Evolving role of professional services in software companies has been saved

Perspectives

Evolving role of professional services in software companies

Discover strategies and professional services trends

Software companies have traditionally focused their professional services offerings on deploying, customizing, and optimizing on-premise products. As companies shift to SaaS- and consumption-based models, they have an opportunity to evolve the role professional services plays to meet emerging customer needs.

Software industry trends having an impact on professional services

Across the software industry, we have witnessed the growing shift of customer preferences away from perpetual licenses deployed on-prem to as-a-service software deployed on the cloud or in a hybrid environment.

By the end of 2022 , more than 90% of global enterprises were relying on some form of hybrid (combination of private and public) cloud deployment1. Gartner estimates the market size of SaaS products and services was $123 billion in 2021 and is expected to grow more than 19% to $145 billion by the beginning of 20232. One of the main drivers of this explosive growth has been the increased ease and flexibility of deploying, maintaining, and scaling software solutions delivered via the cloud.

Relative to on-prem deployments, cloud-based delivery has reduced the complexity of configuring and operating the underlying software products. The simplest SaaS applications, targeted at smaller customer segments today, are broadly “plug and play,” with end users enabled by in-product guidance, on-demand learning, and community-led support. However, realizing the value of feature-rich enterprise software, especially when deploying complex use cases or driving adoption of advanced features, remains heavily dependent on the involvement of professional services to drive the initial deployment and enable internal teams for success. While the role of professional services was limited to one-time implementation of solutions purchased by customers, there is now an increased expectation to go beyond implementation and drive ongoing adoption by delivering business and technical outcomes, such as ensuring faster go-live through best practices and enabling a first use case within a certain time frame (e.g., 90 days). This introduces an opportunity to introduce new professional services offerings that provide deep technical expertise and on-demand guidance across the end-to-end customer journey.

At the same time, with annual recurring revenue (ARR) emerging as a leading measure of sales efficiency for SaaS companies, many have shifted focus to increasing the share of recurring (subscription- and consumption-based) revenue relative to one-time revenue obtained from traditional perpetual license-based models. Gross margins on mature products offered by SaaS companies typically exceed 75%3, much higher than margins obtained via on-prem business models.

However, based on a Deloitte professional services industry survey4 across 50–70 services organizations, gross margins on professional services vary widely, anywhere from +40% to –40% (figure 1) depending on the strategic role of Professional Services (PS) , pricing structures, discounting models, and labor costs associated with delivery.

This variance is due to the still evolving role of professional services within software companies: Some traditional computer and network infrastructure-oriented companies continue to view professional services as a profit driver contributing to the overall P&L, whereas many established SaaS companies are willing to temporarily sacrifice margins to grow product ARR. The trend is amplified by hyperscalers with consumption-based models who use professional services as a loss leader to drive new logo acquisition. Additionally, some companies that frequently deploy highly complex and scalable enterprise solutions offer free or heavily discounted professional services as part of an initial discovery phase to reduce time to value for their largest deals.

Overall, in the context of SaaS- and consumption-based deployments, we are seeing a shift in the focus of professional services organizations from direct profitability to enabling customer outcomes and thereby driving expansion of recurring product revenue.

Evolving role of professional services in enterprise software companies

An additional trend we have observed is a decrease in attach rates, or professional services revenue per dollar of product revenue sold, for cloud and hybrid deployments relative to traditional on-prem software deployments. Although it varies by product category and customer segment, average attach rates for SaaS- and consumption-based solutions are frequently around 0.25x–1.5x, much lower than the 2x–3x attach rate for on-prem deployments (figure 1). Focusing on adoption and expansion is a relatively new sales motion for services sellers. As such, professional services tends to take a back seat after the initial implementation (which itself is typically a smaller deal due to the reduced complexity of implementing SaaS and cloud-based software).

Additionally, some companies may use channel partners to deliver low-margin services to drive scale at low cost. As a result, the typical size of the professional services organization, by revenue, has also decreased and is generally less than 20% of overall revenue for companies that predominantly provide cloud-based software offerings. This presents an opportunity to introduce new professional services offerings, such as adoption and optimization services, and educate and enable sales and customer success teams to attach PS offerings beyond the initial deal. (We will delve deeper into outcome-based service portfolio strategy in an upcoming paper.)

