially deliverable products along the way.

By constantly solving problems, project teams continuously learn and shape longer-term solutions and deliver transformational change—whether they involve transforming customer relationships or driving new processes and systems to generate cost-savings or other benefits (see Figure 1).

Beyond the mindset, there are four key practices essential to agile transformation:

- Envision and activate a transformation ambition. First, have a clear transformation ambition. Transformations are not small change; they are usually significant and ambitious. For example, a software company may have the following ambition as it shifts business models: “We will grow our revenues and flip our revenue mix from 70% products and 30% subscriptions to the reverse in the next two years, while delighting customers with better experiences.” This statement sets forth a clear objective for change that can be communicated and cascaded through the organization and embedded into objectives and key results (OKRs) and other outcome metrics (for more, see “Crafting your transformation ambition,” CFO Insights, March 2020).

- Focus on sprints with well-defined outcome metrics. A second key practice is to break the project down into small units of work. Using a popular agile methodology called “scrum,” sprints are executed with clear outcome metrics. Instead of planning for a year-long project, the work is broken down into short sprints that could be as brief as one week, with defined objectives, such as a more user-friendly interface for the client website. This can then be A/B tested simultaneously with the prior interface to see if users prefer the new format. Short sprints with well-defined and tangible goals drive the possibility of realizing desired results within a fixed period of time. In addition, focusing on tangible outcome metrics, such as measurable shifts in consumer behavior, instead of team output metrics (e.g., lines of code or sales metrics) allows projects to deliver near-term tangible results that work toward enabling desired future outcomes.

- Organize teams for speed and ownership of outcomes. Another key difference in implementing the agile method is to organize around teams that have all the competencies to deliver on an outcome and to free up their time to deliver. Essentially, the team should be able to go from “concept to cash or the desired outcome.” This means breaking through functional and vertical silos and assembling a horizontal team that is empowered to make decisions and deliver. Ideally, the teams are small or “two-pizza” teams to reduce hand-offs across groups and coordination costs or delays. The teams also need to be empowered and psychologically safe to take actions that drive outcomes. Leaders can help these teams by clearing obstacles, providing that psychological safety, and relinquishing a command-and-control model. Instead of being deadline driven and project managed, the teams need the license to self-manage to deliver outcomes and the ability to speak out on what outcomes cannot realistically be delivered.

- Sprint, assess, stop, or pivot forward. Sprints are by essence short distance races; in agile efforts, sprints address a narrow scope of work that enables focus and faster execution. By breaking down work on transformation into small chunks with clear outcomes or with outcomes that resolve prior uncertainties, teams can leverage the learnings to adapt strategy going forward. Small chunks of work in a fixed time frame also minimizes work-in-progress inventory and can enable more predictable costs for the sprint’s duration. Finally, the process of sprint, assess, stop, or pivot forward can reduce overall project failure risks. This process quickly determines what can, and cannot, work, thereby allowing teams to halt unproductive courses of action. Moreover, continuous reassessment of progress toward the outcome and stopping sprints as needed allow teams to resolve critical uncertainties and focus resources on pathways most likely to yield favorable results.

What can CFOs do to support agile?

At the outset, some CFOs may be uncomfortable with agile given its improvisational nature. Adopting agile may also create challenges in existing processes for identifying and classifying capital expenditures versus operating expenses2. Consequently, we recommend considering an agile approach to building agile capabilities.

Start with one or two small agile teams to address a few key problems and deliver outcomes within a fixed time frame and budget. Learn from how these teams perform to make adjustments for deploying future teams. Align a finance resource to these teams—not to set project deadlines or say “no” to resources—but to observe, work out ways of recording expenses and capital expenditures, seek additional budget if needed, and provide input on future sprints.

To be clear, using agility does not mean abandoning rigor. All the necessary checks and balances that happened before should happen again; the difference is that they may be embedded in the agile process, for example, as part of the detailed quarterly planning process where changes are reviewed or embedded in the guardrails that define the team’s boundaries.

Based on the performance of the teams, the choice to scale agile transformation may lead to creating an agile activation office to coordinate efforts, share knowledge, and track multiple team efforts. Over time, CFOs may also reserve a portion of their annual budgets for agile projects. Rather than tugging on budgetary constraints like a leash to keep projects from incurring runaway costs, CFOs can leverage these resources to empower agile teams by transparently linking short-term funding to specific outcome objectives and metrics. This requires a move away from fixed annual budget planning to continuous allocation of resources to agile teams as deemed necessary.

By implementing agile methods and practices, CFOs can navigate transformation uncertainties through a series of small “sprints” that clarify the best ways to valued outcomes. As the company develops experience with this way of accomplishing change, it can scale efforts as needed for broader transformation efforts.

