Consumer banking remade by COVID-19 has been saved

Perspectives

Consumer banking remade by COVID-19

Scenarios for resilient leaders

There are various scenarios exploring how the COVID-19 pandemic could accelerate or redirect the consumer banking industry over the next one to three years. These scenarios target consumer banks and are built on important macro and banking sector uncertainties—both already evident and others potentially plausible based on the severity of the pandemic and government actions. These decisions could ultimately spark several questions around implications and next steps for your organization.

Explore content

In the wake of COVID-19, Deloitte and Salesforce hosted a dialogue among some of the world's best-known scenario thinkers to consider the societal and business impact of the pandemic. The results of this collaboration can be found in The World Remade: Scenarios for Resilient Leaders.

The consumer banking industry remade

How might consumer banking evolve in the coming years, and how can leaders be prepared? Insights on how consumer banking in the US might evolve in the next one to three years to help leaders:

- Explore how uncertainties during the pandemic could shape US consumer banking in the medium term.

- Have productive conversations on the lasting implications and impacts of the crisis.

- Identify decisions and actions that will improve US banks’ resilience to the rapidly changing landscape.

- Move beyond responding to the crisis, and towards recovering in the medium term.

We are in uncharted waters; yet, banking leaders should take decisive action to help ensure their organizations are resilient. Deloitte’s Resilient Leadership framework defines three time frames of the crisis.

Consumer banking remade by COVID-19

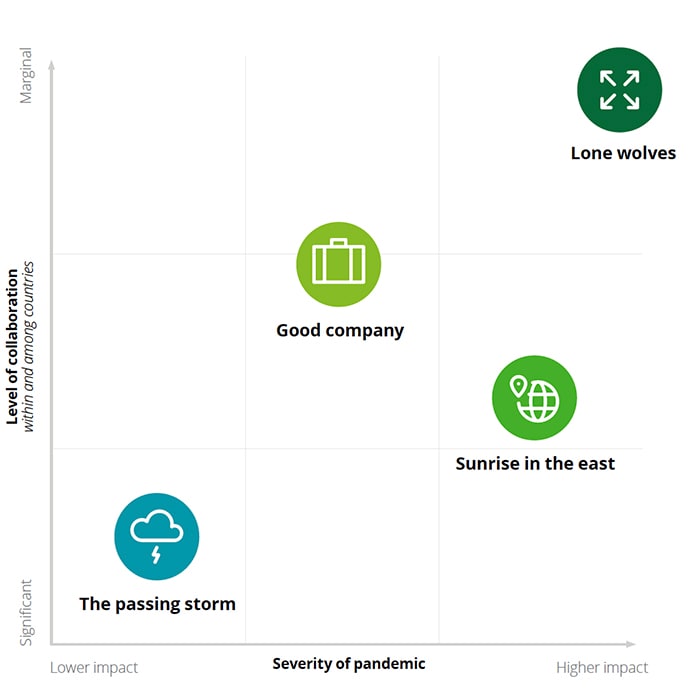

Four COVID-19 banking scenarios as thought starters

Four distinct scenarios emerge based on current trends and critical uncertainties. They are summarized below, and more details can be found in the attached PDF:

Two critical uncertainties will drive the overall impact of COVID-19:

- What is the overall severity of the pandemic and pattern of disease progression?

- What is the level of collaboration within and between countries?

The pandemic is managed due to effective responses from governments to contain the virus, but is not without lasting repercussions, which disproportionately affect SMBs and lower- and middle-income individuals and communities.

- Relatively constrained disease dynamic.

- Effective health system and policy response.

Banking system

- Strong policy response prevents structural damage to the banking industry and leads activity to recover to positive growth within one to two years.

- Most mid-tier and community banks weather the storm due to both their strong capital reserves and effective government actions (including the CARES Act) designed specifically to support them.

- Challenger banks and noncharter financial institutions are shaken due to their lack of liquidity and capital access, driving regulators to further scrutinize these players.

- Market consolidation continues and accelerates slightly above the pre-crisis rate.

- Increased collaboration between countries leads to further convergence of global banking regulations around open banking and data sharing, placing more control into the hands of customers.

Governments around the world struggle to handle the crisis alone, with large companies stepping up as a key part of the solution and an acceleration of trends toward “stakeholder capitalism.”

- More prolonged pandemic.

- Collaboration to control the pandemic led by large companies.

Banking system

- Demand for nonloan banking services recovers slowly and trust in banking institutions increases; leads to higher demand post-crisis and engages less price-sensitive customers.

- Regulators loosen regulations to support flow of credit to the communities. Regulators are supportive of big tech, challenger banks, and other new entrants who heavily use technology and have low cost structures.

- Increased trust in “good companies” results in customers willing to share data more broadly, which gives players who are able to drive insights and value an advantage over competitors.

- Challenger banks and other niche players lean in and benefit from the rising tide of trust for institutions. Rising trust levels provide increased access to data, which further drives and sets the pace of innovation.

- Prolonged pandemic and economic downturn lead to a fundamental shift in the balance of market power as M&A activity, from nontraditional players, impacts existing market structures.

China and other East Asian nations are more effective in managing the virus and take the reins as primary powers on the world stage.

- Severe pandemic.

- Collaborative health response led by East Asian countries.

Banking system

- Slow recovery and long-term near-zero interest rates result in muted balance sheets and a smaller banking profit pool, driving increased market consolidation particularly among small- and mid-sized banks.

- US banking policy shifts towards less protectionism and greater convergence with international rules (e.g., open banking), as better economic conditions abroad lead to a decline in investment capital in the US and a greater desire for foreign investment.

- The largest East Asian banking and technology ecosystem players begin to make plans to penetrate the US markets.

- Customers, hurt by the crisis, increasingly seek to optimize their financial situation as they search for yield. Platform models gain in popularity, offering institution- and product-agnostic algorithms that match customers with products based on price and fit (identified with data-driven insights).

- Incumbents accelerate their push for customers to be self-serviced through digital and call-center channels. The acceleration is driven by worsening customer economics and foreign new entrants.

Prolonged pandemic period, spurring governments to adopt isolationist policies, shorten supply chains, and increase surveillance.

- Severe, rolling pandemics.

- Insufficient global coordination and weak policy response.

Banking system

- Overall trust in the banking system declines due to the prolonged crisis eating at banks’ capital and limiting the effectiveness of government backstops. Loyalty to individual banks also decreases as customers switch banks often in search of the best yield.

- Some international banks make plans to exit the US as they find it costly to operate across multiple countries with divergent and strict regulations.

- Community and regional banks that historically have not invested in digitalization struggle to remain competitive from a pricing and digital experience perspective, leading to significant market consolidation as those banks are acquired by larger and stronger incumbents.

- The US accelerates digitization and becomes a more cashless economy to reduce the risk of contagion through physical currency bills. Merchants invest in facial recognition and geo-sensors to facilitate contactless payments and money transfer.

For an in-depth discussion of the four scenarios, ten potential implications for consumer banking in the US, irrespective of which scenario unfolds, and seven no-regret actions in the following six to nine months that can better position banks to recover. Download the PDF here.

Get in touch

Thomas Nicolosi

Principal | Deloitte Risk & Financial Advisory

Chris Smith

Audit & Assurance Partner | Deloitte & Touche LLP

Recommendations

The CARES Act: Summary for financial services

FSI provisions for the Coronavirus Aid, Relief, and Economic Security Act