Strategic choice points for software companies to consider

The expanded role of professional services in realizing full potential of the deployed cloud solution, together with near-term pressure on financial metrics, presents organizations with several strategic choices to consider around offering design, GTM, and operating model.

Within software companies, professional services typically refers to an organization of technology and solution experts engaged in delivering technical advisory and implementation services for their customers. As the size of traditional professional services deals (product-led, project-based, implementation-oriented services) decreases with increased demand for cloud-based deployments, companies are investing in new capabilities and repeatable, scalable offerings to stay relevant. This is manifested in the fact that services are being made available in more bite-sized, on-demand packages, at lower costs and with rapid delivery to meet changing product needs and customer preferences. Across the spectrum of software companies, the emerging portfolio of professional services offered can be broadly classified into four types across the customer life cycle:

- Visioning services are focused on understanding customer needs, which are often 100% funded by the solution provider as a cost of the sale. Depending on customer size and level of vendor investment, these services could be delivered as high-touch engagements (e.g., visioning workshops) or digital tools (e.g., online surveys that measure organization, process, and tooling maturity) with the same goal of accelerating sales deal velocity and teeing up follow-on professional services engagements at higher value and margins.

- Assessment services help customers evaluate current-state technology and tooling landscape and design SaaS- and consumption-based solutions that help deliver desired customer outcomes. These are generally sold at cost or low margins to get customers through the engagement funnel to high-margin activities.

- Migration and adoption services leverage industry best practices and technical and solution expertise in the professional services organization of the service provider to help customers deploy, integrate, and configure solutions, migrate data, and go live faster. The margin for these services increases to between 20% and 50% at maturity and sees increased partner involvement in implementation to reduce costs.

- Optimization services leverage usage data to proactively work with customer teams to build hands-on product experience, accelerate adoption, automate business operations, and shape business outcomes. These services are the most profitable, with margins up to 60% at maturity, but also play a critical role in maintaining customer retention and, hence, driving up Net Dollar Retention Metric (NDR)5.

For example, Splunk6 has invested in launching a portfolio of lightweight, prepackaged, on-demand advisory, implementation, and education services that most customers are entitled to via a success plan embedded in their product purchase. Customers receive credits on a recurring basis, which they can burn down to purchase specific tasks (e.g., build a new dashboard) in Splunk’s predefined service catalog that enable success across the customer life cycle.

From a GTM perspective, the addition of new routes to market for SaaS/cloud products (e.g., e-commerce platforms and cloud marketplaces) enables companies to increase their total addressable market by targeting new customer segments (e.g., mid-market, small and medium businesses). However, given the lower average deal sizes common within these segments, the repeatable, scalable offerings outlined in the prior section are a prerequisite to targeting them.

Additionally, companies transitioning to SaaS models have an opportunity to expand their partner ecosystem by shifting focus from resellers and distributors to an increased emphasis on system integrators and managed service providers that complement their internal professional services organizations and expand their reach to high-volume, lower-margin segments.In addition to building a network of professional services partners to supply low-margin, implementation capacity, we see companies embracing partners to develop industry-specific solutions that are valued at a premium by customers, thus increasing the overall marketing and sales capabilities for product license growth in addition to services.

The evolving role of professional services organizations in SaaS- and consumption-based companies means that the lines between professional services, customer success, and sales are often blurred. Increasingly, customer success is emerging as a persistent, proactive orchestrator, focused on building long-term relationships with the customer’s IT and business stakeholders and driving adoption across entire customer life cycle. In turn, professional services leverages specialized technical and product expertise in time-bound engagements to accelerate time to value of new releases and expand the number of deployed use cases. However, it is not unnatural for companies to be challenged by friction between these functions, and we observe distinct strategic choices in response.

Companies with highly configurable, cloud-based platforms such as Salesforce have unified professional services under the broader umbrella of customer success to provide expertise, accelerate time to value, boost adoption, and improve customer experience7. Breaking down internal functional silos allows for greater sharing of technical expertise and clarity in roles and responsibilities across customer touchpoints required to operationalize and deliver seamless customer experience.