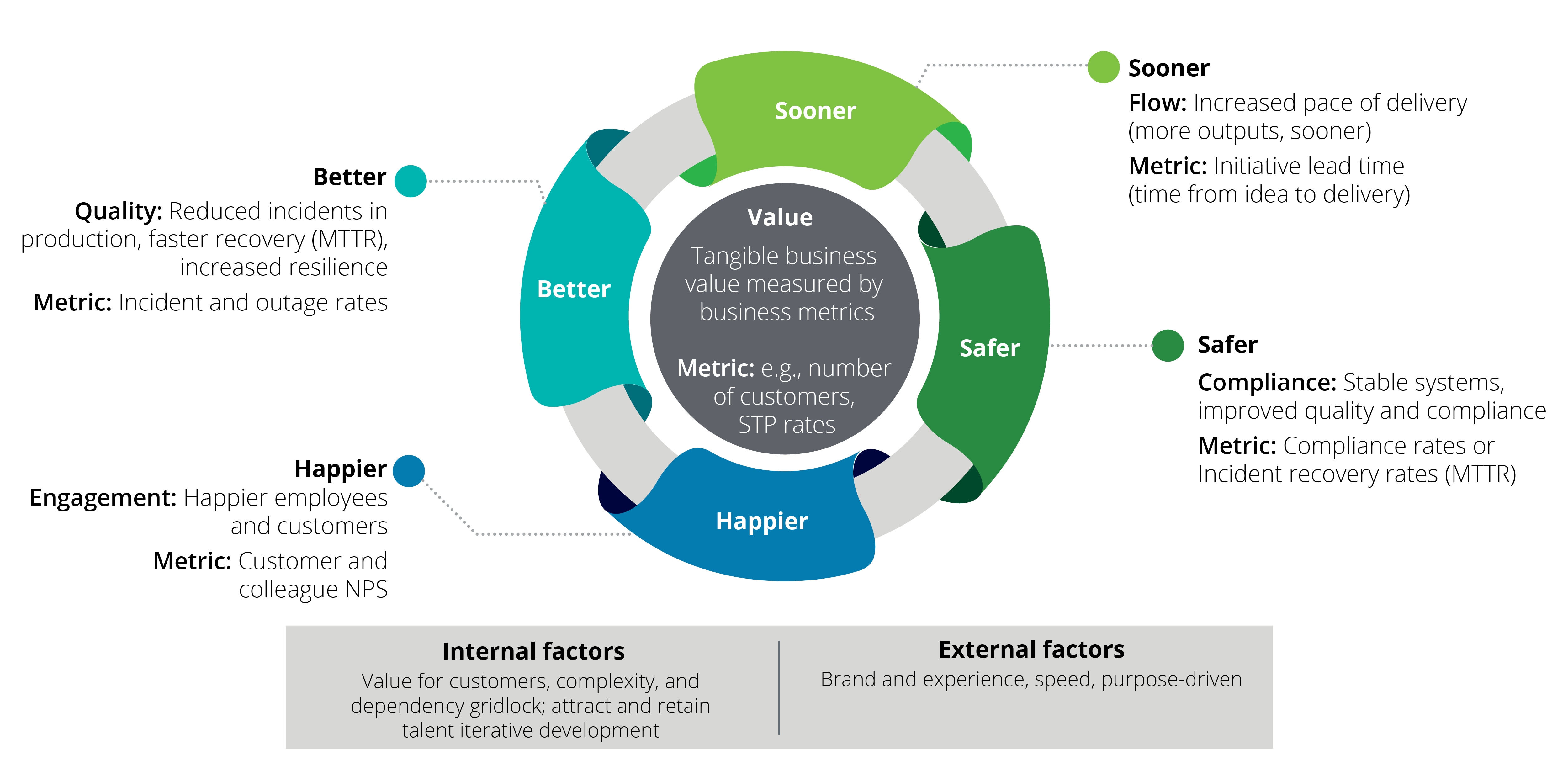

Figure 1: An agile definition of success

Success is measured through the lens of continuous value—"Better, Value, Sooner, Safer, Happier"—and not through project lenses on requirements, budget, and time

Source: “IT 2025: Collaborating on the digital shift,” CFO Program, Deloitte LLP

Endnotes

1 “Accounting for Costs Incurred in the Application of Agile Software Development,” Accounting Spotlight Newsletter, Deloitte Development LLC , May 2020.

2 Ibid.

CFO Insights, a bi-weekly thought leadership series, provides an easily digestible and regular stream of perspectives on the challenges you are confronted with.

View the CFO Insights library.

About Deloitte's CFO Program

The CFO Program brings together a multidisciplinary team of Deloitte leaders and subject-matter specialists to help CFOs stay ahead in the face of growing challenges and demands. The Program harnesses our organization’s broad capabilities to deliver forward-thinking and fresh insights for every stage of a CFO’s career—helping CFOs manage the complexities of their roles, tackle their company’s most compelling challenges, and adapt to strategic shifts in the market.

Learn more about Deloitte’s CFO Program.

Deloitte CFO Insights are developed with the guidance of Dr. Ajit Kambil, global research director, CFO Program, Deloitte LLP; and Lori Calabro, senior manager, CFO Education & Events, Deloitte LLP. Special thanks to Josh Hyatt, manager/journalist, CFO Program, Deloitte LLP, for his contributions to this edition.

Recommendations

CFO Signals™: Q1 2021

After a tough year, CFOs express increased optimism and expectations for economic growth