Alternatively, companies with a more complex portfolio mix of IaaS, PaaS, and SaaS offerings deploy a well-defined engagement model in which collaboration between customer-facing service functions is incentivized and the role of professional services is expanded to be an enabler for delivering customer outcomes. Mutually beneficial positioning, in which customer success identifies opportunities to expand service coverage and professional services is pulled through to provide deep technical expertise, drives higher adoption and, thereby, likelihood of retention. This also means companies need to measure the success of professional services organizations beyond margins and through metrics, such as a combined scorecard consisting of customer success and professional services metrics with shared accountability.

While a full-scale PS transformation that includes reimagining the service charter and traditional ways of doing business may be required in companies transitioning to SaaS- and consumption-based models, we observe five winning moves that can set up professional services organizations to deliver on desired customer outcomes and positively influence expansion of recurring revenue.

Winning moves to evolve the role of software professional services

As discussed earlier, SaaS companies are increasingly realizing that customers in the commercial and mid-market segments need professional services support to realize the value of their deployed solution. However, the enterprise sales and delivery motion for professional services can be highly labor and cost intensive and does not scale to serve these new segments; additionally, the traditional emphasis on implementation leads to a lack of focus on adoption, which is required to sustainably drive recurring revenue. SaaS- and consumption-based software companies that aim to drive adoption and target new segments can benefit from five winning moves across their value chain from strategy to delivery.

Set a clear professional services strategy in the context of overall customer outcomes and influencing NDR: First, articulate the strategic role of professional services as a driver of product adoption, and align capabilities, staffing, and stakeholder expectations accordingly. This could also mean measuring time to value for PS engagements, long-term adoption, or customer health metrics and, from an operational perspective, potentially having lower utilization targets to account for time spent on adoption activities. Based on product and business goals, tie professional services outcomes to customer success, and measure broader-impact metrics delivered across the customer life cycle.

Develop prepackaged offerings: Second, invest in development of prepackaged service offerings that can be marketed and sold to SMBs and commercial-tier customers at a lower cost of delivery without slowing down the deal velocity. This follows Deloitte surveys that highlight growing customer need and willingness to pay. So, the onus is on providers to make it easy for these customers to buy and consume professional services offerings. This can take the form of predefined engagements, digital tools, and execution frameworks, among others. Figure 5 shows the increasing use of prepackaged offerings for geographic regions and customer segments with low affinity for premium range of services.

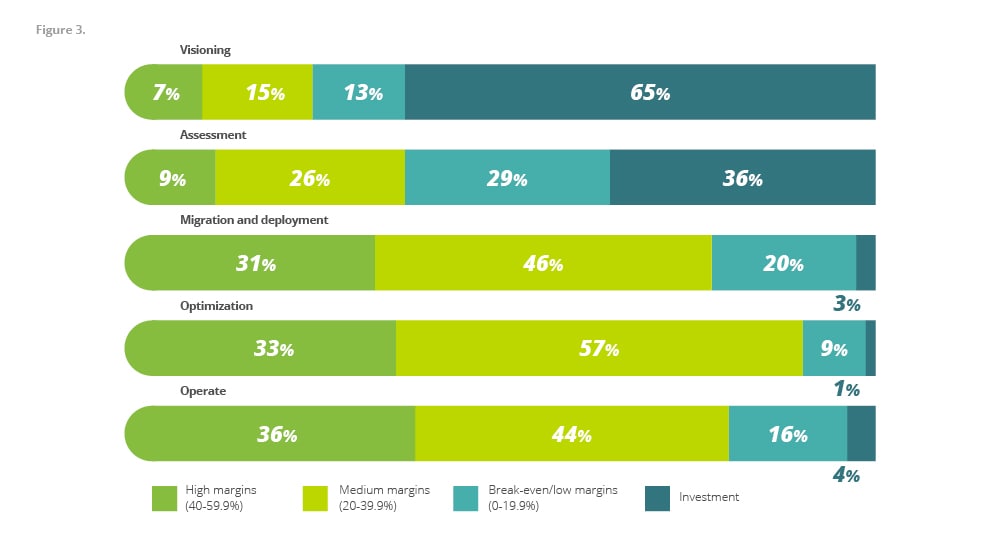

Introduce flexibility in margin targets across the customer life cycle: Third, vary margin targets to increase stickiness across the customer life cycle. Gain customer mindshare through upfront investments in deal cycle, and recover margins as solution offerings mature over time. As shown in survey results in figure 3 below, nearly 78% and 65% of software companies are providing visioning and assessment services, respectively, as an investment or at break-even cost.

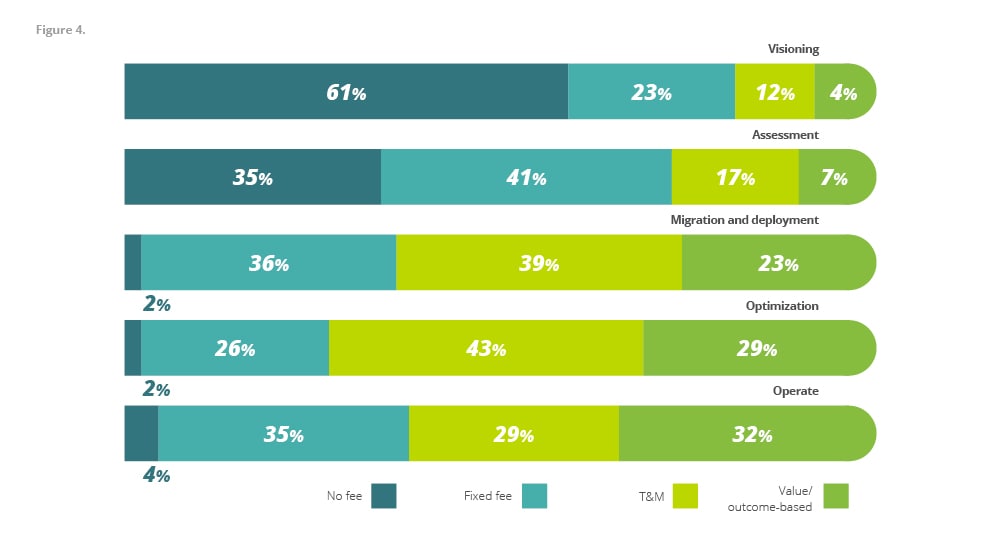

Introduce value-based pricing: Fourth, for large, routine, late-stage engagements with enterprise customers, consider employing value-based pricing that aims to maximize profitability to make up for margins lost in the early stages. At the same time, for SMB customers, use cost-plus pricing that provides full cost coverage and hedges against customers’ unwillingness to pay at future engagement stages. Figure 4 shows the increasing use of value/outcome-based pricing models by software companies at late-stage professional services engagements.

Rethink talent model, skills, and delivery centers: Finally, executing these changes requires fundamental shifts in the skills needed, organization design, and use of delivery models, such as outsourcing and partners. For example, companies are identifying predefined, skills-based technical advisory services (e.g., guidance for advanced product adoption, optimization services) that can be performed by a pooled set of resources from a near-shore delivery center. Companies are already capitalizing on strong software engineering talent in Asia and Eastern Europe to improve cost mix and access to in-demand skills.

Keep the professional services evolution going

While the nature and boundaries of professional services organizations within software companies are evolving rapidly, it is important to note that there is no one-size-fits-all for professional services organizations, and leaders must continue to evolve in line with the shifts in overall corporate strategy. Professional services teams will need to gain incremental capabilities and adapt to new offerings, packaging, pricing, operating models, GTM, and measurement practices but will remain a key strategic instrument of driving revenue growth and product adoption for SaaS- and consumption-based software companies.

Endnotes

1 Deloitte, “The cloud migration forecast: Cloudy with a chance of clouds,” December 2020.

2 Gartner, “Gartner forecasts worldwide public cloud end-user spending to grow 18% in 2021,” November 2020.

3 Software Equity Group, “The impact of gross margin on SaaS valuations,” March 2021.

4 Deloitte, Deloitte Professional Services Industry survey, February 2022.

5 “Driving sustainable and repeatable growth in Enterprise SaaS”, April 2022

6 Splunk, “Success plans,” August 2022.

7 Salesforce, “CS and PS offerings,” August 2022.

Get in touch

|

|||||||

|

Marybeth D’Souza |

|

Gopal Srinivasan |

||||

|

Jon Smyrl |

|

Aftab Khanna |

||||

Recommendations

Customer outcomes: Chief Customer Officer study

A new focus for B2B technology companies